原文作者:雨中狂睡,加密 KOL

就像前情提要说的那样,这次的十月展望会非常简洁,只会详细聊我个人想要参与的 3-5 个代币,希望这种形式大家会喜欢(以前太散了,信息效率不高)。

TLDR: $UNI $SOL Berachain $TAO $WELL $ENA

市场的炒作一般分为两种模式,一种是人造叙事,这种叙事一般会推一个龙头代币走独立行情,比如 $SUI。另一种是创新的酝酿、出现和爆发。这种创新可能是一个好玩的 Ponzi,也可能是在很大程度上满足了市场需求的叙事,比如 $AXS(这一轮的 memecoin 算一个非典型案例)。

一般而言,第一种叙事浪潮会给到我们普通人更多的机会。这种大的创新往往诞生于宏观流动性外溢的情景下——资金对赚钱效应&资本效率有了更高的需求,需求推动创新的发生。

这一轮有一个很大的问题就是「没有出现像上一轮那样能够引导流动性进入和转移的叙事」,而流动性是资产定价的关键。叙事无法引导流动性,资产炒作也就很难起来。大家都在炒 meme,注意力也在 meme 上,只要有一些风吹草动,相关的 meme 就会迅速出现。但 meme 叙事也最容易让投资者感到疲倦,最终一地鸡毛。

那么币圈还有机会吗?

我觉得是有的,至少币圈还是有几个主线叙事正在并行发展的。

意图抽象&链抽象

这个叙事最终想要达成的目的就是「让用户和流动性以一种低门槛和无感的方式进入和参与 Crypto」,看起来前景是一片光明。但这个不是 Ponzi,大概率不会出现批量的财富机会。

本质上这些炒作还是基于「币圈用户觉得这个叙事能够为他们带来新的接盘侠」这个思路进行的。但它最终能否为币圈带来大量的真实用户和流动性,这里我们还是得打个问号。

而这个叙事的核心催化剂在于 $UNI v4 的推出。

Uniswap v4 的推出相当于是一个将市场注意力引向这个叙事的催化剂。未来在这个叙事发展的过程中,前端可能会成为最受市场青睐的炒作标的,而类似 Uniswap v4 这样的「基础设施层标的」,以及「流动性交互层标的」次之。但在最开始,机会最大的应该还是 $UNI。同时,类似概念的 $COW $1INCH 应该也会有对应的机会。

Layer 1 竞争

在当前市场中,Layer 1 竞争是最为主流的叙事,没有之一。

在这个周期中,市场炒作的主线是 Solana,并且还会时不时会蹦出一条其他 Layer 1 来与 Solana 竞争一下。

比如之前的 $AVAX,Avalanche 是通过「炒 meme」和「官宣与顶级公司的 PR」来推动代币价格增长的。现在的 $SUI 也是一个道理,他们是通过「OTC 交易来让英文 CT 们喊单(存疑,不确定)硬造一个新叙事」、「memecoin 炒作(现在 Sui 上也有一些不错的财富效应)」以及「用 $SUI 代币来激励流动性(类似于 Arbitrum)」来吸引市场注意力和提升流动性粘性的。值得一提的是,Sui 上的 DeFi 收益率还是不错的。

现在很多 Layer 1 都开始尝试利用 memecoin 来吸引市场的注意力和流动性,不过最终收效甚微(比如 BSC)。

因此,我觉得 Layer 1 的你方唱罢我登场大概率是短期事件。这些 Layer 1 搞事情,短期参与肯定可以获利——因为你的行为匹配了项目方的需求。

另外一种 Layer 1 玩法是 Fantom 的 Rebrand——搞一个性能更好的链进行品牌升级。区块链如果一开始没人玩,那就用未来空投的预期做激励。本质上,它与之前 Layer 2 的玩法类似,新意不高,但是在空投前是有效的。

