原创 | Odaily星球日报(@OdailyChina)

作者 | Asher(@Asher_ 0210 )

HyperSwap:Hyperliquid 生态头部 DEX

HyperSwap 是 Hyperliquid 生态上原生 DEX,当前 TVL 近 8000 万美元,每日交易量在 5000 至 6000 万美元,其产品愿景为将 DeFi 的精髓引入 HyperEVM 链、为生态系统用户提供无需许可的高效工具等。

目前,HyperSwap 仍在进行积分活动,包括 HyperSwap 积分与忠诚度积分,用户可通过在平台组 LP 活动积分奖励博未来代币空投。

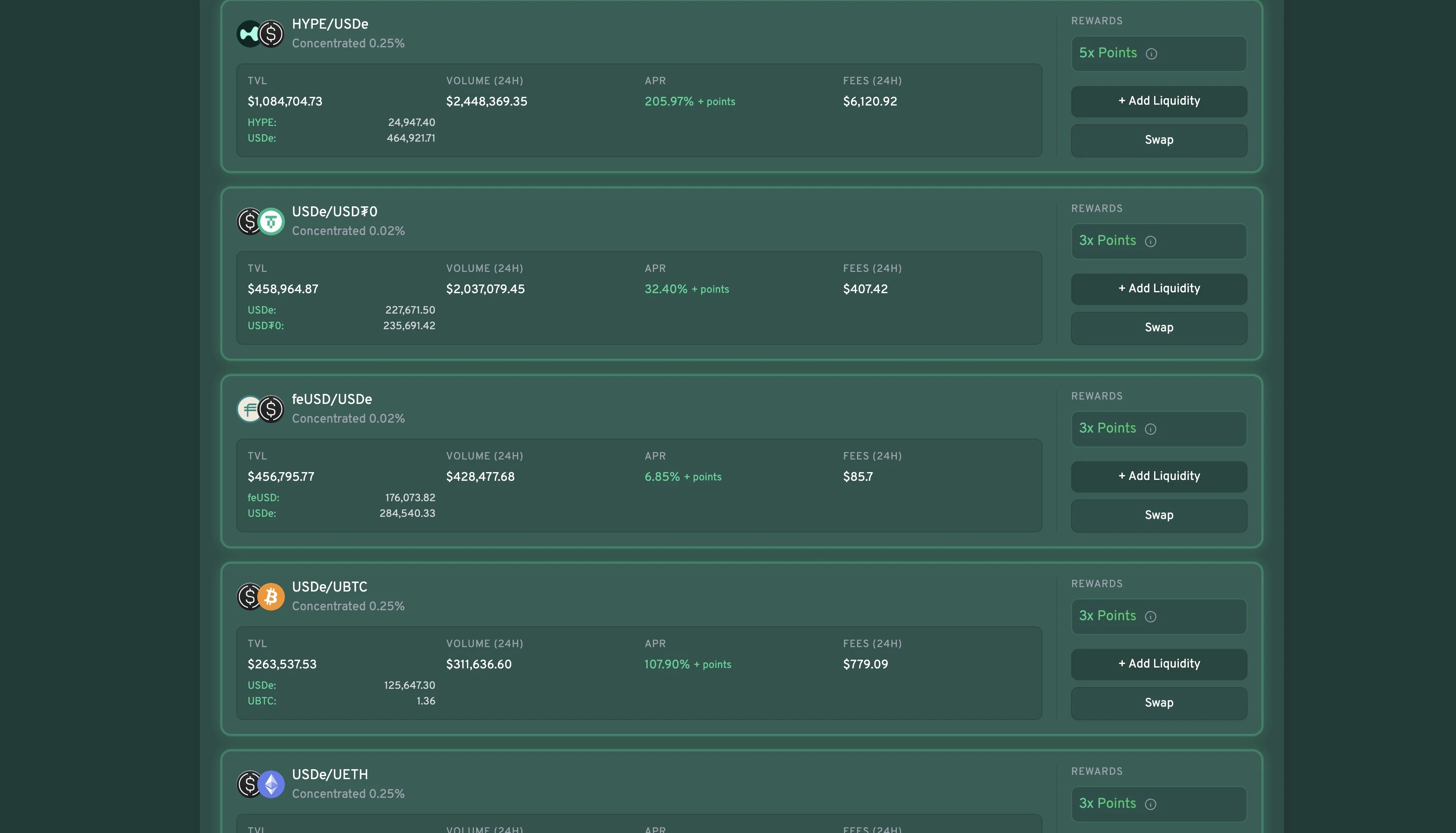

Kittenswap:Hyperliquid 生态头部 DEX

Kittenswap 为 Hyperliquid 生态上的头部 DEX,当前 TVL 超 3000 万美元,每日交易量在 1000 至 2000 万美元。用户可以在平台提供代币流动性获得对应的积分奖励,博未来的代币空投,为了鼓励用户参与,Kittenswap 官方计划将代币空投的比例从 30% 提高至 35% 。

积分活动示意图

目前,Kittenswap 积分活动已结束,其他积分相关活动或将在近期公布,值得关注。

Unit:Hyperliquid 生态跨链项目

Unit 是 Hyperliquid 上的跨链项目,支持多种资产的无缝存取,目前支持加密资产如 BTC、ETH、SOL、FARTCOIN 在 Hyperliquid 及其原生区块链之间流动。使用 Unit,Hyperliquid 用户可以:

将 BTC、ETH、SOL、FARTCOIN 从个人钱包或交易账户直接存入 Hyperliquid;

在 Hyperliquid 的现货订单簿上交易、转移或以其他方式利用这些主要资产以及现有资产;

将资产直接提取到相应资产的原生区块链上的地址。

根据社区反馈,Unit 或将在近几个月发币,因此可在其平台存取款 BTC、ETH、SOL、FARTCOIN 四种资产,或在 Hyperliquid 交易这四种资产的现货买卖。

Felix:Hyperliquid 生态头部 DeFi 项目

