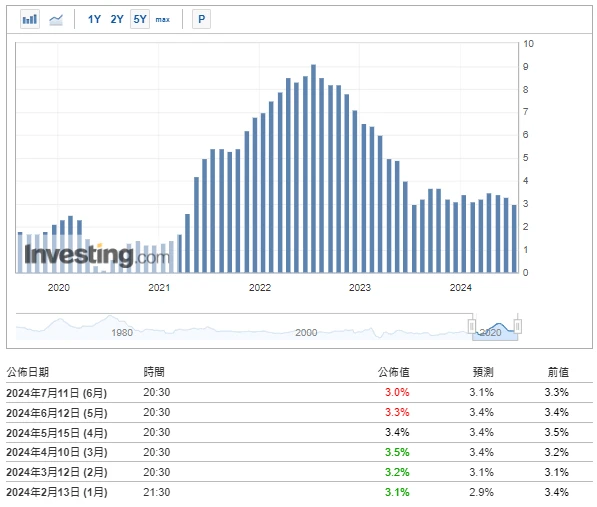

CPI 数据走低主流币价格冲高回落

数据来源: https://hk.investing.com/economic-calendar/cpi-733

年内降息预期大幅升温, 9 月首次降息的可能性回升至 80% , 7 月降息概率重现。比特币与以太坊价格在 CPI 数据公布前持续上涨,数据公布后冲高回落。美国劳工部公布的数据显示, 6 月份美国消费者价格指数(CPI)同比增速由 5 月的 3.3% 放缓至 3% ,为去年 6 月以来最低增速;环比由 5 月的持平,转为 6 月的下降 0.1% ,增速较上月回落 0.1 个百分点,为 2020 年 5 月以来的首次负增长,显示出通胀继续放缓的迹象。

距离下一次美联储议息会议(2024.08.01)还有约 17 天

https://hk.investing.com/economic-calendar/interest-rate-decision-168

市场技术与情绪环境分析

情绪分析组成

技术指标

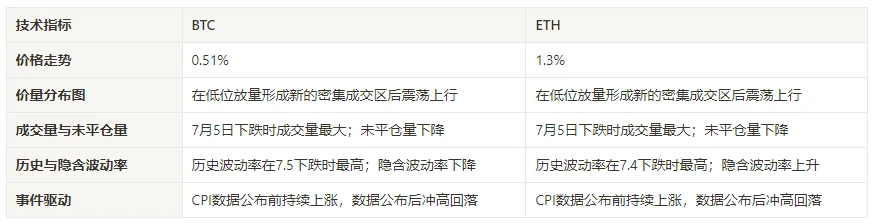

价格走势

过去一周 BTC 价格上涨 0.51% ,ETH 价格上涨 1.3% 。

上图是 BTC 过去一周的价格图

上图是 ETH 过去一周的价格图

表格显示过去一个周的价格变化率

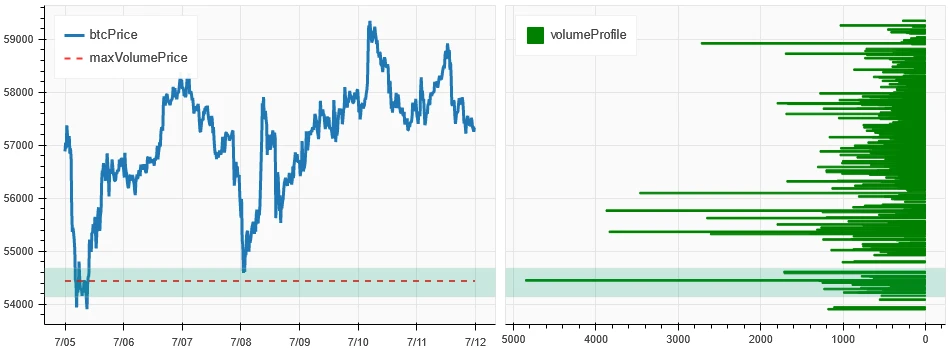

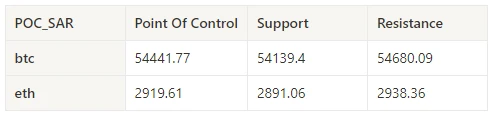

价量分布图(支撑阻力)

