美联储最近释放的降息信号,让市场对流动性宽松的预期进一步升温,提前推动了部分资金涌入加密市场,作为一种新兴资产类别,其对冲传统风险和价值存储的叙事,仍在持续吸引机构层面的兴趣。

全球经济复苏与不确定性交织的当下,美联储货币政策的一举一动,始终牢牢牵动着投资者的注意力。

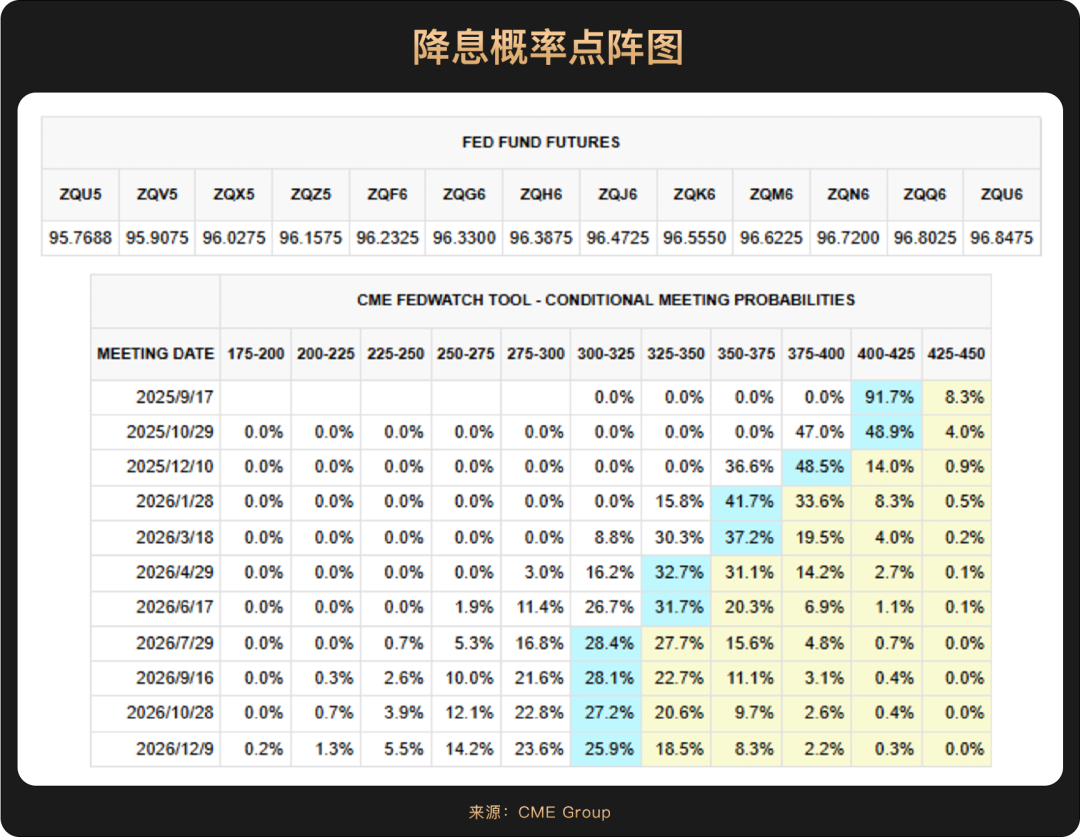

8月末,美联储主席鲍威尔向市场释放了货币政策转向的明确信号。他不但一改7月时“通胀风险权重高于就业风险”的鹰派立场,转而警告就业下行风险引发“裁员大幅增加和失业率上升”。这番言论使得市场对9月降息的概率预期一度从75%飙升至90%以上,标志着美联储政策天平正在向促就业倾斜。

