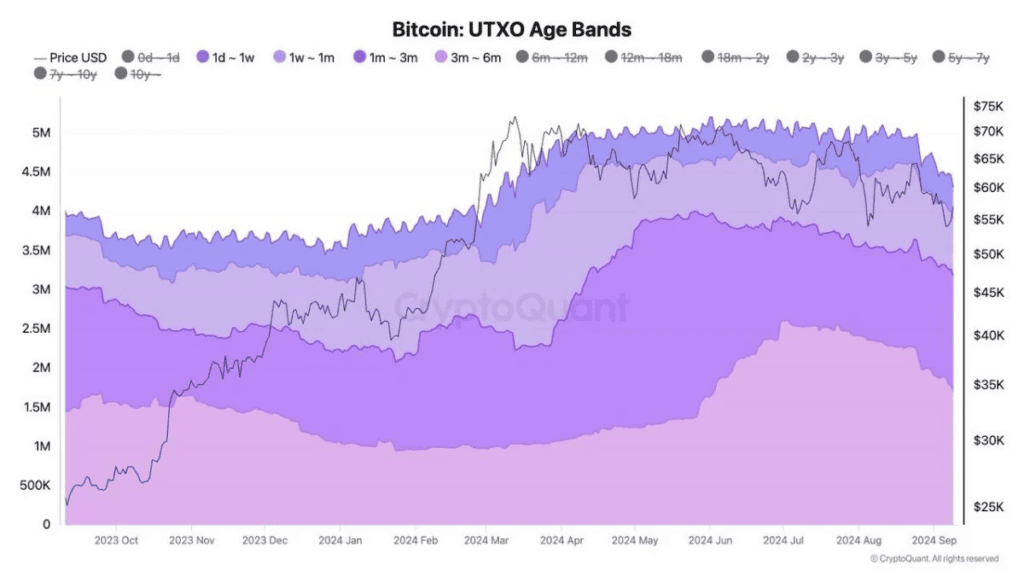

- Количество биткоинов, принадлежащих краткосрочным ходлерам, снижается с конца мая, заявил эксперт CryptoQuant.

- Однако долгосрочные владельцы продолжают увеличивать позиции.

Количество биткоинов, принадлежащих краткосрочным владельцам, снижается с конца мая 2024 года, что свидетельствует об ослаблении спроса на актив. Об этом в комментарии The Block заявил глава отдела исследований CryptoQuant Хулио Морено.

Он добавил, что долгосрочные ходлеры первой криптовалюты накапливают средства. По словам аналитика, если спрос на актив снова вырастет, «это приведет к тому, что краткосрочные владельцы будут покупать у долгосрочных».

Кроме того, Морено объяснил, что краткосрочные владельцы — это те, кто хранит биткоины менее 155 дней. По его данным, такие инвесторы значительно сократили свои позиции, особенно в июле и августе.

«Увеличение накоплений долгосрочными ходлерами может привести к стабилизации цен и подготовить рынок к потенциальному отскоку, тогда как распродажи со стороны краткосрочных держателей могут создать незначительное понижательное давление на цены биткоина. Данные показывают явное перетекание капитала из слабых рук в сильные руки, что свидетельствует о стабильности рынка», — говорится в сообщении.

Ранее в CryptoQuant заявили, что количество активных адресов в сети биткоина достигло минимума за 2024 год. Также эксперты заметили стремительный рост количества владельцев стейблкоинов Tether (USDT) на криптовалютных биржах.