要说看好的 Layer 1 ,我这里的名单是:Solana $SOL 和 Berachain。

看好 Solana 的原因很简单,只要看看在 Binance 上谁家的大市值 memecoin 数量更多就可以了。memecoin 就是一条 Layer 1 的王牌。

而 Berachain 的 PoL 是这个周期 Layer 1 共识机制中唯一的大型创新,引入了用户、节点和项目方的动态博弈。同时他们也在积极地用透明、去中心化和公平的方式扶持生态项目。我深度参与了 Berachain 的生态,所以奶一奶,DYOR。

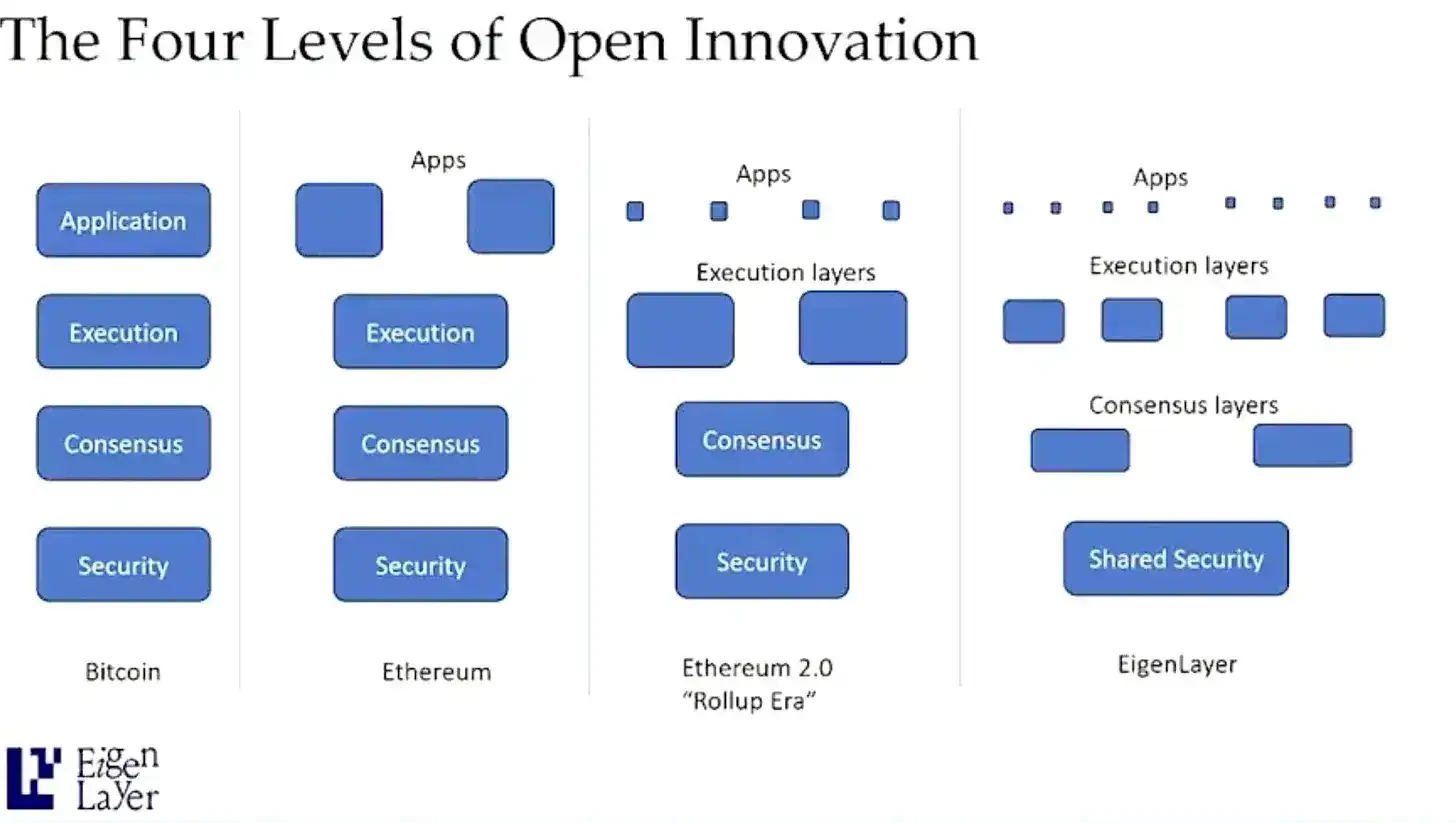

除了基础的 Layer 1 竞争外,我也很喜欢模块化叙事,模块化是这轮周期被讨论比较多的新叙事。其实看下面这张图就好了。

不过模块化标的又有些一言难尽。本来我是想奶 $EIGEN 一口,却没想到 $EIGEN 出了黑客事件,引起了社区极大的反响。总而言之,我还是看好 $EIGEN,并且认为 $EIGEN 有可能吸血其他模块化项目,在 Q4 的某个时期有一波价格上的表现(真正要大规模炒起来,估计要下一个周期了)。

AI

AI 叙事无需多提,看 OpenAI 最近的操作即可。以及,之前 AI 代币还会跟英伟达股票。最近 Crypto AI 赛道中表现最好的代币就是 $TAO,要选标的就选最强的。AI 代币的炒作与基本面无关,我们重点还是要关注 AI 行业的变迁。(中国 TAO $NMT 也可以关注一下,不过它的炒作是 $TAO 后面的事情了)关键词是「在大盘回调期间的价格表现」与「合适的时间节点」。