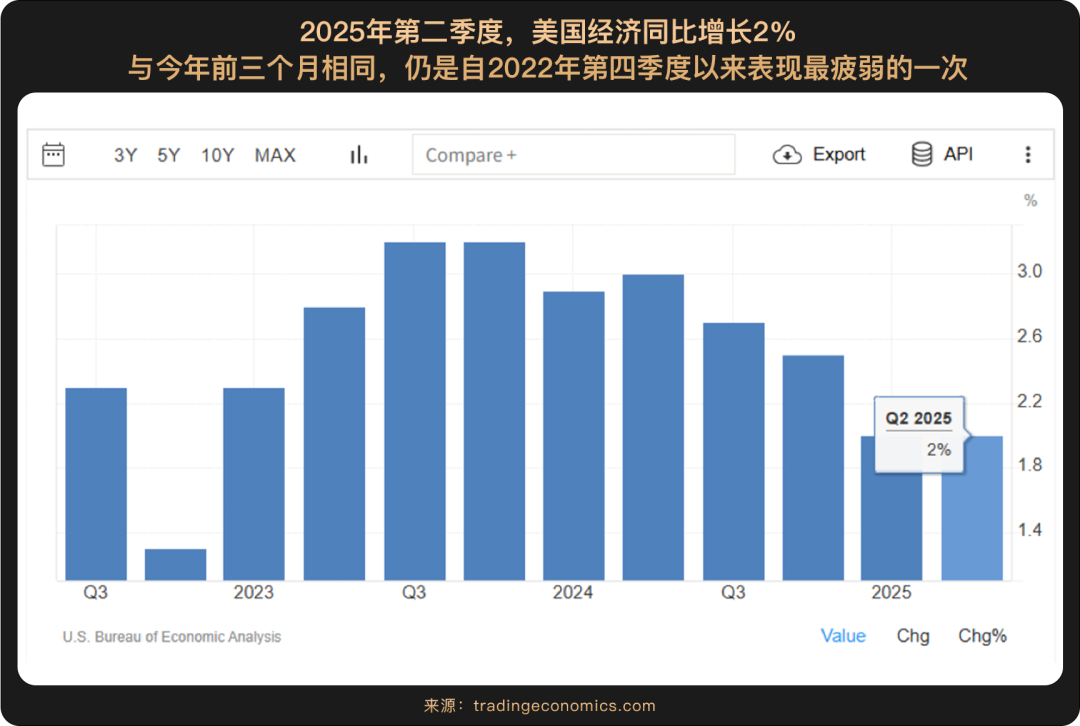

鲍威尔的这一转向并非空穴来风,其背后是美国经济动能显著放缓的现实。2025年上半年美国GDP年化增长率平均为1.2%,远低于2024年同期的2.5%。更为关键的是,劳动力市场虽然表面失业率稳定在4.2%,但内在疲态已现:美国7月新增非农就业人数骤降至7.3万人,大幅低于预期的10.4万人,为去年10月以来最小增幅,并且5、6月份的非农就业人数累计下修了25.8万。这表明经济扩张的力度已大不如前。

但通往降息的道路也不是一片坦途,通胀仍是美联储无法忽视的变量。虽然鲍威尔判断,关税带来的物价影响更可能是“一次性冲击”而非持续性通胀,且8月的五至十年期通胀率预期终值降至3.5%(低于预期的3.9%),但8月的CPI数据(截至发稿尚未公布)将是决定9月是否降息的“临门一脚”。若8月通胀数据超预期大涨(例如CPI环比增速超过0.5%),仍可能迫使美联储重新评估其决策。

且美国经济还笼罩在“类滞胀”的阴影之下。一方面,经济增速在放缓;另一方面,在关税和收紧的移民政策影响下,通胀压力并未完全消散。这种“增长放缓与物价压力并存”的复杂局面,意味着鲍威尔此次的鸽派转向信心不足,其措辞也更为谨慎。

美联储未来的政策路径将极度依赖数据,尤其是在通胀与就业两大目标出现矛盾时。如果后续通胀风险超越就业风险,鲍威尔同样有可能叫停降息。因此,我们在拥抱降息预期带来的短期资产价格欢愉之时,仍需对经济基本面的复杂性和货币政策的摇摆性保持一份清醒。