Felix 是一个部署在 Hyperliquid L1 上的 DeFi 协议,致力于为用户提供安全、低摩擦、风险可控的流动性释放与收益获取方式,平台目前提供两大核心功能模块:

CDP 市场:这是一个基于 Liquity v2 架构设计的借贷系统,用户可以通过抵押资产(如 BTC、HYPE)铸造平台原生稳定币 feUSD。该市场通过聚合 feUSD 借款人和稳定池存款人,形成一个稳定的货币市场;

Vanilla 市场:这是一个实时撮合资产出借人与抵押借款人的市场,与 CDP 模块不同,Vanilla 市场不设固定利率、不提供赎回机制,借贷利率完全由资金利用率自动调整,市场化程度更高。

目前 Felix 正在开展积分激励活动。用户不仅可以通过抵押资产铸造 feUSD 稳定币获取积分,也可以将 feUSD 存入平台稳定池赚取额外积分,用于未来空投或其他奖励机制。

HypurrFi:Hyperliquid 生态头部 DeFi 项目

HypurrFi 是一个专注于提供去中心化金融借贷和收益增值服务的平台。HypurrFi 允许用户存入原生 Hyperliquid 资产并借入 USDXL 以获取杠杆收益。其应用的主要功能包括稳定收益、质押资产赚取收益、借贷与循环操作等。致力于将波动的收益稳定为以 UST 为支撑的稳定币 USDXL,目前平台 USDXL 借款年利率为 16.18%。

具体参与 HypurrFi 交互的方式如下:

抵押借贷:将 HYPE 等资产作为抵押,借出平台稳定币 USDXL,需密切关注账户“健康度”,以避免因抵押比例过低而被清算;

金库存款:将手中的 USDXL 存入金库,不仅可以获得稳定收益,还能积累 HypurrFi 积分,用于未来奖励或活动兑换;

交易参与:在 HypurrFi 平台上进行代币兑换或其他交易操作,有助于提升个人账户的链上活跃度;

跨链交互:支持通过 HypurrFi 的跨链桥,将资产从其他链转入平台,参与更多生态玩法。

HyperLend:Hyperliquid 生态头部 DeFi 项目

HyperLend 是 Hyperliquid 生态中的借贷协议,当前 TVL 已超 3 亿美元,是整个 HyperEVM 生态中仅次于 Hyperliquid 的协议。目前参与交互的方式为:

