Author: David, Deep Tide TechFlow

In 2025, crypto companies raised $3.4 billion in the U.S. stock market.

Circle and Bullish each raised over $1 billion, and Gemini rose 14% on its Nasdaq debut. By January 2026, BitGo rang the opening bell at the New York Stock Exchange, surging 24.6% on the first day, with a market cap of $2.6 billion.

These pioneers proved one thing: Wall Street is willing to pay for compliant crypto infrastructure.

The pipeline for 2026 is even bigger. Kraken, Consensys, and Ledger are all queuing up for IPOs, with valuations ranging from several billion to twenty billion dollars. Even CertiK, a security auditing firm, announced its IPO plans at Davos.

Exchanges, wallets, custody, security... The "water sellers" of the crypto industry are collectively moving toward public markets.

When will these companies go public, what are their valuations, and what are the risks? Let's look at them one by one.

1. Kraken, The $20 Billion Compliance Case Study

Estimated Market Cap: $20 billion

Estimated Time: First Half of 2026

Kraken is one of the oldest crypto exchanges, founded in 2011, a year earlier than Coinbase. But its IPO timing is five years later than Coinbase's. During this gap, it experienced an SEC lawsuit, settlement negotiations, business restructuring, and finally obtained the result of the SEC dropping the case in March 2025.