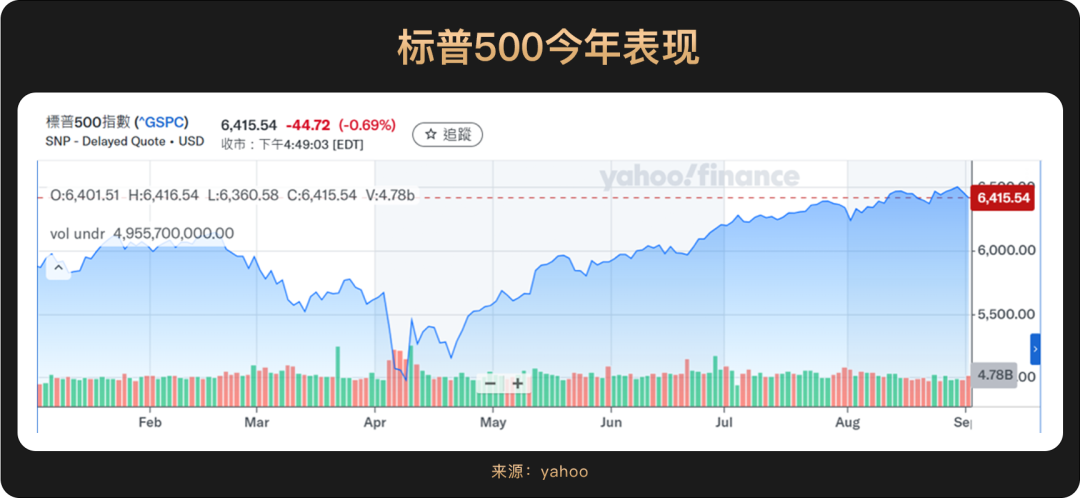

今年以来,美股在AI革命和政策转向预期的双重驱动下表现强劲,上半年美股已多次触及新高,科技股和成长股领涨。截至8月底,标普500指数年内涨幅接近10%,并多次刷新历史纪录,盘中一度突破6500点关口。

从财报数据来看,企业盈利是支撑市值的关键因素。美股2025 年 Q2 财报表现出色,其中AI 相关企业业绩格外突出,已成为推动此轮美股市场上扬的核心动力。英伟达(NVDA)作为 AI 领域的风向标,其二季度财报显示,营收同比大幅增长 56%。虽然数据中心收入略低于预期,但整体业绩证实了 AI 热潮的持续性,给市场增添了信心。其他芯片股同样表现不俗,博通(AVGO)和美光科技(MU)上涨了 3% 。AI 概念股 Snowflake(SNOW)因财报超预期,股价更是飙升约 21% 。

汇丰银行的分析指出,AI对企业的影响显著,44家标普500企业借助AI实现了1.5%的运营成本节约和平均24%的效率提升,这在一定程度上抵消了关税带来的压力。美联储的货币政策预期同样为市场提供了重要支撑,9月大概率降息提振了美股这类风险资产的表现。

不过,尽管美股表现强劲,但其估值已处于历史高位。截至8月,标普500指数的预期市盈率约22.5倍,虽低于历史峰值,但仍远高于2000年以来16.8倍的平均水平。

整体而言,2025年8月的美股市场在AI创新驱动、相对较稳健的经济基本面以及宽松货币政策预期的共同作用下,风险偏好得到显著提振。虽然估值偏高提示市场需保持一定警惕,但企业盈利的强劲增长,以及可能到来的降息周期,使得美股仍被认为具有吸引力。

