热潮退去,衰退阴云笼罩

2025年初,美国金融市场从狂热走向不安。去年11月特朗普胜选时,投资者掀起“特朗普交易”热潮,憧憬他的减税和放松监管政策能延续经济繁荣,股市应声攀升。然而,这股乐观情绪迅速消退,取而代之的是对“特朗普衰退”的担忧。

纳斯达克指数遭遇2022年9月以来最大单日跌幅,技术股和银行股连日重挫,消费者的支出意愿以四年来的最快速度萎缩。法新社直言,金融市场与特朗普的“蜜月期”已结束。摩根大通将今年衰退概率从30%上调至40%,高盛从15%调整至20%,Polymarket上2025美国衰退的概率也来到了40%。

市场开始质疑:特朗普的政策是否正在将美国经济推向深渊?在这场风波中,所有人都在追问:美联储何时降息,才能为这场风暴按下暂停键?

关税与裁员:衰退的导火索?

特朗普上任不到两个月,政策已掀起波澜。他重拾关税武器,对加拿大、墨西哥、欧盟乃至中国提出10%到25%的加税计划,试图扭转贸易失衡并刺激制造业回流。

同时,马斯克领导的“政府效率部”裁减联邦雇员,仅2月就宣布裁员17.2万人,创2009年以来同期最高纪录,未来总数可能超过10万。这些举措让市场不安:企业成本上升,物价压力隐现,消费者信心摇摇欲坠。

亚特兰大联储预测,第一季度GDP增长将放缓,而历史规律显示,自1980年以来,美联储加息至5%以上后,2到4年内总有危机发生,如今正值2022年加息后的风险窗口。

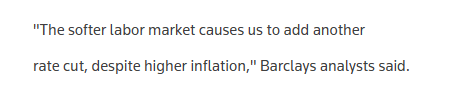

特朗普3月9日称:“这是转型期,我们在做大事。”然而,野村证券策略师却认为,他可能在有意制造衰退,以放缓经济增长并推动通缩。巴克莱最新预测也反映了这一趋势,预计美联储将在6月和9月分别降息25基点,相较此前仅预期6月降息一次,调整背后或是对通胀和经济放缓的更深忧虑。

债务压顶与美联储博弈

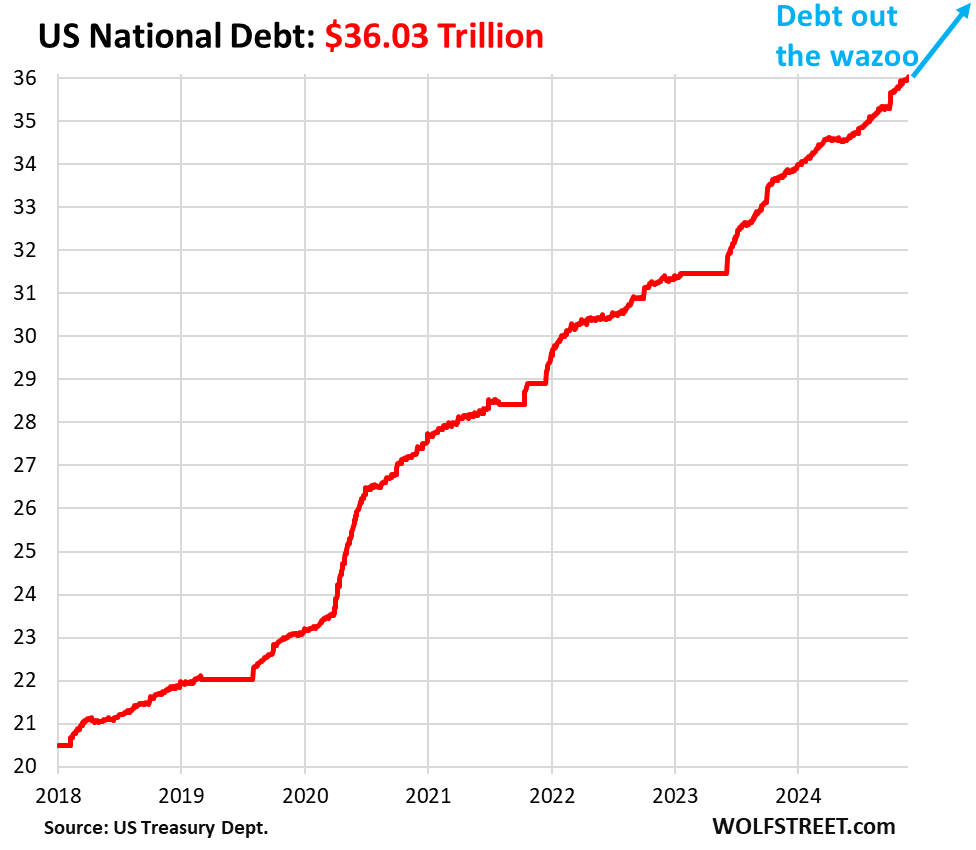

特朗普的政策或许瞄准了更深层的目标。美国联邦债务已达36万亿美元,利息支出成为财政重担。据国会预算办公室估算,2025财年利息成本将达9520亿美元,10年后可能飙升至1.8万亿美元。若美联储降息100基点,政府每年可节省3000到4000亿美元利息,这对特朗普而言是难以抗拒的诱惑。

他曾威胁撤换美联储主席鲍威尔,马斯克也在3月11日与他共同亮相白宫,宣布裁员计划的同时频频抨击货币政策。财政部长贝森特称经济需“排毒”,摆脱对政府支出的依赖,似乎在为短期阵痛铺垫。

目前,联邦基金利率维持在4.25%-4.5%,鲍威尔月初表示,通胀(CPI约3%)尚未降至2%,经济仍有韧性,无需急于降息。但劳动力市场已现裂痕,2月裁员总数翻倍,若失业率从4%升至5%,美联储可能被迫出手。市场猜测,6月或成降息起点,而巴克莱的预测进一步强化了这一预期,认为9月降息是对经济放缓的后续应对。

转型的代价与未知的风险

特朗普的野心可能远不止眼前。他的经济顾问史蒂芬·米兰提出,美国需重塑美元体系,摆脱储备货币的赤字拖累。他设想通过“海湖莊园协议”,迫使中国、欧盟抛售美元资产,转向长期债券,实现美元贬值并刺激制造业回流。若此计划成真,将重塑全球贸易格局,但前提是经济先“排毒”——主动刺破泡沫,降低杠杆。

3月11日,特朗普对百名企业高管说:“我们必须重建国家。”然而,这场转型代价高昂:股市下挫、美元走弱,甚至短期衰退,都可能是必经之路。

哈佛经济学家劳伦斯·萨默斯警告,衰退概率已近50%,通胀可能重回2021年高位;英国分析师达里奥·珀金斯则指出,真正衰退并非“净化剂”,而可能留下持久创伤。若失控,2026年中期选举的共和党前景将蒙上阴影。从“特朗普交易”到“特朗普衰退”,美联储的抉择至关重要——巴克莱预测的6月和9月降息能否实现,取决于通胀与就业数据的演变,而这场豪赌的成败,仍是未知数。