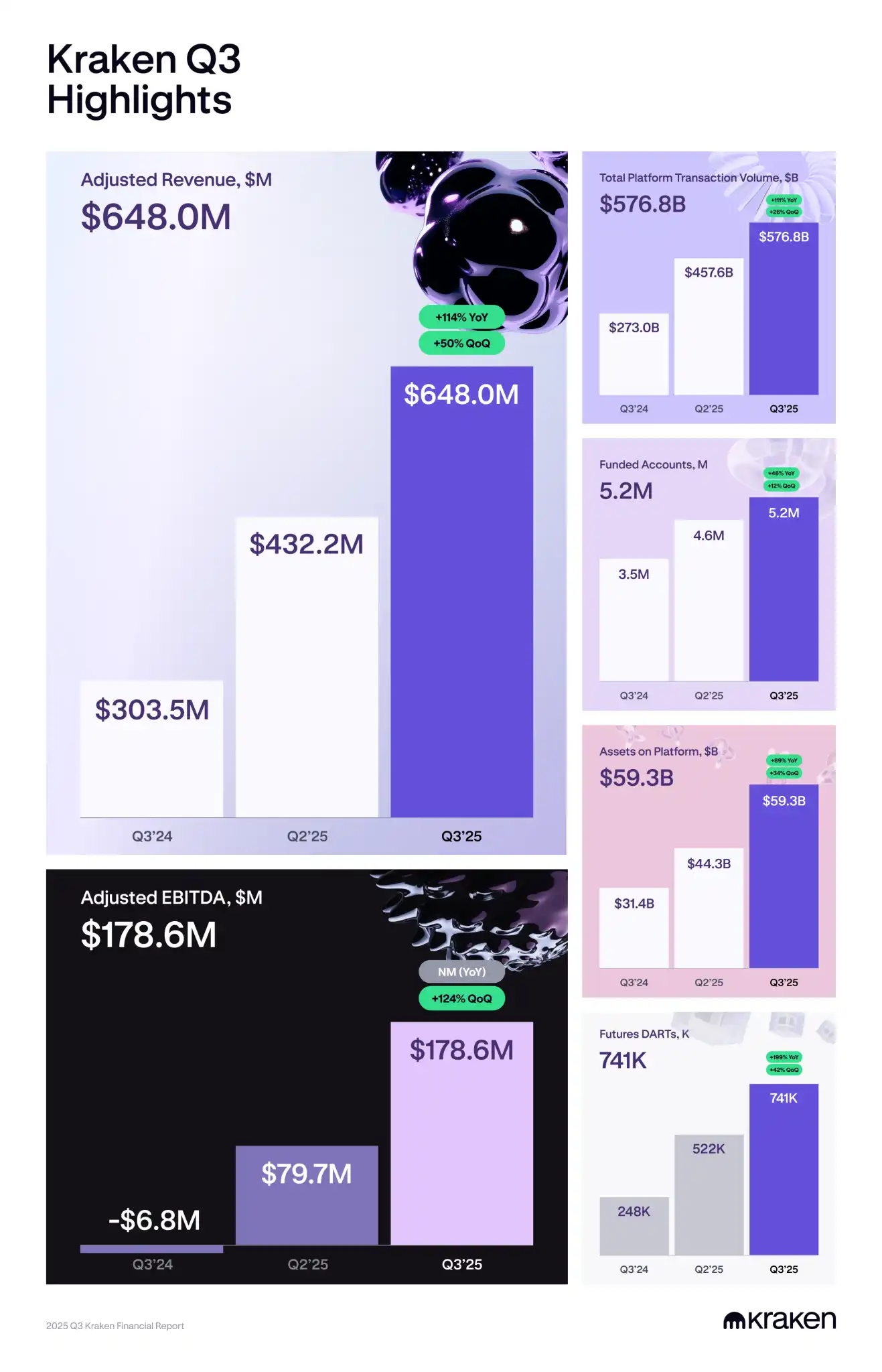

The financial data is also solid:

2024 revenue was $1.5 billion, with adjusted EBITDA exceeding $400 million. In Q3 2025, single-quarter revenue was $648 million, up 50% year-on-year. Platform assets under management were $59.3 billion, with quarterly trading volume of $576.8 billion.

In November 2025, Kraken completed an $800 million pre-IPO financing round, valuing the company at $20 billion. The investor list included Citadel Securities, Jane Street, and DRW. The entry of these top traditional finance market makers means they are betting that crypto exchanges will become part of the financial infrastructure.

In the same month, Kraken confidentially filed an S-1. The goal is to go public in the first half of 2026.

If successful, it will become the second major crypto exchange to list on the U.S. stock market after Coinbase, and the first company to complete the full IPO process in the "post-Gensler era."

2. Consensys, MetaMask's Parent Company Wants to Go Public

Estimated Market Cap: $7 billion (2022 valuation)

Estimated Time: Mid-2026

Consensys owns some of the most valuable products in crypto: the MetaMask wallet with 30 million monthly active users, the Infura node service supporting the底层 of most Ethereum dApps, and the Linea L2 network. It is the "plumber" of the Ethereum ecosystem; almost all developers use its tools.

The company was founded by Ethereum co-founder Joseph Lubin. It raised $450 million in 2022 at a $7 billion valuation. It is now working with J.P. Morgan and Goldman Sachs to prepare for an IPO, targeting mid-2026.

The prospectus is expected to highlight revenue from MetaMask Swaps. This feature allows users to trade tokens directly within the wallet, charging a 0.875% fee per transaction. In 2025, MetaMask also added native Bitcoin support, expanding from a pure EVM wallet to a multi-chain wallet, attempting to keep users within its ecosystem.

The suspense around Consensys' IPO lies in the fact that it is simultaneously working on a MASK token and an IPO. How will these two things be coordinated? Will the interests of token holders and shareholders conflict? This issue may become a new case study in crypto company governance.

3. Ledger, The Hardware Wallet Trying to Tell a Software Story

Estimated Market Cap: $4 billion

Estimated Time: 2026

Ledger has sold over 6 million hardware wallets, custoding over $100 billion in Bitcoin for users. But it doesn't want to just be a "device seller."

In the past two years, CEO Pascal Gauthier has frequently appeared in New York. The story he tells investors is: Ledger wants to become the "Apple of self-custody."

The key to the transformation is Ledger Live, an application that integrates hardware wallets, software wallets, staking, and DeFi interactions. It's shifting from selling hardware to selling subscription services, from one-time revenue to recurring revenue.

Wall Street bought this story.

On January 23, the Financial Times reported that Ledger is in talks with Goldman Sachs, Jefferies, and Barclays for a NYSE IPO, targeting a valuation of over $4 billion. This number is nearly triple its $1.5 billion valuation in 2023.

Supporting this valuation is performance.

2025 revenue reached hundreds of millions of dollars; Gauthier called it a "record year." After the FTX collapse, the phrase "Not your keys, not your coins" became popular again, and both institutions and retail are moving towards self-custody.

Last year, the amount stolen in the crypto industry hit a new high of $17 billion, which ironically became a selling point for Ledger.

However, hardware wallets are still too difficult for the average person to use. Ledger's growth ceiling depends on whether it can lower this barrier.

