作者:HANGRY

编译:深潮TechFlow

注:本文内容仅代表原作者观点,还请DYOR。

早上好,各位撸毛朋友!

有人可能会说,三位数的年化收益率时代已经结束,但他们只是不知道该去哪里寻找。

以下是我们本周推荐的卑微农场。

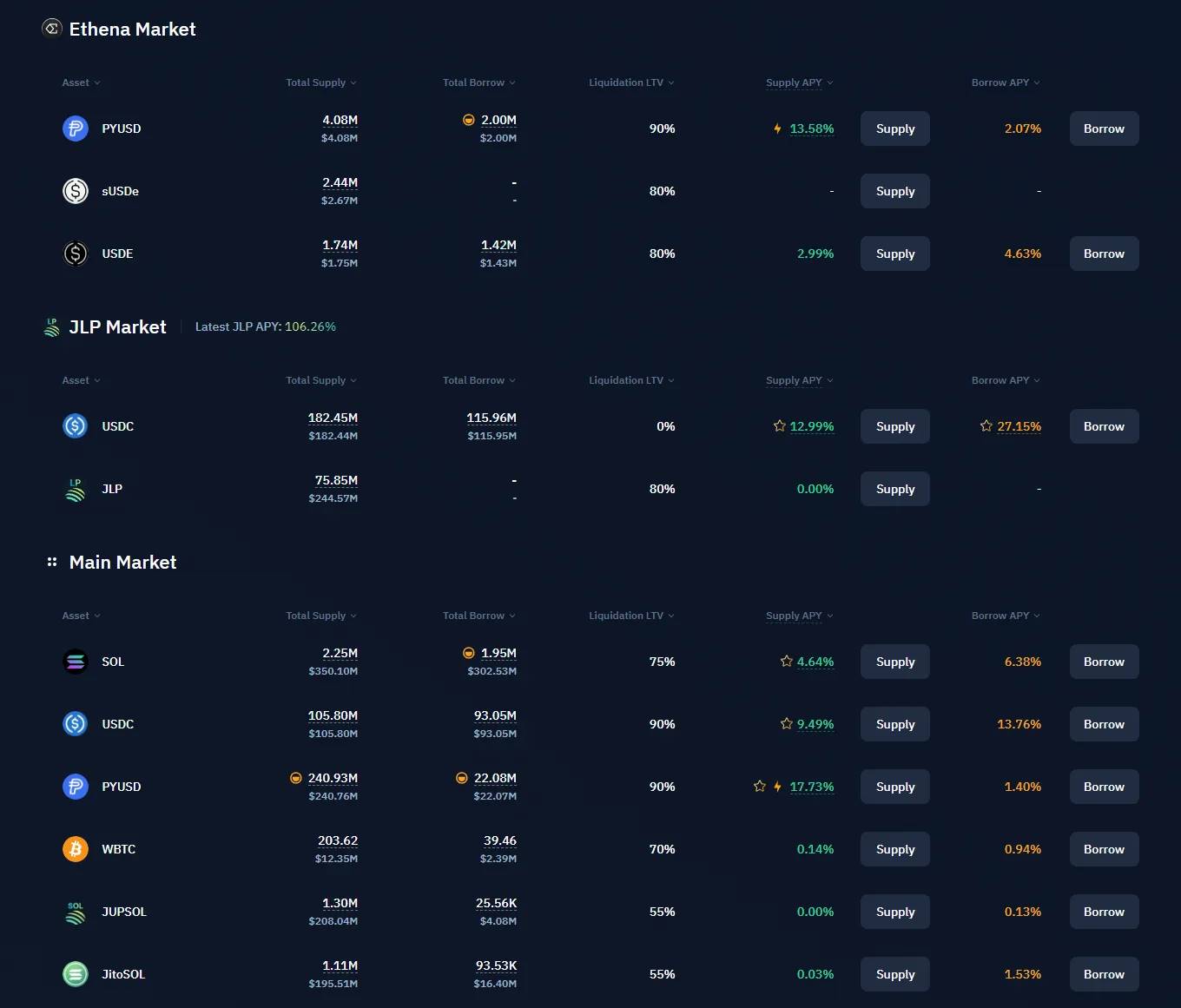

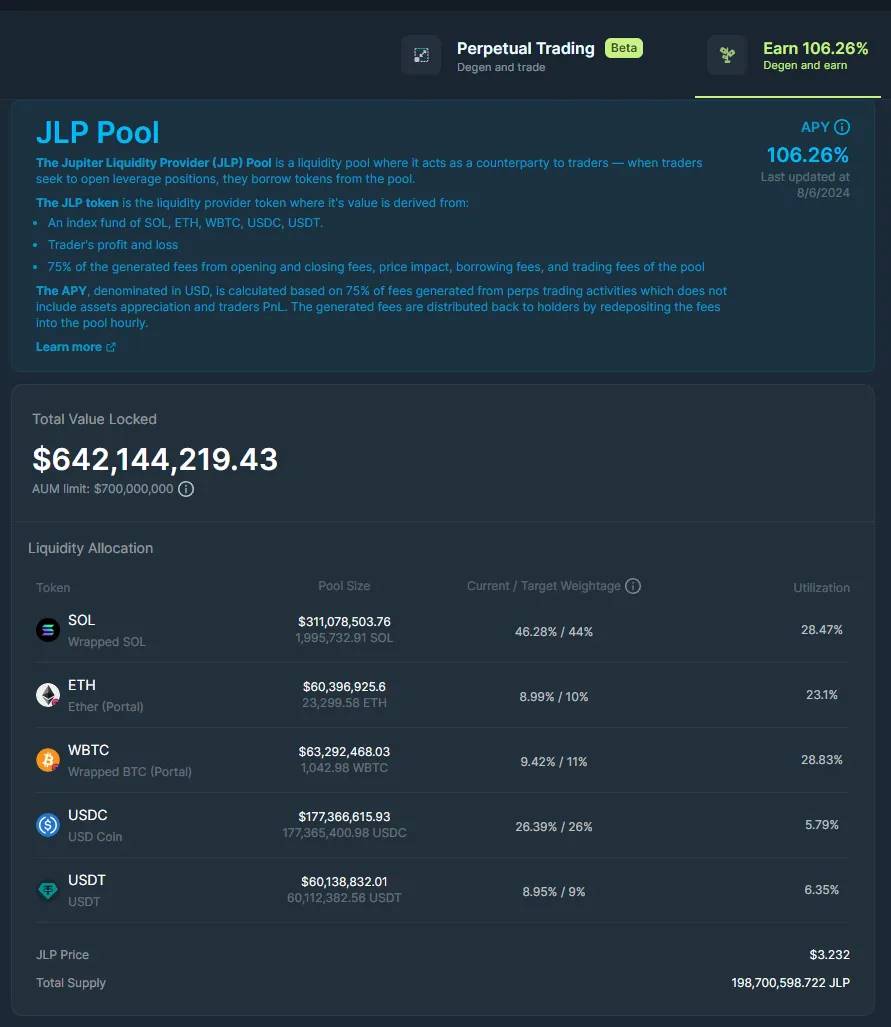

1. Jupiter

