Thị trường crypto tháng 12 lạnh như thời tiết.

Giao dịch on-chain đã ngủ đông từ lâu, các narrative mới cũng khó lòng xuất hiện. Chỉ cần nhìn vào những tranh cãi và tin đồn mà cộng đồng CT Trung Quốc đang bàn tán vài ngày gần đây, là đủ biết thị trường này chẳng còn mấy ai chơi nữa.

Nhưng ở cộng đồng tiếng Anh, mấy ngày nay đang bàn về một thứ mới.

Một đồng meme coin tên là Snowball, phát hành trên pump.fun vào ngày 18 tháng 12, chỉ trong bốn ngày vốn hóa đã lao lên 10 triệu USD và vẫn đang lập đỉnh mới; trong khi cộng đồng Trung Quốc hầu như không ai nhắc đến.

Trong bối cảnh không có narrative mới và meme chó cũng chẳng thèm chơi như hiện nay, đây có lẽ là một trong số ít thứ khiến người ta sáng mắt, mang lại hiệu ứng tài sản cục bộ.

Mà cái tên Snowball dịch ra là hiệu ứng quả cầu tuyết, vốn đã là câu chuyện nó muốn kể:

Một cơ chế khiến token "tự lăn càng to".

Biến phí giao dịch thành lực mua, market-making như lăn quả cầu tuyết

Muốn hiểu Snowball đang làm gì, trước tiên phải biết token trên pump.fun thường kiếm tiền như thế nào.

Trên pump.fun, bất kỳ ai cũng có thể tạo một token trong vài phút. Người tạo token có thể thiết lập "phí nhà sáng tạo", nói thẳng ra là cứ mỗi giao dịch thì抽 một tỷ lệ nhất định vào ví của mình, thường trong khoảng 0.5% đến 1%.

Về lý thuyết, số tiền này có thể dùng để xây dựng cộng đồng, quảng bá thị trường, nhưng trong thực tế, lựa chọn của hầu hết Dev là: tích đủ rồi rút chạy.

Đây cũng là một phần trong vòng đời điển hình của một con shitcoin. Phóng, kéo, thu phí, bỏ chạy. Nhà đầu tư đang cá cược không phải vào bản thân token, mà là lương tâm của nhà phát triển.

Cách làm của Snowball là, không lấy tiền phí nhà sáng tạo này.

Chính xác hơn, 100% phí nhà sáng tạo không vào ví của bất kỳ ai, mà được tự động chuyển vào một bot market-making on-chain.

Bot này định kỳ thực hiện ba việc:

Thứ nhất, dùng số vốn tích lũy để mua token trên thị trường, tạo thành lực mua hỗ trợ;

Thứ hai, thêm token đã mua và SOL tương ứng vào pool thanh khoản, giúp depth giao dịch tốt hơn;

Thứ ba, mỗi lần thao tác đốt 0.1% token, tạo ra giảm phát.

Đồng thời, tỷ lệ phí nhà sáng tạo mà token này thu không cố định, mà sẽ dao động từ 0.05% đến 0.95% tùy theo vốn hóa thị trường.

Khi vốn hóa thấp thì抽 nhiều hơn một chút, để bot tích lũy đạn dược nhanh hơn; khi vốn hóa cao thì giảm xuống, giảm ma sát giao dịch.

Tóm tắt logic của cơ chế này trong một câu, mỗi lần bạn giao dịch, là có một khoản tiền tự động biến thành lực mua và thanh khoản, chứ không phải vào túi nhà phát triển.

Vì vậy, bạn cũng dễ dàng hiểu hiệu ứng quả cầu tuyết này:

Giao dịch sinh ra phí → Phí biến thành lực mua → Lực mua đẩy giá cao → Giá cả thu hút nhiều giao dịch hơn → Nhiều phí hơn...... Về lý thuyết có thể tự lăn.

Tình hình dữ liệu on-chain

Nói xong cơ chế, hãy xem dữ liệu on-chain.

