YZi Labs-backed perpetual DEX platform Aster has finally unveiled its Aster Chain mainnet. The new chain will adopt zero-knowledge proofs and stealth addresses in a bid to curb ‘position hunting,’ common on transparent public chains and platforms like Hyperliquid.

Initially, the DEX debuted on BNB Chain via a bridge and later extended to Ethereum [ETH], Solana [SOL], and Arbitrum [ARB] as a multi-chain dApp. While it will still support trading across these chains, it will transition into a sovereign Layer 1 ecosystem.

The move is aimed at achieving the privacy and other optimal features for high-frequency traders while maintaining a CEX-like user experience.

Aster’s market share falls

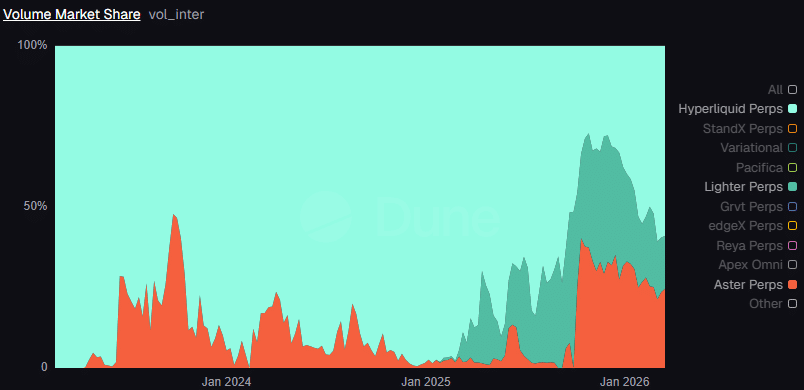

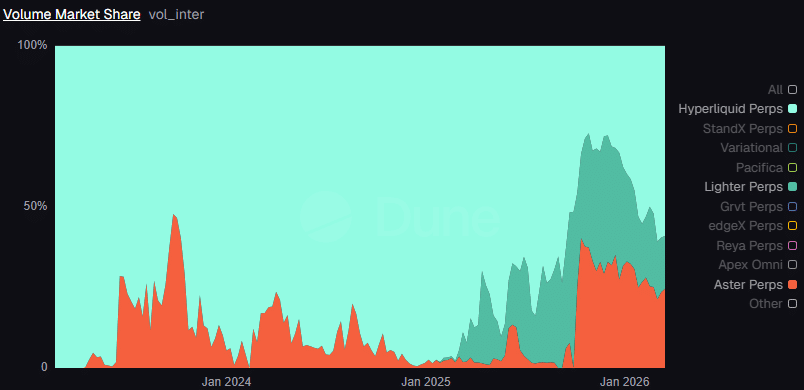

Although the DEX became an instant hit after its launch last September, the traction has waned significantly in 2026.

During its peak activity in October 2025, it handled nearly $74 billion in weekly trading volume. But its trading activity shrank to less than $10 billion as of mid-March 2026, following the broader crypto rout in the past few months.

Its overall market share in perps trading volume declined by half, from 40% to 20%, over the same period.

Interestingly, Aster’s wild FOMO after launch clawed down Hyperliquid’s [HYPE] market share. Hyperliquid had over 60% dominance before Aster went live. Afterward, its dominance fell to 27% but began reclaiming it only after unveiling trading support for oil, gold, silver, and other commodities via HIP-3.

As of writing, Hyperliquid has regained most of its trading volume, while Aster’s steep decline has not abated.