我们本周的第一个撸毛机会是 Jupiter,它是 Solana 上领先的 DEX 聚合器和永续交易所。

在过去的一年里,Jupiter 已经巩固了自己作为 Solana 上的蓝筹协议的地位,JLP 证明在市场波动期间是一个安全的避风港。

目前,流动性提供者(LP,Liquidity Provider)在保持对 BTC、ETH 和 SOL 等主要资产的敞口的同时,正在获得三位数的年化收益率。

除了收益,提供流动性还可能使您有资格参加 Jupiter 将于 1 月进行的下一轮空投。

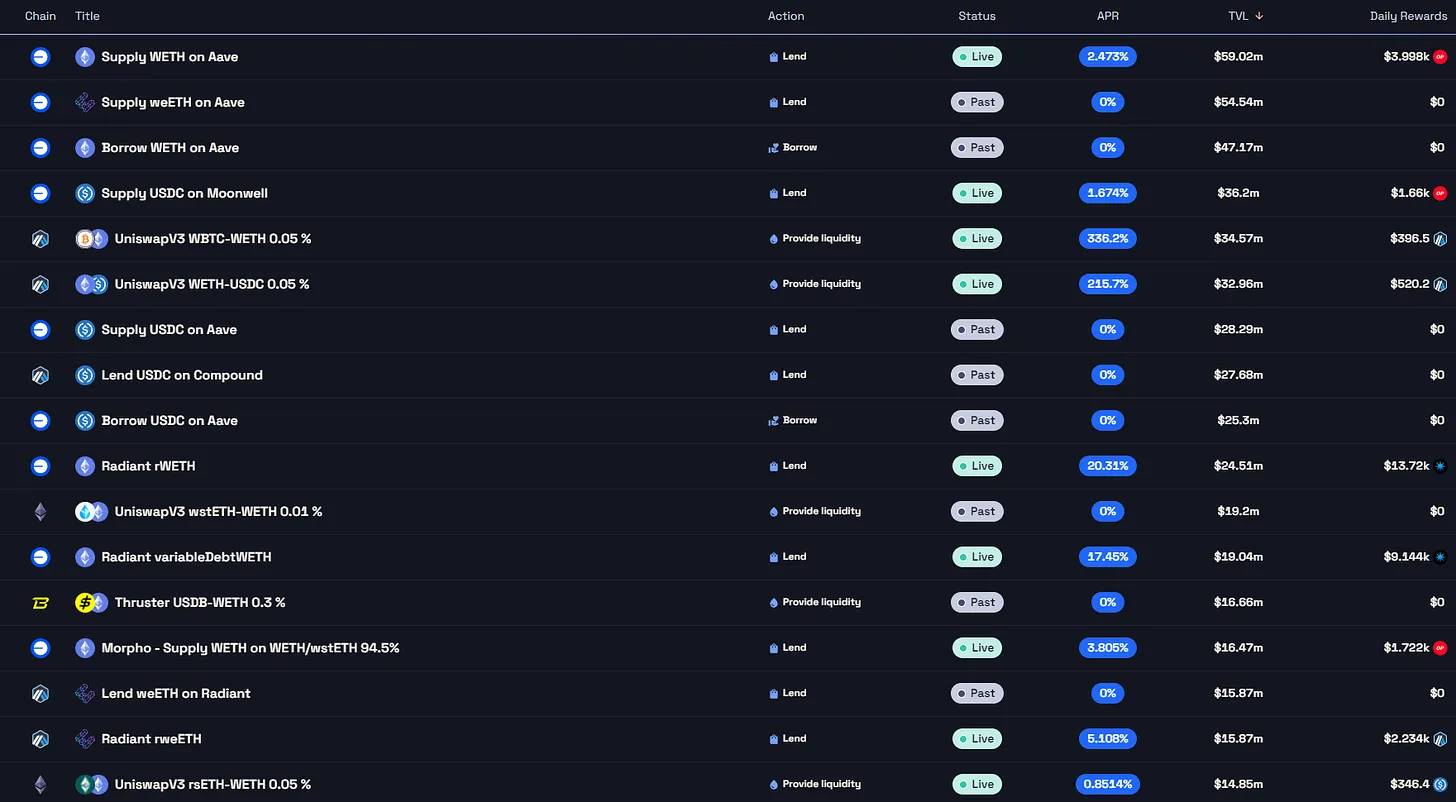

2. Merkl

接下来是 Merkl,这是一个奖励中心,旨在探索和分发跨各种链的流动性池(liquidity pools)的代币奖励。

Optimism Superfest 奖励正在通过 Merkl 分发,以及许多其他活动的激励。

在寻找新的流动性池提供流动性时,Merkl 是我们最喜欢的地方之一。

目前我们最喜欢的一些流动性池包括:

