月末市场仍保持平静,欧洲方面延续了鸽派的步伐,西班牙 CPI 数据疲软,欧洲央行官员自豪地宣称,尽管工资上涨,央行仍能够“很快地”开始降息。同时,瑞典央行也表达了鸽派立场,进一步加剧了降息预期,市场预期欧洲央行在年底前将降息近 95 个基点(4 次),而对于美联储的降息预期则约为 76 个基点。

在美国方面,理事 Waller 在盘后发表谈话,延续其 2 月份的鹰派基调,他发表了诸如“经济情况没有给我们大幅降息的理由”以及“根据近期的数据,减少降息次数或是推迟降息都是合适的”等言论,然而,随著交易员开始为长周末做准备,美债收益率几乎没有受到影响,季末再平衡资金可能会主导明天的价格走势。

有趣的是,美国将在周五休市时发布 PCE 物价指数,华尔街预测核心 PCE 环比将放缓至 0.3% 以下,这将会是核心通胀年初小幅回升后一个良好的转变,不过投资者正在享受假期,并期待著第一季的出色回报,市场不太可能给予这个数据太多关注。

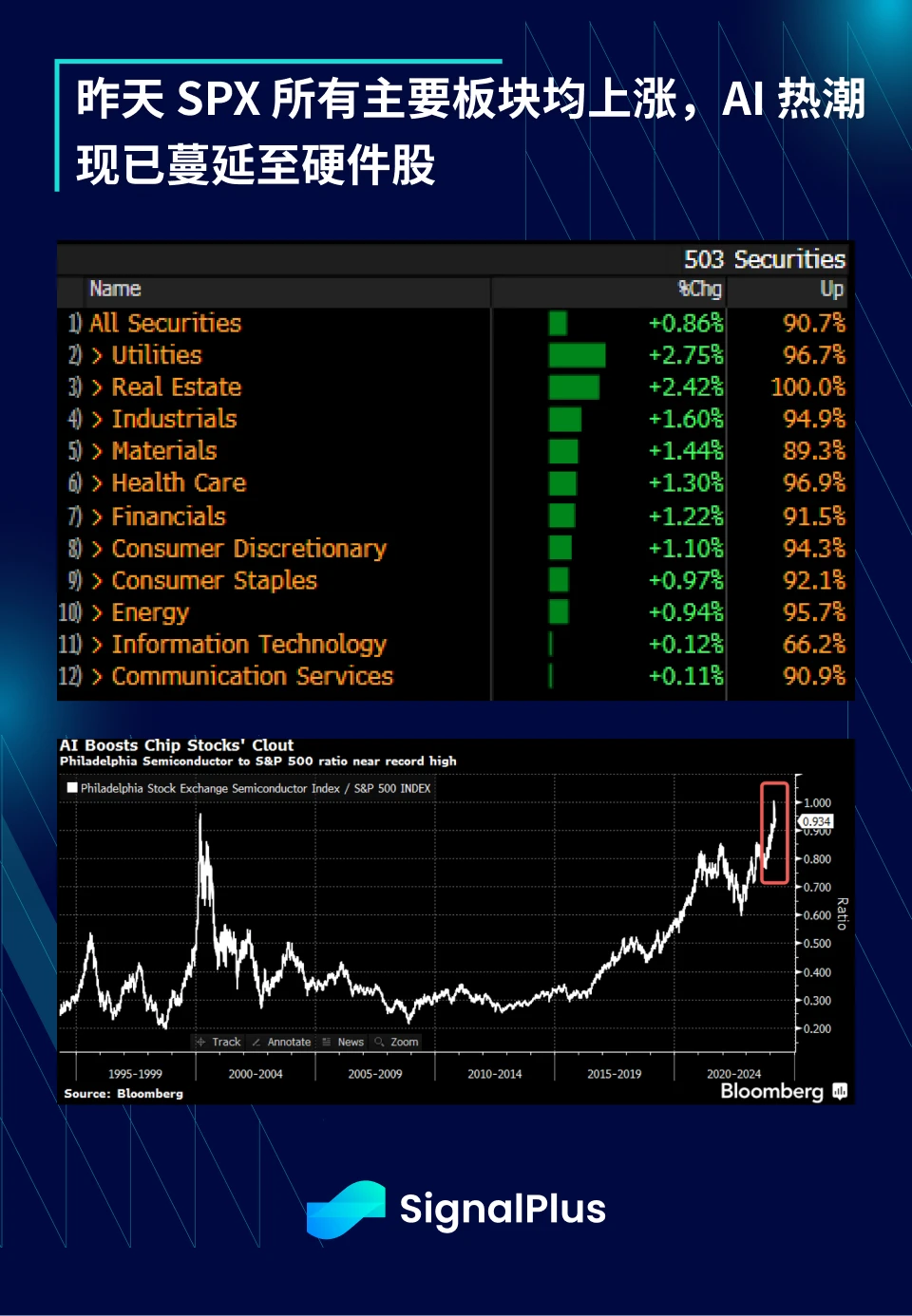

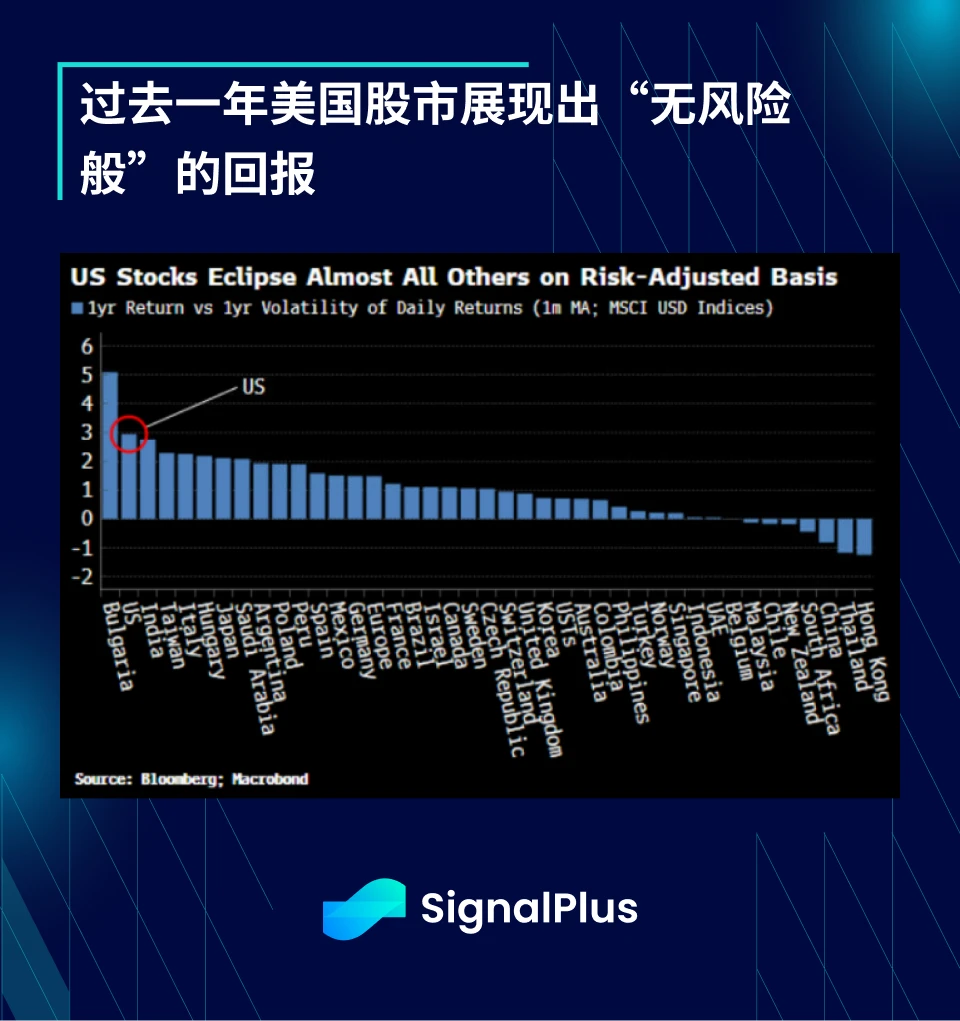

昨天 SPX 指数有 91% 的成分股上涨,所有主要板块均呈现涨势。随著 Nvidia 出现一些乏力迹象,AI 的热潮已开始向硬件股蔓延,费城半导体指数的表现以互联网泡沫以来从未见过的速度超越了 SPX。此外,回顾过去一年,美国股市以近 3 x 的 Sharpe ratio 领先全球股市,考虑到其成分股的巨大市值,这是一个不可思议的成绩,突显了这次牛市行情中所产生的巨大财富效应。

在加密货币方面,纽约开盘时出现了一些价格波动,BTC 价格飙升至近 7.2 万美元,然后反转下跌至 6.85 万美元的低点,同时 Coinbase 股价一开盘也出现波动(几分钟内从 267 --> 278 --> 256 美元),波动可能是由于美国地区法官裁定 