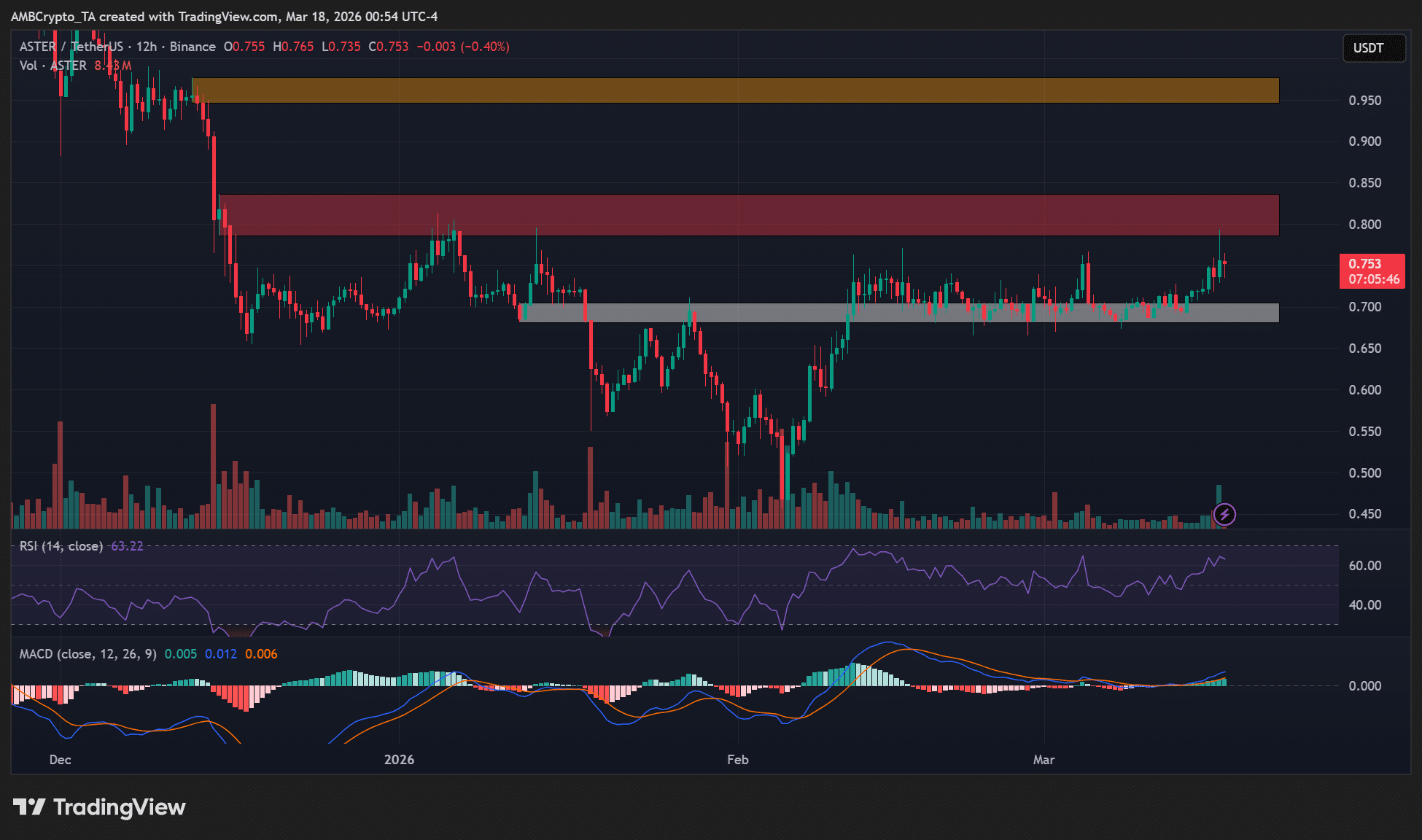

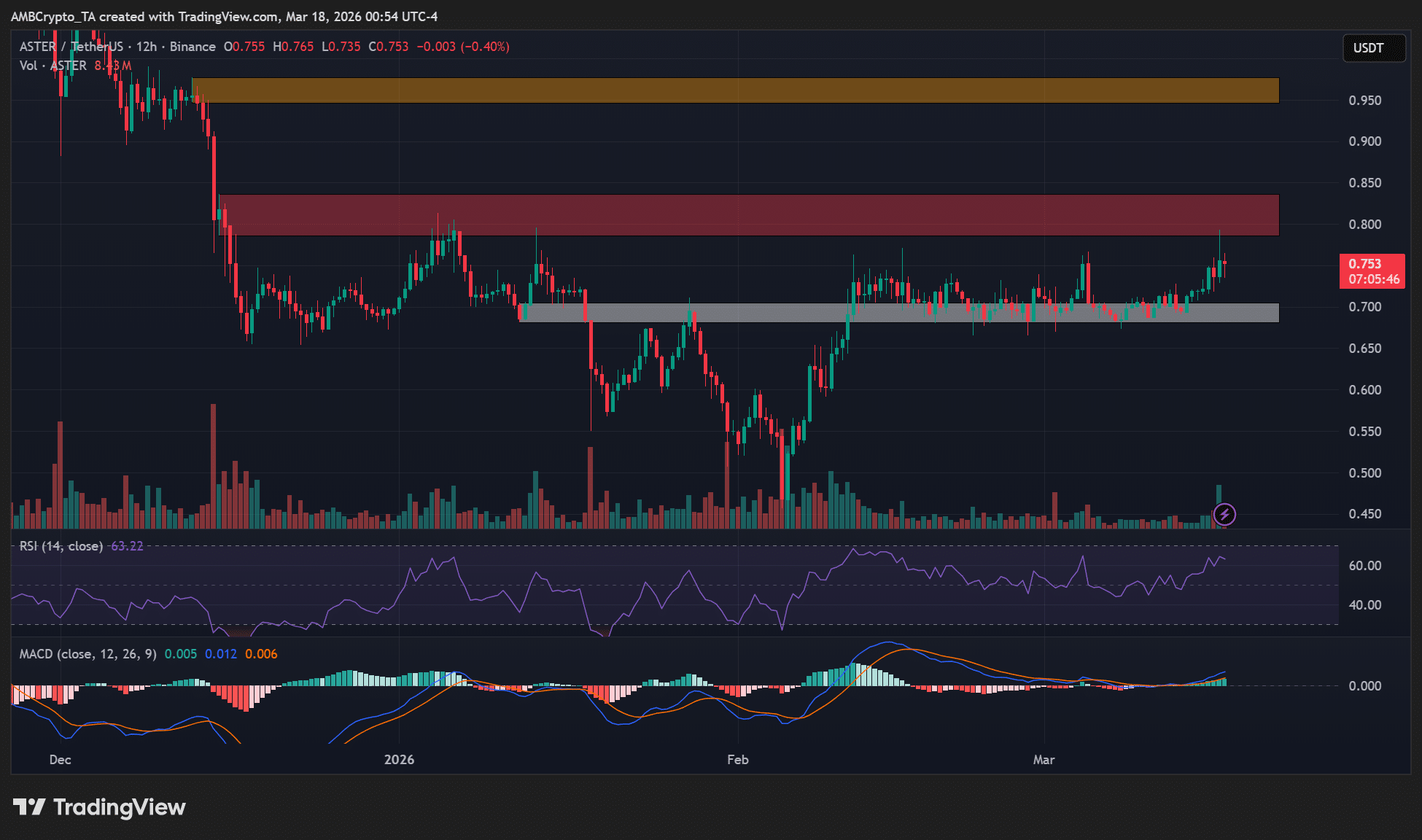

ASTER price reaction

Likewise, its native token ASTER slumped 86% after a free fall from $3 to a low of $0.4. However, the broader market relief bounce from early February has boosted the altcoin’s recovery by 80%.

But the mainnet debut didn’t help bulls that much. After the update, ASTER swiftly rallied by nearly 10%, hitting $0.790, but had erased most of the gains at the time of writing.

When zoomed out, the altcoin was still stuck at its February tight price range of $0.70 and $0.80. The sideways structure may extend if there is no meaningful catalyst for a broader market extended recovery.

However, should the $0.80 price level be flipped to support, then retesting $0.950 could be feasible. It’s unclear whether the planned staking feature will induce demand for ASTER.

Final Summary

- Aster has unveiled its Aster Chain mainnet to double down on privacy and trading efficiency.

- Still, the DEX’s traction remains in a downtrend while the ASTER price has been stuck in a tight range.