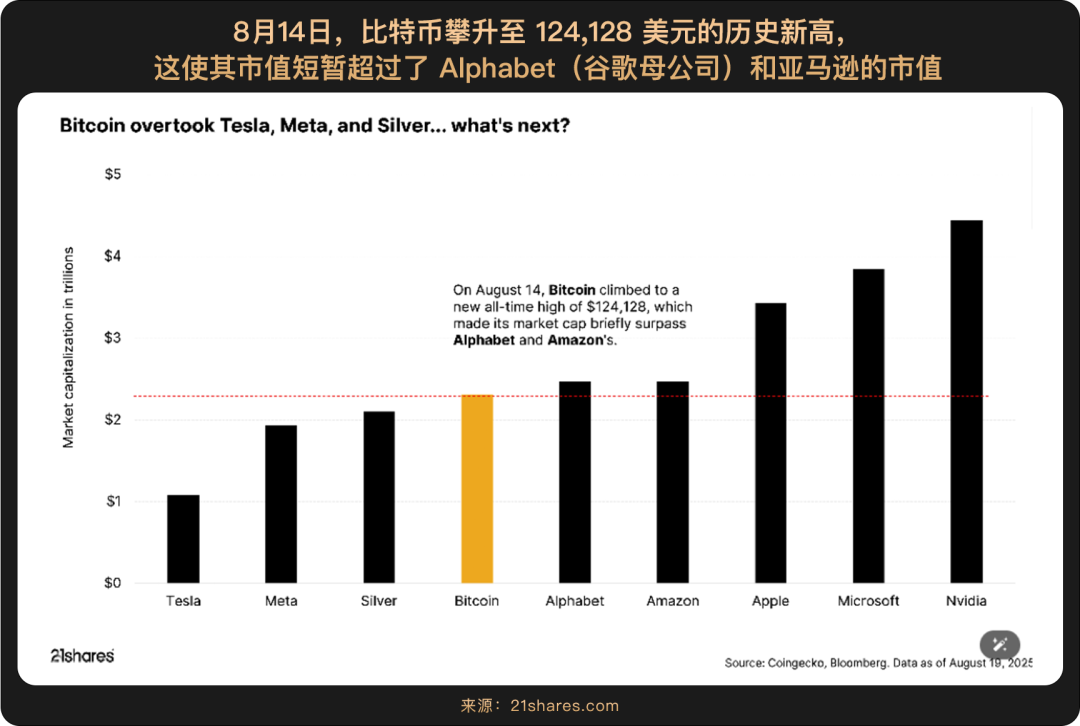

比特币市场在2025年8月又展现出了前所未有的成熟度。

一方面,据摩根大通分析,比特币六个月滚动波动率已从年初的近60%暴降至约30%,创下历史新低。与此同时,比特币与黄金的波动率比率也降至历史最低水平,这一变化大幅提升了比特币对机构投资者的吸引力。

而波动率的降低,主要归因于美国现货比特币ETF等受监管投资工具吸引了大量机构资金,其持有量已占比特币总供应量的6%以上,以及企业财库持续配置比特币(即DAT风潮),这些因素共同“锁定”了部分流通供应,减少了市场浮动筹码。