过去一周 BTC 与 ETH 在低位放量形成新的密集成交区后震荡上行。

上图是 BTC 过去一周的密集成交区分布图

上图是 ETH 过去一周的密集成交区分布图

表格显示 BTC 与 ETH 过去一周中每周的密集成交区间

成交量与未平仓量

过去一周 BTC 与 ETH 在 7 月 5 日下跌时成交量最大;未平仓量 BTC 与 ETH 都持续下降。

上图最上方 BTC 的价格走势,中间是成交量、最下方是未平仓量、浅蓝色是 1 天均值,橘色是 7 天均值。其中 K 线的颜色代表当前的状态,绿色是价格上升有成交量支持,红色是在平仓,黄色是在缓慢累积仓位,黑色是拥挤状态。

上图最上方 ETH 的价格走势,中间是成交量、最下方是未平仓量、浅蓝色是 1 天均值,橘色是 7 天均值。其中 K 线的颜色代表当前的状态,绿色是价格上升有成交量支持,红色是在平仓,黄色是在缓慢累积仓位,黑色是拥挤状态。

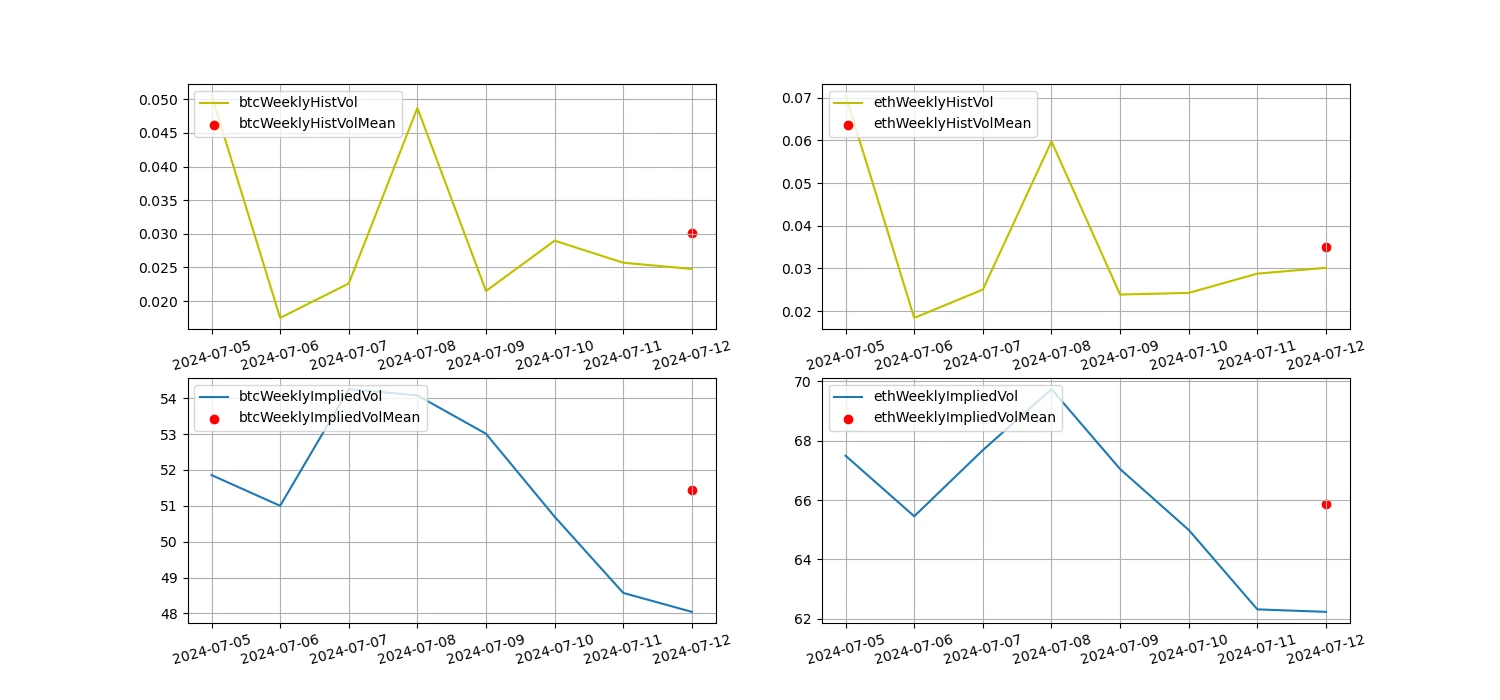

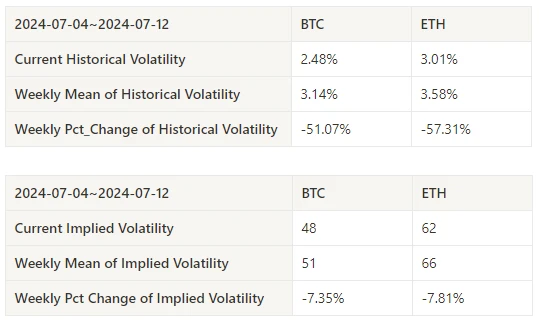

历史波动率与隐含波动率

过去一周历史波动率 BTC 与 ETH 在 7.5 下跌时最高;隐含波动率 BTC 与 ETH 同步下降。

