From 'Stablecoin First Stock' to 'Ankle Cut' in Stock Price: Why Circle Quickly Fell from the Spotlight into a Revaluation Cycle

From "Stablecoin Unicorn" to "Ankle-Cut" Stock Price: Why Circle Quickly Fell from Its Peak into a Revaluation Cycle

Circle, the issuer of the USDC stablecoin, experienced a dramatic stock price decline shortly after its IPO in June, dropping from an initial peak of around $260 to approximately $88. This reflects a broader market shift from hype-driven optimism to a more rational reassessment of the stablecoin industry.

Multiple factors contributed to this sharp correction. Initially, the stock was significantly overvalued due to market enthusiasm for the "first stablecoin stock" and the high-interest environment that boosted the appeal of its reserve-backed revenue model. As early investors took profits and sentiment cooled, a price correction was inevitable.

Increased competition is also pressuring Circle. While USDC is the world's second-largest dollar stablecoin, it faces growing challenges from new stablecoin projects and digital dollar initiatives from traditional financial institutions. The sector is shifting from an oligopoly to intense competition, raising investor concerns about USDC's future growth certainty.

Furthermore, macroeconomic interest rate trends pose a fundamental risk to Circle's business model. Its core revenue comes from interest earned on the cash and short-term U.S. Treasuries backing USDC. Expectations that the Federal Reserve may begin a rate-cutting cycle could directly compress this income. Rising operational and distribution costs further squeeze profitability.

Analysts hold divergent views on Circle's future. Firms like Mizuho have turned bullish, upgrading the stock and suggesting the sell-off related to its post-IPO lockup expiration may have created a buying opportunity. They point to USDC's continued adoption by mainstream financial institutions. Conversely, analysts at firms like Susquehanna remain pessimistic, maintaining an "Underperform" rating. They warn that lower future interest rates and potential underperformance in USDC growth could continue to pressure the stock price and have lowered their price target.

The upcoming end of the post-IPO lockup period, which restricts insiders from selling shares, has added near-term selling pressure, but this is viewed by some as a temporary overhang. Circle's recent Q3 earnings report, which beat expectations for both revenue and profit, shows that these fundamental concerns have not yet materialized, leaving the company's trajectory highly dependent on future interest rates and its ability to maintain and grow USDC's market share amidst fierce competition.

cointelegraph_中文2 min fa

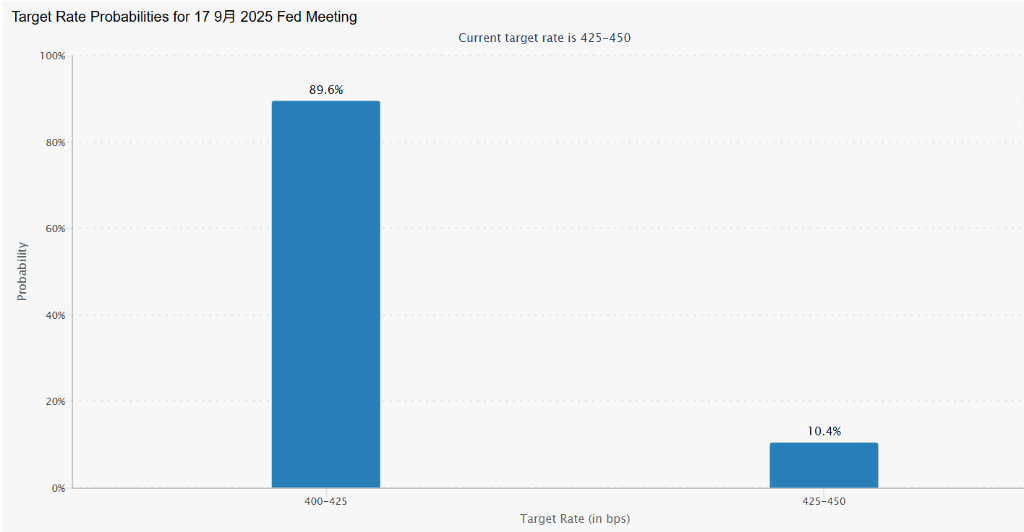

(9月降息25基点概率高达89.6%)

(9月降息25基点概率高达89.6%)