撰文:Cookie,律动

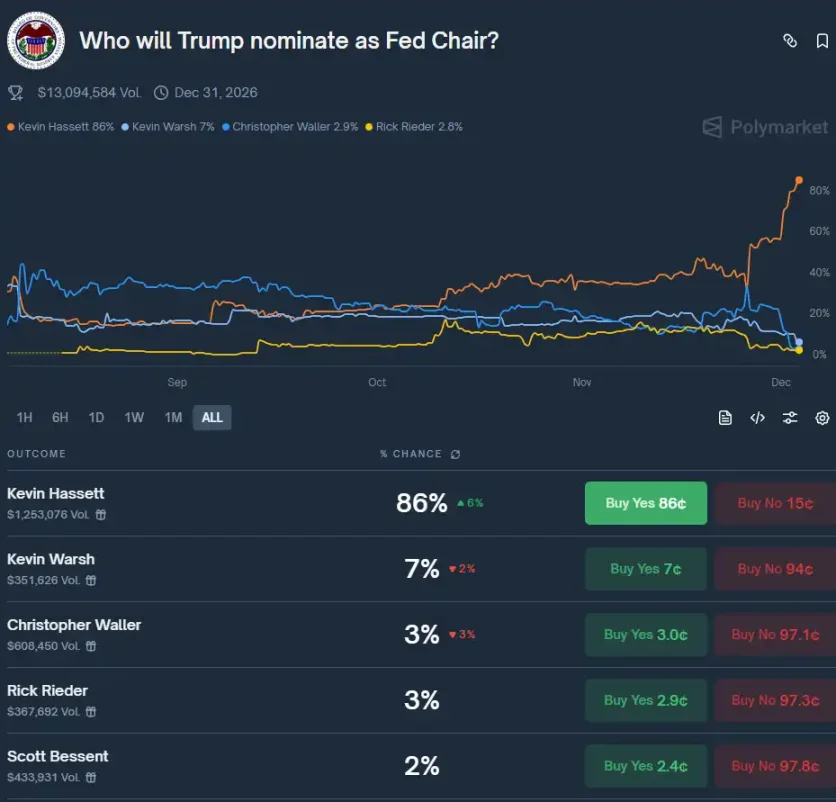

在预测市场 Polymarket 上,哈塞特当选新一任美联储主席的概率已经上升至了 86%,远远领先其他可能的美联储新任主席人选。

不出意外的话,凯文·哈塞特(Kevin Hassett)会是下一届美联储主席,特朗普的最爱。

美联储的动作一直是影响加密货币市场的重要因素。那么,如果哈塞特最终如市场预期那般成为新一任美联储主席,预计会对市场造成哪些影响呢?

加速降息

哈塞特 11 月底的时候曾表示,此时暂停降息将是「非常糟糕的时机」,因为政府停摆已经拖累了第四季度的经济增长。他预计政府停摆将导致第四季度国内生产总值(GDP)下降 1.5 个百分点。与此同时,他指出 9 月份消费者价格指数(CPI)显示,通胀表现好于预期。

更早一些的时候,11 月 13 日,哈塞特表示,预计第四季度 GDP 将因政府停摆而下降 1.5%。看不到不降息的太多理由。

因此,若哈塞特成为新一任美联储主席,预计他将推动更快的利率下调,可能将联邦基金利率降至 3% 以下,甚至接近 1%,以刺激经济增长和就业。

这也是特朗普想看到的。

恢复 QE

12 月 1 日,美联储正式结束了量化紧缩(QT)政策,这标志着从 2022 年开始的资产负债表缩减过程的结束。尽管有观点认为,相关效果或将于明年年初才能显现,但流动性宽松预期已获得逐步实现。

哈塞特可能对通胀更宽容,将 2% 通胀目标视为灵活上限,而非严格锚定。重点放在就业和 GDP 增长上,减少对数据依赖的「渐进式」决策,转向更主动的亲增长干预。

今年 9 月,哈塞特在接受 Fox Business 采访时表示,美国正处于供给侧繁荣的时期,在没有真正通胀的经济体中,当前利率正阻碍经济增长和就业创造。同时他还表示,美国有望实现 4% 的 GDP 增长。

优先发展经济而非通膨控制的观点,让哈塞特执掌后的美联储重启 QE 是可以被期待的。

对比特币的影响

每一位美联储主席候选人,不论其是否直接谈论加密话题,都将对加密货币行业产生结构性影响,而哈塞特更与加密货币行业有着不容忽视的关联,他不仅曾公开持有价值百万美元的 Coinbase 股票,还担任过 Coinbase 的顾问委员会成员。

此外,他曾参与白宫内部关于数字资产政策的工作小组,推动在监管框架中为创新保留空间,并认为加密技术是影响未来经济结构的重要变量。他曾表示比特币将「改写金融规则」。

哈塞特的加密背景可能会减少监管不确定性,推动机构推动和美联储探索加密货币整合。这可以提升比特币的合法性和流动性,潜在推动价格至新高。

有不少交易员看好哈塞特上任后的行情,认为上任后才是牛市的开始,预计时间是明年年中,所以 26 年下半年是加密货币行业的重中之重。