这类炒作会延续到 AI 泡沫破裂前。在破裂前,我们能做的只有享受泡沫。

稳定币竞争和 DeFi

当前稳定币赛道的竞争愈发激烈,比如 Paypal 的入局,Binance 转头去扶持 FDUSD,贝莱德也在积极布局稳定币赛道,Coinbase 在 Base 上 USDC 和欧元稳定币。

在这种激烈竞争下,目前能供我们炒作的主要是 Sky(原 MakerDAO)、 $LQTY 和 $ENA 这三个代币。

Sky 是最古老的去中心化稳定币项目,最近正在推进其治理代币和原生稳定币的转型。很明显,Sky 希望降低降息对于项目产品的影响,从「使用 RWA 收益激励采用」转型到「使用代币激励采用」的模式。后面,Sky 会通过发 SubDAO 的形式来开新盘子,以维持项目稳定币的采用规模。财富机会肯定会有,不过现在社区并不买单 Sky 最近的操作。我也看到了社区的一些负面言论。

另外,就像神鱼老师所说的,降息肯定会提升 DeFi 的竞争力。DeFi 赛道,包括以太坊和 Solana 的 DeFi 都有机会。简而言之就是哪个 Layer 1 链上活动高,TVL 高,哪个链上的 DeFi 项目代币就越受青睐。后面,对高收益的需求可能也会催生出新的盘子。不过那是大牛市的事情了,我们走一步看一步呗。