参与平台借贷:存入 BTC、ETH 或 HYPE 等资产为平台提供流动性,可获得年化收益和积分奖励;

好友邀请获返佣:通过邀请码邀请好友,不仅可以获得返佣,还能获取邀请积分。

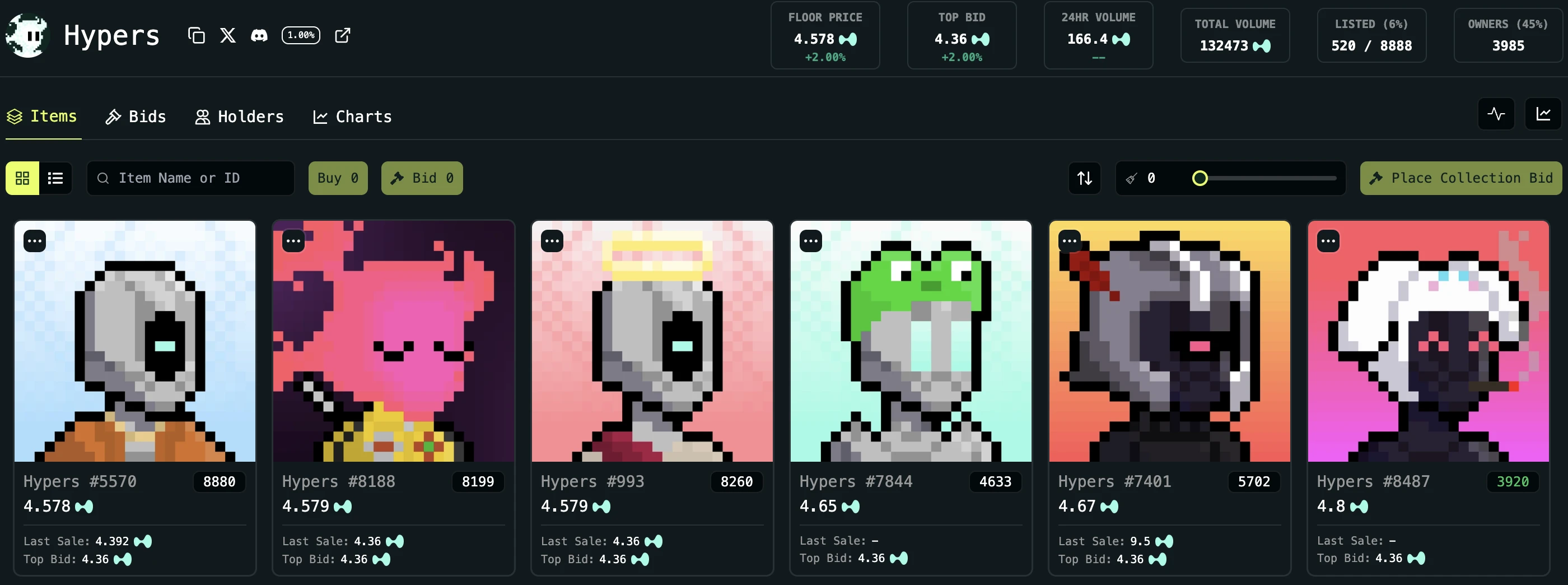

Drip.Trade:Hyperliquid 生态 NFT 市场

Drip.Trade 是 Hyperliquid 生态 NFT 市场,Drip.Trade 覆盖了 Hyperliquid 生态上 NFT 的全流程服务,从发行到交易一站式完成,目前几乎所有 Hyperliquid 生态上的 NFT 项目都是通过该平台发布的。目前参与交互的方式为:

买卖 NFT,刷交易量:通过 HYPE 代币在 Drip.Trade 买卖热门 NFT 来刷交易量;

持有官方 NFT 博空投:Hypers 是 Drip.Trade 的官方 NFT,目前 Hypers NFT 的地板价是 4.6 HYPE ,NFT 数量为 8888 个。

此外,忠诚度越高,积分加成越多,最高可达 100%。当用户拥有 100% 忠诚度、且有 25 枚 HYPE 的交易记录时,可以在平台内每天签到,玩转盘游戏赚取更多的积分。