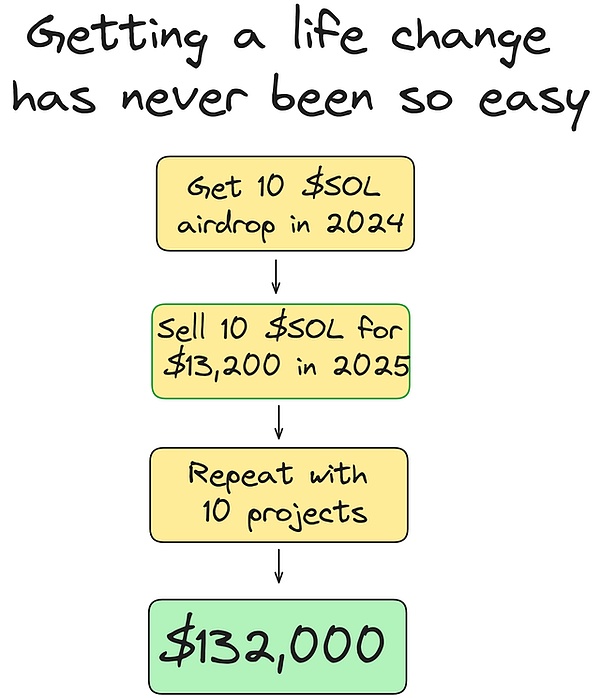

近期,随着市场对 SOL ETF 预期的高涨,越来越多的投资者开始关注 Solana 生态系统中的空投机会。预计一旦 SOL ETF 获批,Solana 的价值将大幅提升。这篇文章将深入探讨当前最值得参与的 SOL 空投项目,并提供详细的策略指导。

1. SOL ETF 的预期效应

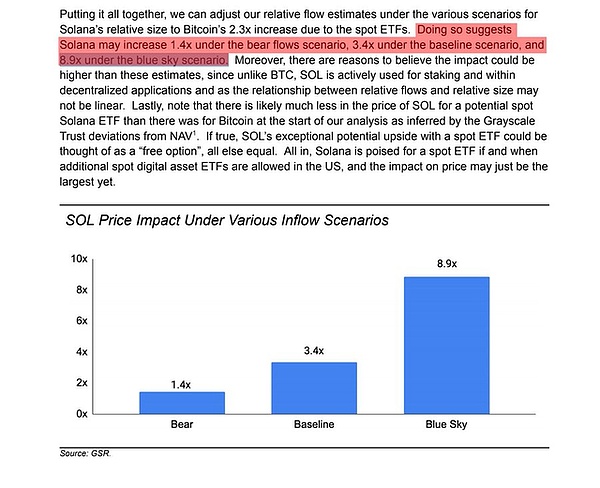

根据研究报告,SOL ETF 获批后,Solana 的收益将显著提升。在熊市条件下,预计收益可达 1.4 倍;在现有市场价格基础上,有望实现 3-4 倍的增幅;若牛市来临,收益甚至可达 8-9 倍。因此,目前参与 Solana 空投项目是一个极具潜力的投资机会。

2. 主要的 SOL 空投项目

Jupiter Exchange

Jupiter Exchange 是 Solana 上的主要流动性提供者和去中心化交易所(DEX)聚合器。目前,其第二次空投计划已确认,将空投 36 亿 JUP 代币,价值接近 33 亿美元。以下是具体策略:

交换策略:访问 Jupiter Swap,每天进行交换以增加交易量。

投票策略:购买至少 100 个 JUP 代币,访问 Jupiter Vote,质押并参与每次投票。

杠杆策略:前往 Jupiter Perps,选择带杠杆的货币对,定期开立多头或空头仓位。

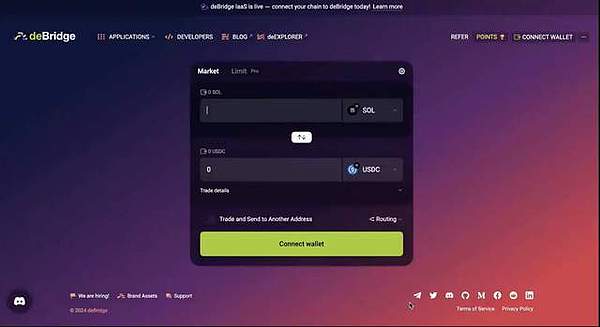

deBridge Finance

deBridge Finance 是构建在 Solana 上的 LayerZero 的竞争对手,通过积分系统奖励忠实用户,而非使用任何女巫标记。其空投策略如下:

交换策略:访问 deBridge,连接钱包并在不同网络之间交换代币。使用便宜的网络(如 Polygon、AVAX 等)来最大化收益。

Meteora

Meteora 是一个完全由 Jupiter 支持的平台,通过 DLMM 池提供 0% 滑点体验。其空投策略如下:

池策略:访问 Meteora,选择 JLP/USDC 池,将 50% 的存款金额兑换成 JLP 并创建池。

3. 参与空投的注意事项

了解项目:在参与任何空投之前,务必深入了解项目的背景、团队以及长期发展规划。

风险控制:不要在单个项目上投入过多资金,分散投资以降低风险。

定期监控:定期查看项目进展和市场变化,及时调整投资策略。

总体而言,随着 SOL ETF 的预期加持,Solana 生态系统中的空投项目为投资者提供了丰富的机会。通过合理的策略和风险控制,投资者可以在这一波市场浪潮中获取可观的收益。未来,随着市场的进一步发展和技术的不断进步,Solana 有望成为加密资产领域的又一重要支柱。让我们共同期待,并积极参与这些充满潜力的投资机会。