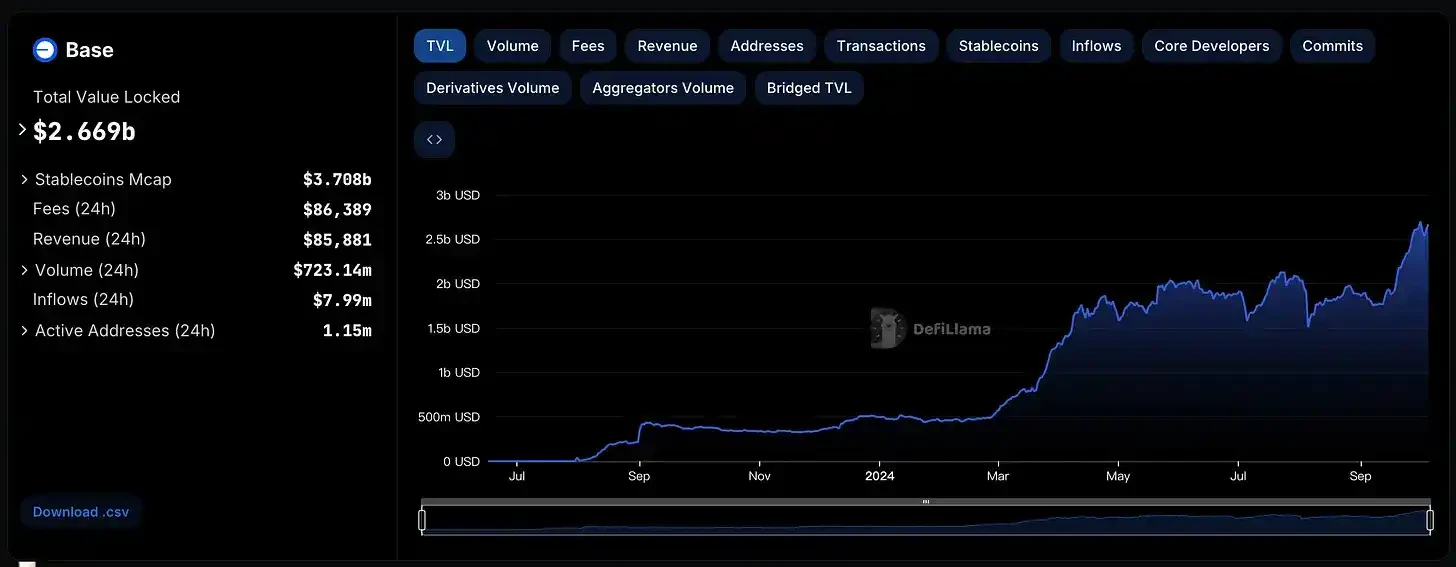

这里我想单独提一下以太坊 Layer 2 Basechain。Base 最近表现很好,TVL 在 9 月涨了很多,基本面的增长会带来新的财富机会。这里我们需要明确 Coinbase 做 Basechain 的需求:Base 能够拓展 Coinbase 在加密行业的影响力,还能够为 Coinbasse 带来排序器收入。Base 好,Coinbase 就会受益,那么 Coinbase 就完全有动力去推动 Base 生态的持续增长(之前拉盘 $AERO 也是这个道理)。

目前 Coinbase 在推的是什么?

cbBTC。

Moonwell 和 Aerodrome 将会是 cbBTC 增长的主要场所。目前,Moonwell 已经推出 cbBTC 流动性挖矿补贴。拉盘 $WELL 就能够推动更多的 cbBTC 采用(个人观点)。

$LQTY 有 v2 的预期(11 月),也是社区认可的去中心化稳定币。Sky 的转型本身对 $LQTY 来说就是利好,这也是它在前段时间涨势凶猛的原因之一(我个人的观点)。行业变迁的影响和预期的即将兑现可能会影响到 $LQTY 未来的价格表现。