4. Bithumb, The South Korean Old Guard's Comeback

Estimated Market Cap: Undisclosed

Estimated Time: 2026

Listing Venue: South Korea KOSDAQ (also considered Nasdaq)

Bithumb was once South Korea's largest exchange but was later overtaken by Upbit. Now Upbit holds over 80% of the South Korean market, while Bithumb has only 15% to 20%.

In 2024, Bithumb launched a zero-fee campaign, bringing its market share back to around 25%. This was a battle of burning money to gain users, perhaps to build momentum for the IPO.

Samsung Securities is the underwriter. The original plan was to list on the South Korean KOSDAQ in the second half of 2025, with Nasdaq also considered. Currently, the timeline appears delayed to 2026.

However, Bithumb says this IPO is not for fundraising. The company has over 400 billion won (approximately $3 billion) in financial assets on its books; it's not short on cash. The purpose of the listing is to "build market trust" by having its internal governance and finances subject to public audit.

The background to this statement is: Bithumb has had constant troubles in recent years.

In 2023, it was raided by the South Korean National Tax Service on suspicion of fraudulent trading. Several executives were investigated for alleged listing bribes, and former CEO Lee Sang-jun stepped down. A service outage in 2017 led to a six-year lawsuit, resulting in a ruling to compensate users.

For the IPO, the company made personnel changes. Former Chairman Lee Jung-hoon returned to the board; he was previously acquitted of fraud charges related to an acquisition. The new CEO is his close associate.

South Korea has 18 million crypto users, and daily trading volume often exceeds that of the stock market.

Bithumb's IPO is a signal of the institutionalization of the South Korean crypto market. But given its historical baggage, investors will scrutinize its governance issues.

5. CertiK, The Controversial Security Auditing Leader

Estimated Market Cap: $2 billion

Estimated Time: Late 2026 - Early 2027

On January 23 at the Davos Forum, CertiK CEO Ronghui Gu announced the company is advancing its IPO plans.

This is the largest security auditing company in the crypto industry, founded in 2018, headquartered in New York, serving over 5,000 clients, with audited code protecting assets worth approximately $600 billion.

The investor list is indeed impressive: Binance is the earliest and largest financial backer, with SoftBank Vision Fund, Tiger Global, Sequoia, and Goldman Sachs also involved. Its valuation reached $2 billion during the B3 funding round in 2022.

But CertiK is also one of the most controversial companies in the crypto space.

The Kraken incident last year was a big deal. CertiK found a vulnerability in Kraken that could credit accounts out of thin air and transferred about $3 million during testing. CertiK called it a "white hat operation"; Kraken called it extortion. The two sides had a public spat, the money was eventually returned, but CertiK's reputation was damaged.

Earlier, CertiK also audited Cambodia's Huione Guarantee. This platform was used for money laundering, buying and selling hacking tools and personal data, and even selling stun guns to scam compounds in Southeast Asia. CertiK later apologized, but this incident showed that the security company's own risk control also has problems.

Gu Ronghui said the IPO is the "natural next step for the continued expansion of products and technology."

But once the IPO prospectus is public, these controversies will be repeatedly questioned by investors. Whether CertiK can rebuild trust is the biggest test on its path to going public.

Overall, the cluster of crypto company IPOs in 2026 might not be a coincidence.

The regulatory environment is changing. SEC Chairman Gensler is gone; the new chairman is more friendly towards crypto; lawsuits against Kraken and Consensys were dropped. The window is open, and those who should are rushing.

The capital structure has also reached its limit. These companies have raised many rounds in the private market, with more and more shareholders, and employee options becoming harder to cash out. Coinbase has been public for five years, proving that crypto companies can survive in the public market. Those waiting in line have no reason to wait any longer.

However, for ordinary investors, this batch of IPOs needs to be differentiated.

Kraken and Ledger have real revenue and clear business models; Consensys has the gateway product MetaMask, but is simultaneously working on a token, and the relationship between shareholders and token holders is not yet sorted out. CertiK has brand recognition but controversy, and Bithumb is a purely South Korean domestic story.

When you can buy, first figure out what you are buying.

For the companies, going public is just the beginning.

Whether they can stand firm in the public market depends on whether these companies can replace the "crypto" label with "financial infrastructure." Coinbase took five years to convince Wall Street it was more than just a crypto trading platform.

For those following, the road is still long.