黄色线为历史波动率,蓝色线为隐含波动率,红点是其 7 日平均

事件驱动

过去一周比特币与以太坊价格在 CPI 数据公布前持续上涨,数据公布后冲高回落。

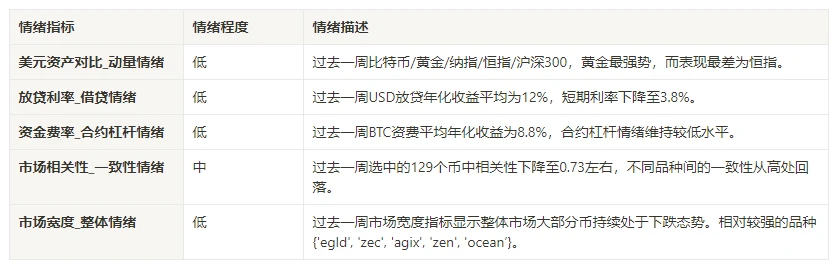

情绪指标

动量情绪

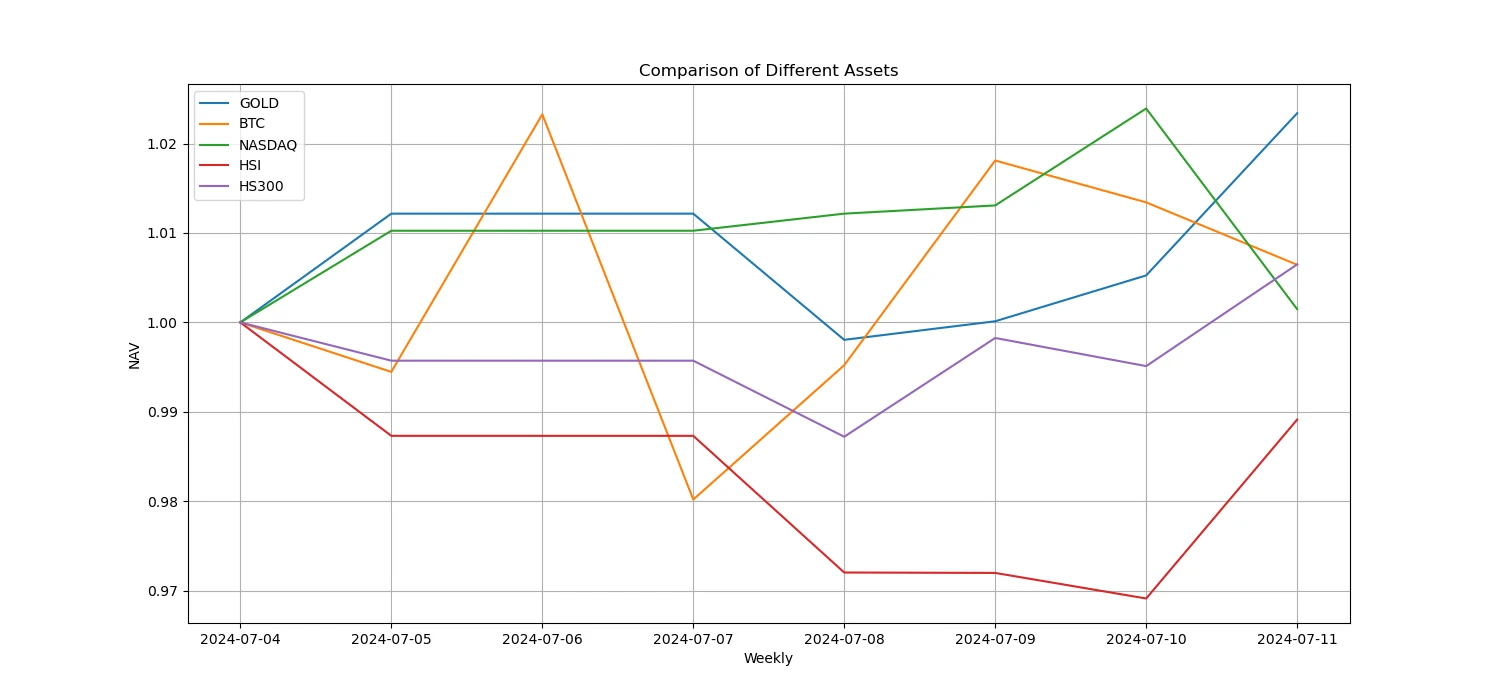

过去一周比特币/黄金/纳指/恒指/沪深 300 中,黄金最强势,而表现最差为恒指。

上图为不同资产过去一周的走势

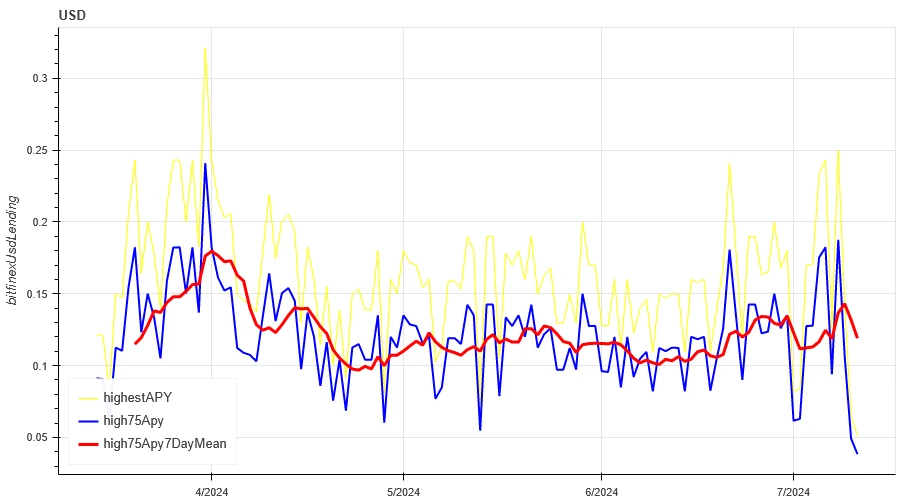

放贷利率_借贷情绪

过去一周 USD 放贷年化收益平均为 12% ,短期利率下降至 3.8% 。

黄色线为 USD 利率的最高价,蓝色线为最高价的 75% ,红色线为最高价的 75% 的 7 天平均值

表格显示 USD 利率过去不同持有天数的平均收益

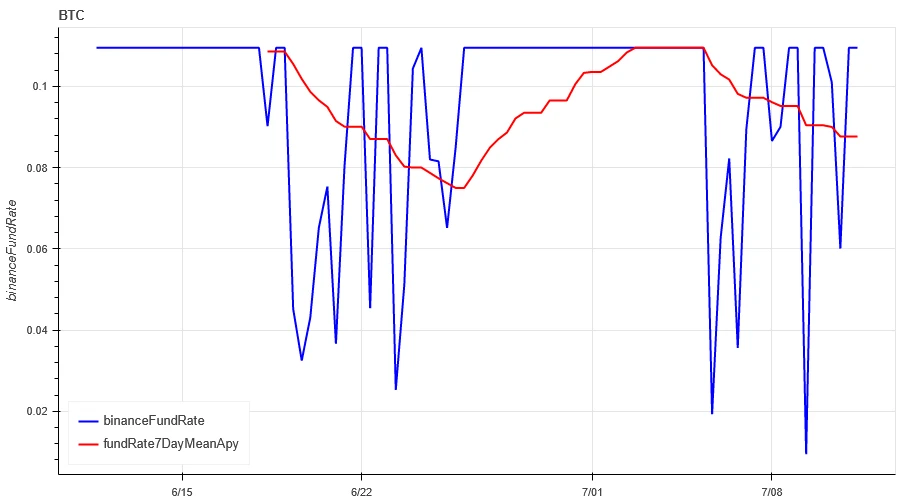

资金费率_合约杠杆情绪

过去一周 BTC 资费平均年化收益为 8.8% ,合约杠杆情绪维持较低水平。

蓝色线为币安上 BTC 的资金费率,红色线为其 7 日平均

表格显示 BTC 的资费过去不同持有天数的平均收益