• tBTC/WETH @ 90% APR

• wBTC/uniBTC @ 31% APR

• wstETH/ezETH @ 25% APR

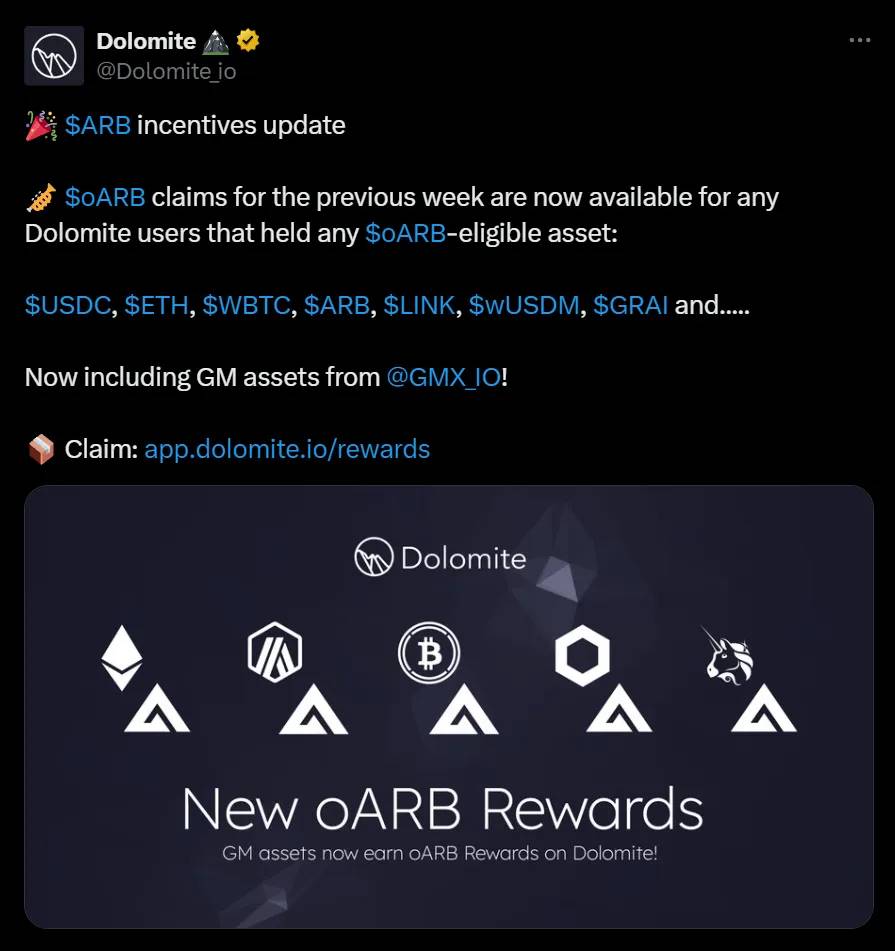

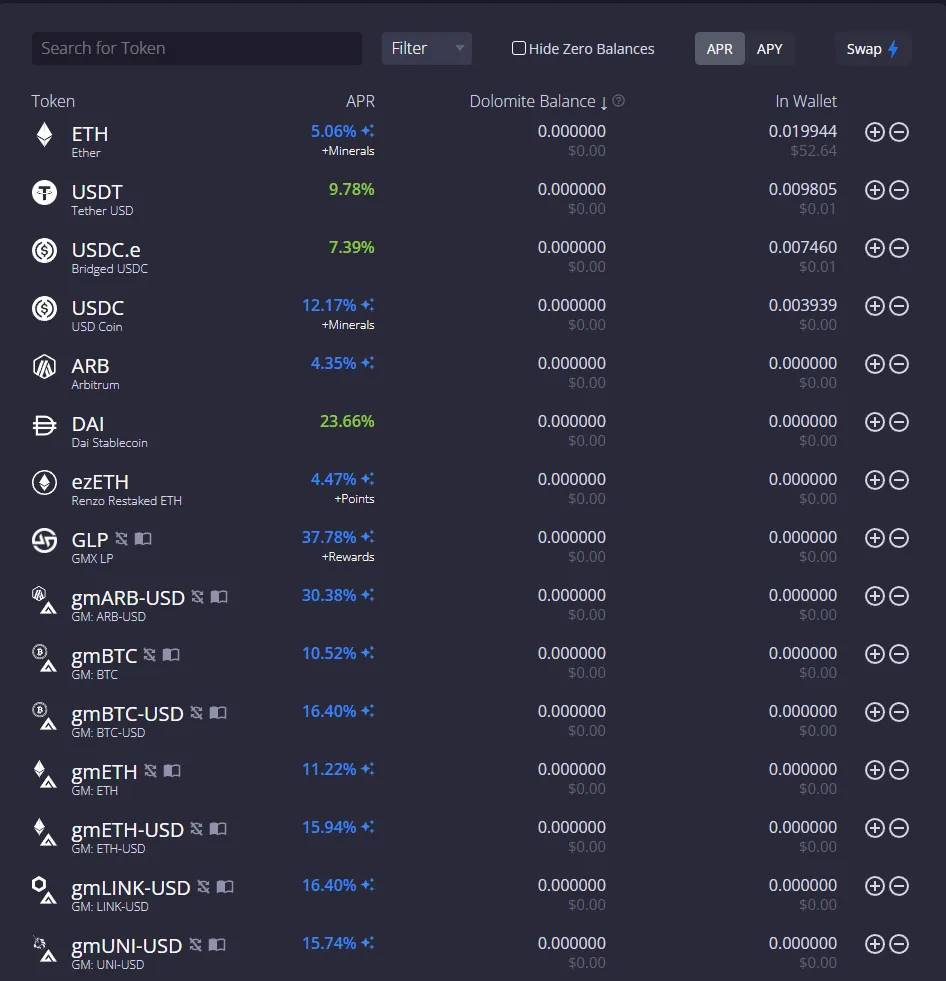

3. Dolomite

我们本周的下一个撸毛机会是 Dolomite,一个多链货币市场和保证金交易协议。

Dolomite 作为一个统一的平台,可以为您的代币赚取额外的收益,同时能够根据您的投资组合借入保证金。

通过 Dolomite,您可以在 Arbitrum 和 Mantle 上存入各种资产,以堆积收益、积分和 Dolomite 矿石。

存入 GLP、DAI 和 USDM 等资产目前的年化收益率在 20-40% 之间,同时允许用户根据其投资组合进行借款。

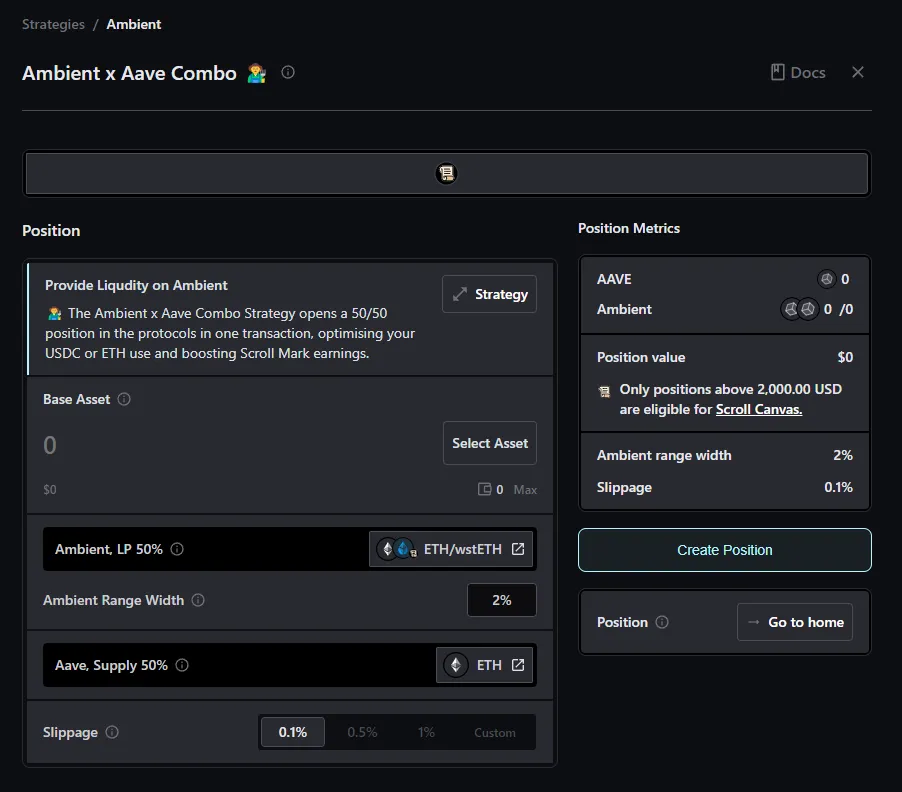

4. Brahma

接下来是 Brahma,这个平台旨在简化和整合去中心化金融的体验。

通过 Console,用户可以安全存放和管理他们的资金,同时获得对各种协议和一键策略的访问。

Brahma 刚刚推出了一种通过 Aave 和 Ambient 提高收益效率的 Scroll 策略,如果您正在进行 Scroll 农场操作,值得一试。

此外,用户在 Brahma 持有资产到本月底将获得额外的 ARB 激励。

5. Kamino

我们本周的最后一个机会是 Kamino,这是一个建立在 Solana 上的借贷、流动性和杠杆协议。

即使在代币上线后,TVL(总锁仓价值)也在持续增长,这得益于 Kamino 的积分计划和新产品的推出。

Kamino 提供了多种收益机会,从借贷到流动性提供,甚至是循环借贷。

以下是我们目前最喜欢的一些机会:

• JLP @ 285% APY(杠杆)

• pyUSD @ 83.2% APY(杠杆)

• sSOL/SOL @ 27.3% APY