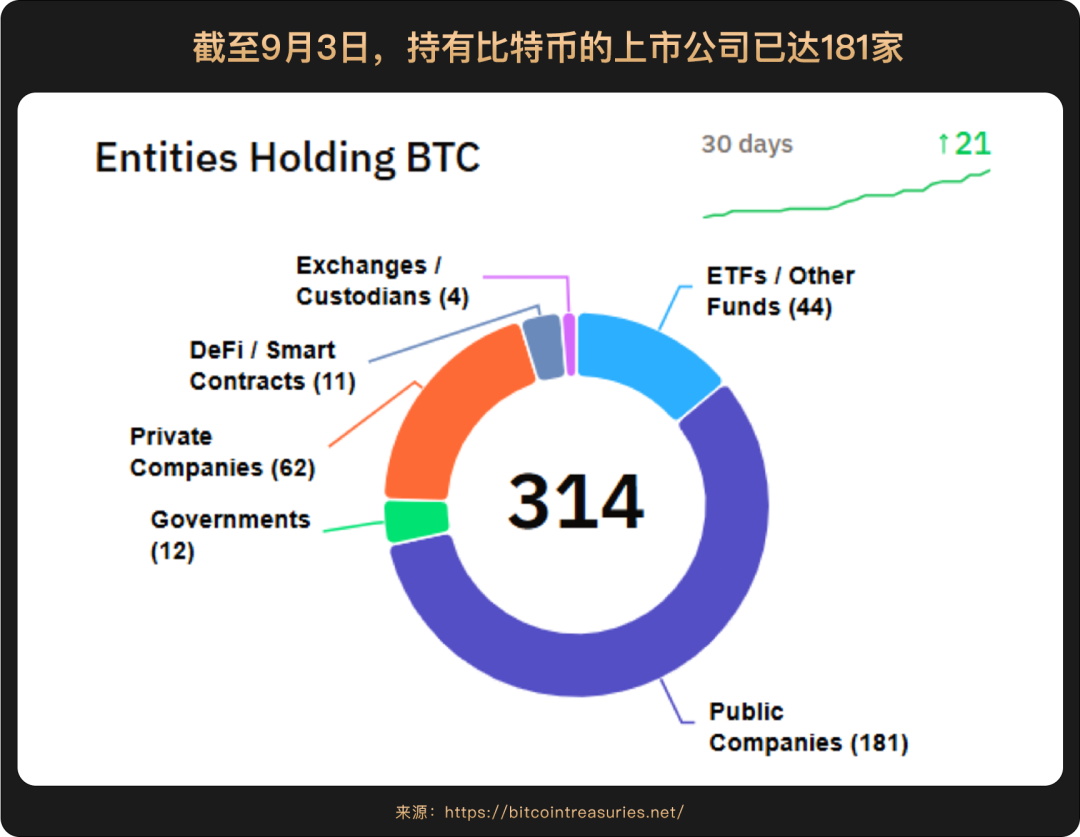

DAT(Digital Asset Treasury,数字资产财库)浪潮在8月持续深化,其核心是上市公司和机构将比特币等加密货币作为战略储备资产,尤其是上市公司,这些大公司的资本配置从投项目转向资产负债表持币,即用自己的资产负债表为加密货币“背书”,不仅为市场提供了持续的购买力,成了市场上最强大的买家之一,也为币价带来强有力的支撑。而对于公司来说,以Strategy(MSTR)为例,只要公司市值比账上比特币的实际价值高,就有机会通过定增、发可转债、卖优先股等方式从市场融资,然后用这些资金购买更多比特币,这么一来,公司就能以更少的成本囤到更多的币。统计数据显示,截至8 月中旬,2025 年DAT 累计融资已超 150 亿美元,显著高于同期加密 VC 规模,头部机构将DAT 视为 ETF 的替代 / 补充方案,强调流动性与弹性优势。今年的Bitcoin Asia 2025(香港)活动上,DAT趋势也成为行业热议的TOP话题。

与此同时,政策面的利好仍在持续。比特币作为唯一被正式纳入主权储备的加密资产,其全球监管框架也日益清晰,例如美国《CLARITY法案》的通过和SAB 121会计指引的废除,为银行等传统金融机构直接持有比特币铺平了道路。这也推动了其他国家,如挪威和捷克,考虑将比特币纳入其外汇储备。美国总统特朗普在8月正式签署行政命令,允许401(k)退休账户投资比特币等数字资产。这一举措为美国规模高达12.5万亿美元的退休金体系打开了进入加密市场的大门。市场分析认为,即便仅有1%的退休资金进行配置,也能为市场带来上百亿美元的潜在增量需求,其带来的长期购买力不容小觑。

值得一提的是,8月份加密市场内部出现了显著的资金轮动。比特币ETF遭遇了显著的资金外流,净流出逾20亿美元。而以太坊ETF则吸引了大量机构资金,净流入约40亿美元。这反映了部分投资者在比特币创历史新高后,转向挖掘以太坊等生态的增长潜力。然而,轮动节奏也很快,8月底以太坊ETF也出现了1.646亿美元的大幅流出,显示市场情绪存在短期波动。

尽管资金短期轮动,但顶级金融机构的持续入场,意味着加密货币已正式被纳入传统金融生态。据彭博,贝莱德比特币现货ETF 在 2025 年第二季度吸引了多家全球顶尖金融机构入场,从对冲基金、做市商到大型银行,持仓规模遍布自营资金与代客资金。摩根大通分析指出,基于风险调整后的估值,比特币的“合理价格”应在12.6万美元左右,显示其相较于黄金存在潜在上涨空间。

简而言之,8月无论是比特币波动性的显著下降、机构采用模式的演变还是内部资本轮动的加速,都意味着加密市场正在经历深刻的结构性转变。短期资金流向仍会有所波动,但支撑加密货币长期价值的制度基础和宏观动力已日益稳固。

长期来看,在降息周期提振风险偏好、加密生态持续完善的背景下,比特币的核心资产的韧性,仍将持续吸引资金流入,市场轮动带来的短期波动,反而为看多资金提供了更好的布局机会。