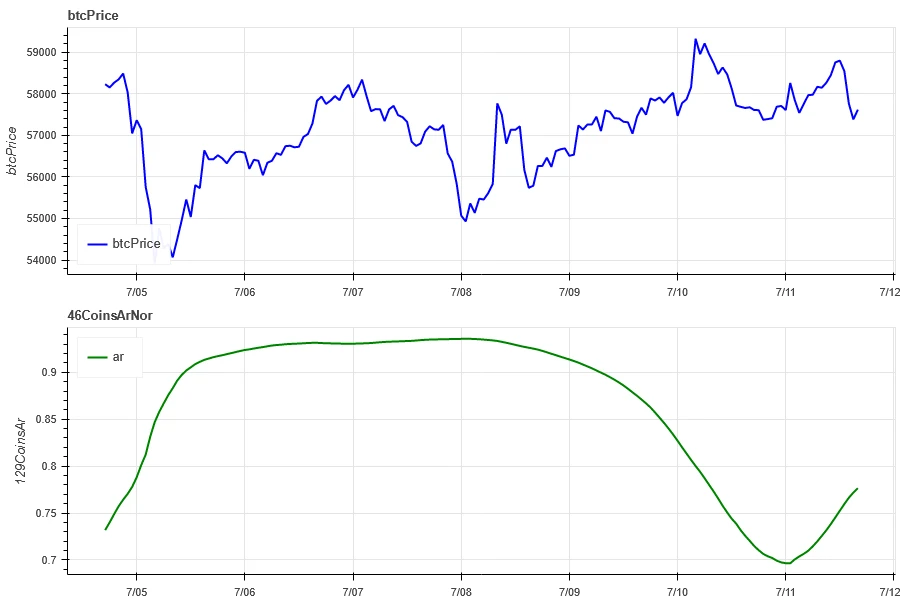

市场相关性_一致性情绪

过去一周选中的 129 个币中相关性维持在 0.73 左右,不同品种间的一致性从高处回落。

上图蓝色先为比特币价格,绿色线为['1000 floki', '1000 lunc', '1000 pepe', '1000 shib', '100 0x ec', '1inch', 'aave', 'ada', 'agix', 'algo', 'ankr', 'ant', 'ape', 'apt', 'arb', 'ar', 'astr', 'atom', 'audio', 'avax', 'axs', 'bal', 'band', 'bat', 'bch', 'bigtime', 'blur', 'bnb', 'btc', 'celo', 'cfx', 'chz', 'ckb', 'comp', 'crv', 'cvx', 'cyber', 'dash', 'doge', 'dot', 'dydx', 'egld', 'enj', 'ens', 'eos','etc', 'eth', 'fet', 'fil', 'flow', 'ftm', 'fxs', 'gala', 'gmt', 'gmx', 'grt', 'hbar', 'hot', 'icp', 'icx', 'imx', 'inj', 'iost', 'iotx', 'jasmy', 'kava', 'klay', 'ksm', 'ldo', 'link', 'loom', 'lpt', 'lqty', 'lrc', 'ltc', 'luna 2', 'magic', 'mana', 'matic', 'meme', 'mina', 'mkr', 'near', 'neo', 'ocean', 'one', 'ont', 'op', 'pendle', 'qnt', 'qtum', 'rndr', 'rose', 'rune', 'rvn', 'sand', 'sei', 'sfp', 'skl', 'snx', 'sol', 'ssv', 'stg', 'storj', 'stx', 'sui', 'sushi', 'sxp', 'theta', 'tia', 'trx', 't', 'uma', 'uni', 'vet', 'waves', 'wld', 'woo', 'xem', 'xlm', 'xmr', 'xrp', 'xtz', 'yfi', 'zec', 'zen', 'zil', 'zrx’]整体的相关性