Snowball phóng vào ngày 18 tháng 12, đến nay là bốn ngày. Vốn hóa từ 0 lao lên 10 triệu USD, khối lượng giao dịch 24h vượt 11 triệu.

Đối với một shitcoin trên pump.fun, thành tích này đã được coi là sống lâu trong môi trường hiện tại rồi.

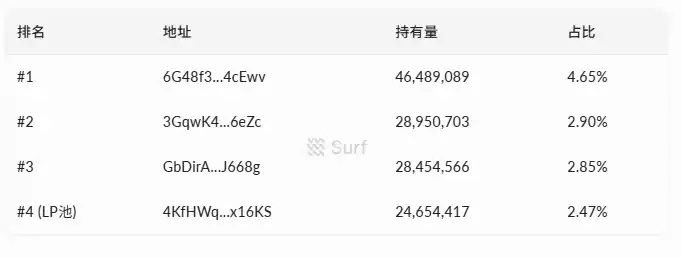

Về cấu trúc nắm giữ, hiện có 7270 địa chỉ nắm giữ. Top 10 người nắm giữ lớn nhất cộng lại chiếm khoảng 20% tổng cung, người nắm giữ đơn lẻ lớn nhất chiếm 4.65%.

(Nguồn dữ liệu: surf.ai)

Không xuất hiện tình trạng một địa chỉ nắm giữ hai ba phần mười cung, phân bố tương đối phân tán.

Về dữ liệu giao dịch, từ khi phóng đến nay tích lũy hơn 58000 giao dịch, trong đó 33000 lần mua, 24000 lần bán. Tổng số tiền mua vào 4.4 triệu USD, bán ra 4.3 triệu USD, dòng tiền ròng vào khoảng 100k. Mua bán cơ bản ngang bằng, không xuất hiện áp lực bán dồn về một phía.

Trong pool thanh khoản nằm khoảng 380k USD, một nửa là token một nửa là SOL. Đối với thể thức vốn hóa này, depth không dày, lệnh lớn ra vào vẫn sẽ có trượt giá rõ rệt.

Một điểm đáng chú ý khác là, Bybit Alpha đã宣布 lên sàn token này chưa đầy 96 giờ sau khi phóng, ở một mức độ nào đó cũng chứng thực sức nóng ngắn hạn.

Động cơ vĩnh cửu gặp thị trường lạnh lẽo

Đi dạo một vòng, có thể thấy cộng đồng tiếng Anh thảo luận về Snowball chủ yếu tập trung vào bản thân cơ chế. Logic của người ủng hộ rất trực tiếp:

Đây là meme coin đầu tiên khóa 100% phí nhà sáng tạo vào giao thức, nhà phát triển không thể lấy tiền bỏ chạy, ít nhất về mặt cấu trúc là an toàn hơn các shitcoin khác.

Dev phát triển cũng đang phối hợp với narrative này. Ví nhà phát triển, ví bot market-making, nhật ký giao dịch đều công khai, nhấn mạnh "có thể kiểm tra on-chain".

@bschizojew tự dán nhãn cho mình là "tâm thần phân liệt on-chain, lực lượng đặc chủng 4chan, lính già meme coin thế hệ đầu", mang đầy hương vị degen tự giễu, rất hợp với khẩu vị cộng đồng crypto native.

Nhưng cơ chế an toàn và kiếm được tiền hay không là hai chuyện khác nhau.

Điều kiện tiên quyết để hiệu ứng quả cầu tuyết thành lập là, có đủ khối lượng giao dịch liên tục sinh ra phí, để nuôi bot thực hiện mua lại. Giao dịch càng nhiều, bot càng đủ đạn, lực mua càng mạnh, giá càng cao, thu hút nhiều người giao dịch hơn...

Đây cũng là trạng thái lý tưởng mà bất kỳ bánh xe flywheel mua lại nào của meme được cho là quay lên trong bull market.