SEC 针对 Coinbase 的诉讼可以继续进行,Coinbase 被指控从事未经注册的证券销售,其股价昨天下跌 2.5% ,并给 BTC 价格带来了压力,不过 ETF 净流入仍为正,昨天增加了 4.18 亿美元的资金。

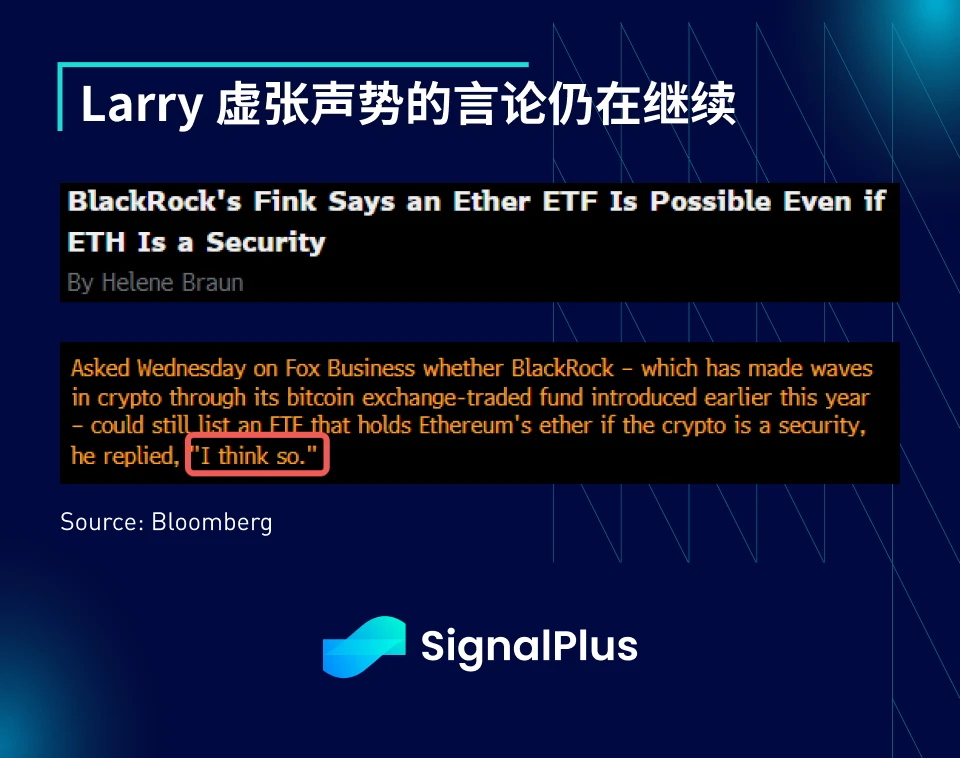

最后,在接受 Fox Business 采访时,Larry Fink 虚张声势的言论仍在持续,他表示即使 SEC 认为 ETH 是一种证券,仍有机会批准 ETH ETF。如果 Blackrock、SEC 和 CFTC 能够一起坐下来好好解决问题,那不是很好吗?

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:xdengalin)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com