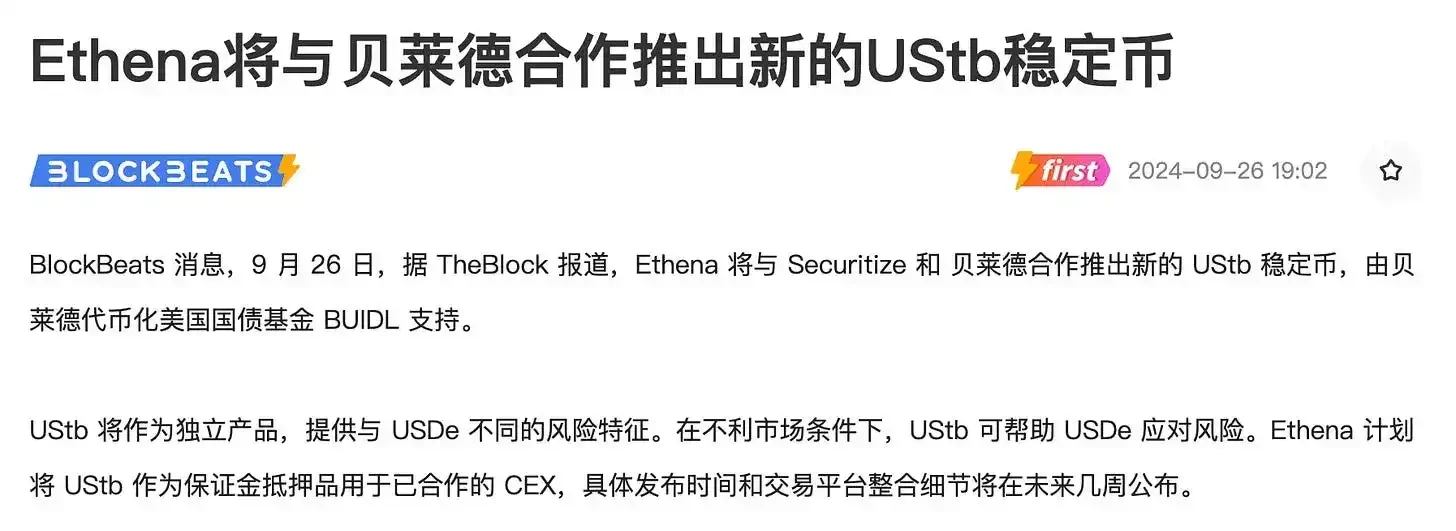

而 $ENA 的竞争力在于:「这个周期出来的新型稳定币」和「与贝莱德合作推出新的 UStb 稳定币」。这个合作形式的影响力要比那些参与贝莱德 Buidl 基金的项目大很多,深度合作是最好的催化剂。$ENA 最近的空投和解锁应该会给到我们入场的机会。

其他看好的代币分别是 $PENDLE 和 $BANANA。$PENDLE 之前聊过多次了,最近在推 BTCFi,还有 v3 预期。$BANANA 可以参考 @BensonTWN 老板的这篇(写得很好):https://x.com/BensonTWN/status/1839664439093813397

游戏的话,会考虑 $PIXEL $PRIME $PIRATE,我个人认为我们不能以游戏板块的视角来看这几个项目,需要单独看这些项目对应的催化剂。

BTC 生态还需要再观察(核心需求还是在的,详情可以看我 metagame 那篇)。目前我们仍处于市场认为矿工需要链上活跃度以增加收入的阶段,期待 BTC 生态能有新盘子跑出来。但问题是,链上手续费激增大概率只会是短期现象,矿工喜欢归喜欢,但是市场不可能持续买单。

关于 memecoin 叙事,我个人认为主流 memecoin 会在流动性回归之后出现一波巨大的涨幅,$WIF $PEPE 机会最大。memecoin 无法预测,只能顺应潮流。总体来说,我还是看好 memecoin 这个赛道,且认为这个赛道会出现至少两个 10 B+ 市值的 memecoin,就像上轮的 $DOGE $SHIB。

最后,我们来扫一下十月会发生什么事情:

$JEWEL Colosseum PvP on Metis:不知道这俩项目能够擦出怎样的火花,不过 $METIS 确实走得不错;

$XRP ETF 和 SEC:我觉得有机会来个不错的反弹;

$STX Nakamoto Upgrade:对 $STX 是利好,大概率 Stacks 上也会出现不错的财富机会;

$DUSK Mainnet Launch:目前不会太关注这个赛道;

$AVAX Summit ( 16-18 Oct)$WLD "New World" with Sam Altman:也与 AI 行业相关;

$RENDER Migration Rewards End$TIA Unlock of $ 1.05 BJPY Interest Rate Decision

详情参考这篇:https://x.com/breadnbutter247/status/1840435197893857689