市场宽度_整体情绪

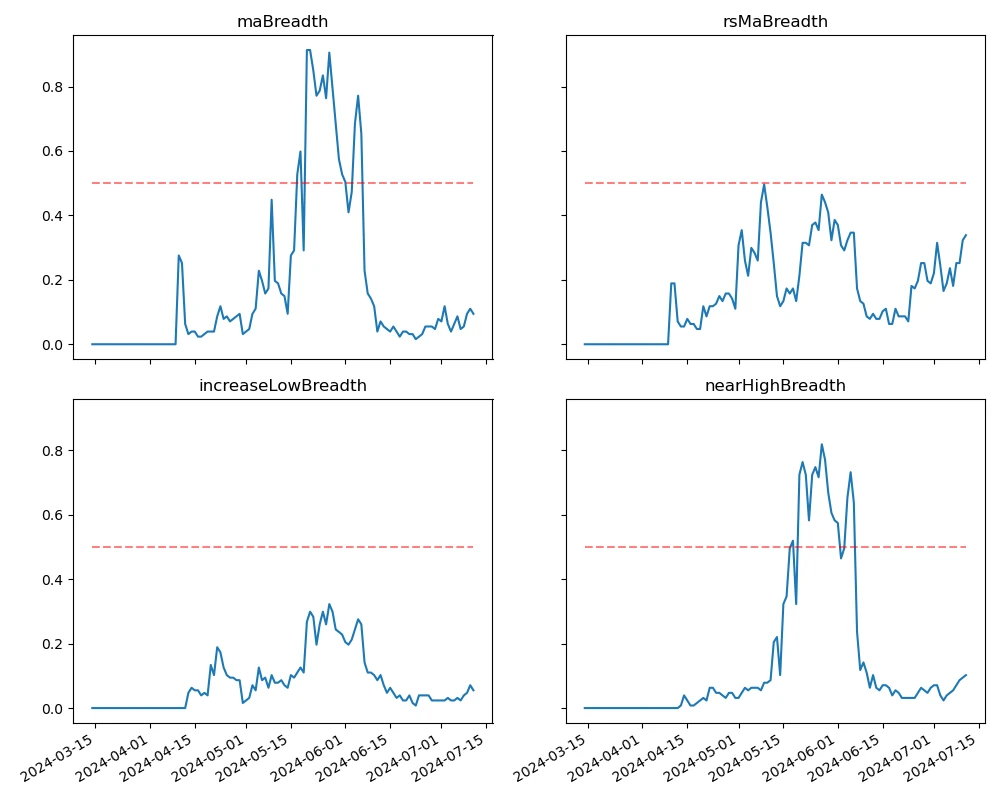

过去一周选中的 129 个币,价格在 30 日均线上方的占比为 9.4% ,相对 BTC 价格在 30 日均线上方占比为 33.8% ,距离过去 30 天最低价大于 20% 的占比为 5.5% ,距离过去 30 天最高价小于 10% 的占比为 10% ,过去一周市场宽度指标显示整体市场大部分币持续处于下跌态势。

上图为['bnb', 'btc', 'sol', 'eth', '1000 floki', '1000 lunc', '1000 pepe', '1000 sats', '1000 shib', '100 0x ec', '1inch', 'aave', 'ada', 'agix', 'ai', 'algo', 'alt', 'ankr', 'ape', 'apt', 'arb', 'ar', 'astr', 'atom', 'avax', 'axs', 'bal', 'band', 'bat', 'bch', 'bigtime', 'blur', 'cake', 'celo', 'cfx', 'chz', 'ckb', 'comp', 'crv', 'cvx', 'cyber', 'dash', 'doge', 'dot', 'dydx', 'egld', 'enj', 'ens', 'eos','etc', 'fet', 'fil', 'flow', 'ftm', 'fxs', 'gala', 'gmt', 'gmx', 'grt', 'hbar', 'hot', 'icp', 'icx', 'idu', 'imx', 'inj', 'iost', 'iotx', 'jasmy', 'jto', 'jup', 'kava', 'klay', 'ksm', 'ldo', 