Vấn đề là, bánh xe cần động lực bên ngoài để khởi động.

Môi trường thị trường crypto hiện tại là gì? Hoạt động on-chain trầm lắng, sức nóng tổng thể của meme coin giảm sút, số vốn sẵn sàng xông vào shitcoin vốn đã ít. Trong bối cảnh này, nếu lực mua mới không theo kịp, khối lượng giao dịch teo lại, phí mà bot nhận được sẽ ngày càng ít, lực mua lại yếu đi, hỗ trợ giá giảm, ý chí giao dịch tiếp tục giảm.

Bánh xe có thể quay xuôi, cũng có thể quay ngược.

Vấn đề thực tế hơn là, cơ chế giải quyết một điểm rủi ro "nhà phát triển rút tiền bỏ chạy", nhưng rủi ro mà meme coin đối mặt còn xa hơn thế.

Zhuāng家 xả hàng, thanh khoản không đủ, narrative lỗi thời, những việc này xảy ra một cái bất kỳ, thì việc mua lại bằng 100% phí giao dịch cũng chỉ có tác dụng rất hạn chế.

Mọi người đều bị割 sợ rồi, trong cộng đồng Trung Quốc cũng có anh总结 khá đúng:

Chơi thì chơi, đừng quá đà.

Không chỉ một quả cầu tuyết đang lăn

Snowball không phải là dự án duy nhất kể câu chuyện market-making tự động này.

Cùng trong hệ sinh thái pump.fun, một token tên là FIREBALL cũng đang làm việc tương tự: mua lại tự động cộng đốt, đóng gói nó thành một giao thức mà token khác có thể kết nối vào. Nhưng vốn hóa nhỏ hơn Snowball rất nhiều.

Điều này说明 thị trường hiện nay có phản ứng với hướng "meme coin kiểu cơ chế".

Cách chơi truyền thống喊单, kéo,炒作 cộng đồng ngày càng khó thu hút vốn, dùng thiết kế cơ chế để kể một câu chuyện "an toàn cấu trúc", có lẽ là một trong những套路 gần đây của meme coin.

Tuy nhiên, nói đến việc tạo ra một cơ chế nào đó nhân tạo, cũng không phải cách chơi mới.

OlympusDAO năm 2021 với (3,3) là trường hợp điển hình nhất, dùng lý thuyết trò chơi đóng gói cơ chế staking, câu chuyện kể là "mọi người đều không bán thì có thể cùng nhau kiếm lời", thời kỳ đỉnh cao vốn hóa lao lên几十 tỷ USD. Kết cục về sau mọi người cũng biết, xoáy giảm, giảm hơn 90%.

Sớm hơn một chút còn có cách chơi của Safemoon "mỗi giao dịch抽税 chia cho người nắm giữ", cũng là narrative đổi mới cơ chế, cuối cùng bị SEC kiện, người sáng lập bị buộc tội gian lận.

Cơ chế có thể là cái móc narrative rất tốt, có thể tập trung vốn và sự chú ý trong thời gian ngắn, nhưng bản thân cơ chế không tạo ra giá trị.

Khi dòng tiền bên ngoài ngừng chảy vào, bánh xe flywheel tinh xảo đến mấy cũng sẽ ngừng quay.

Cuối cùng, chúng ta hãy gỡ lại xem chú chó vàng nhỏ này rốt cuộc đang làm gì:

Biến phí nhà sáng tạo của meme coin thành "bot market-making tự động". Bản thân cơ chế không phức tạp, vấn đề giải quyết cũng rõ ràng, đó là khiến nhà phát triển không thể trực tiếp lấy tiền bỏ chạy.

Nhà phát triển không thể bỏ chạy, không có nghĩa là bạn kiếm được tiền.

Nếu bạn xem xong thấy cơ chế này thú vị, muốn tham gia, hãy nhớ một câu: nó trước hết là một meme coin, sau đó mới là thử nghiệm của một cơ chế mới.