'link', 'loom', 'lpt', 'lqty', 'lrc', 'ltc', 'luna 2', 'magic', 'mana', 'manta', 'mask', 'matic', 'meme', 'mina', 'mkr', 'near', 'neo', 'nfp', 'ocean', 'one', 'ont', 'op', 'ordi', 'pendle', 'pyth', 'qnt', 'qtum', 'rndr', 'robin', 'rose', 'rune', 'rvn', 'sand', 'sei', 'sfp', 'skl', 'snx', 'ssv', 'stg', 'storj', 'stx', 'sui', 'sushi', 'sxp', 'theta', 'tia', 'trx', 't', 'uma', 'uni', 'vet', 'waves', 'wif', 'wld', 'woo','xai', 'xem', 'xlm', 'xmr', 'xrp', 'xtz', 'yfi', 'zec', 'zen', 'zil', 'zrx' ] 30 日的各宽度指标占比

总结

在过去一周,比特币(BTC)和以太坊(ETH)的价格在低位放量后震荡上升,同时这两种加密货币的波动率和成交量在 7 月 5 日的下跌到低点时达到了最高水平。比特币和以太坊的未平仓合约量都在下降。此外,比特币与以太坊的隐含波动率也同步下降。比特币的资金费率维持在低水平,这可能反映出市场参与者对比特币的杠杆情绪持续低迷。市场宽度指标显示大部分加密货币持续下跌趋势,表明整个市场在过去一周中维持疲软的走势。CPI 数据走低,数据公布时主流币价格冲高回落。

Twitter: @https://x.com/CTA_ChannelCmt

Website: channelcmt.com