原创 | Odaily星球日报

作者 | Asher

Blast 主网上线:更新积分规则,迁移主网成本高

火爆的链上数据

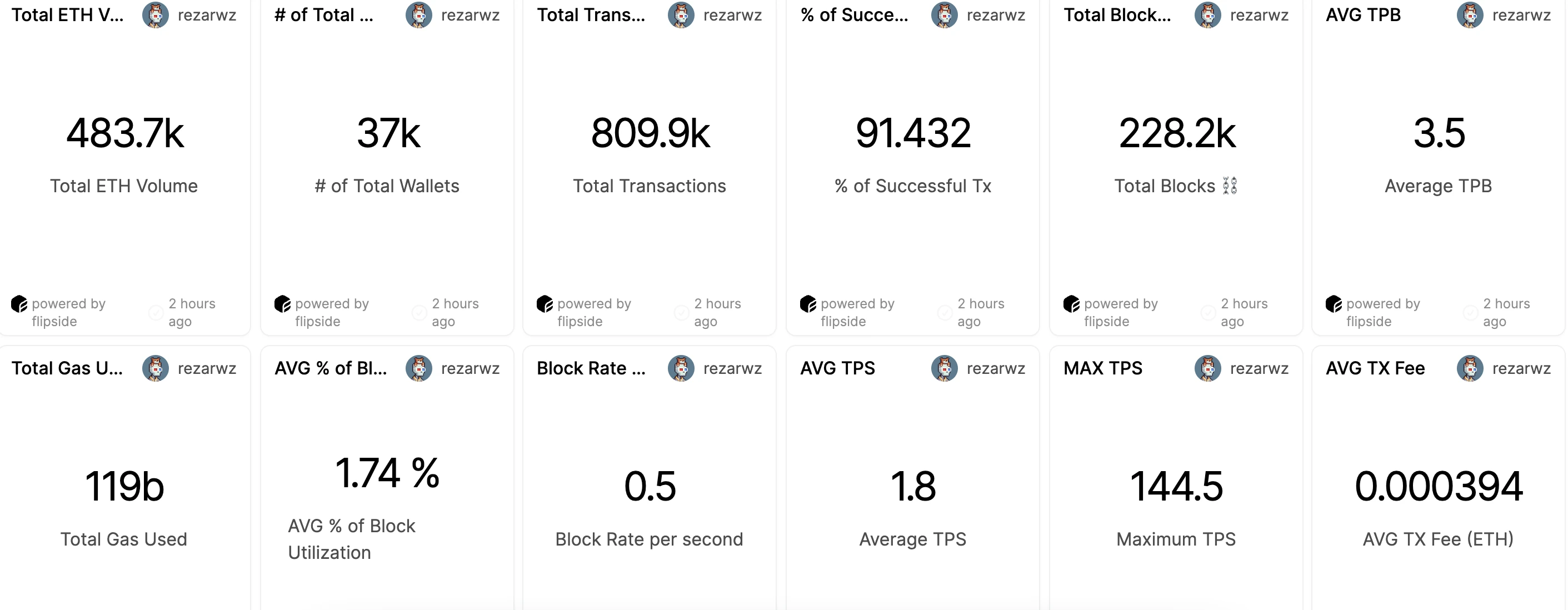

3 月 1 日,基于 Optimistic Rollup 的 Layer2 网络 Blast 正式上线主网,一时间链上活动活跃。根据 Flipside 平台的数据面板,截止到目前,Blast 网络中共有 3.7 万个钱包执行近 81 万笔交易,平均每秒创建 0.5 个区块,平均 Gas 费为 0.000394 ETH(按当前价格计算约为 1.33 美元),平均 TPS 为 1.8,峰值 TPS 为 144.5。

公布新积分规则

参与 Blast 测试网的用户最为关心的是继续参与主网交互的奖励部分。目前 Blast 允许早期访问用户跨链到主网并使用 Blast 原生 DApp。

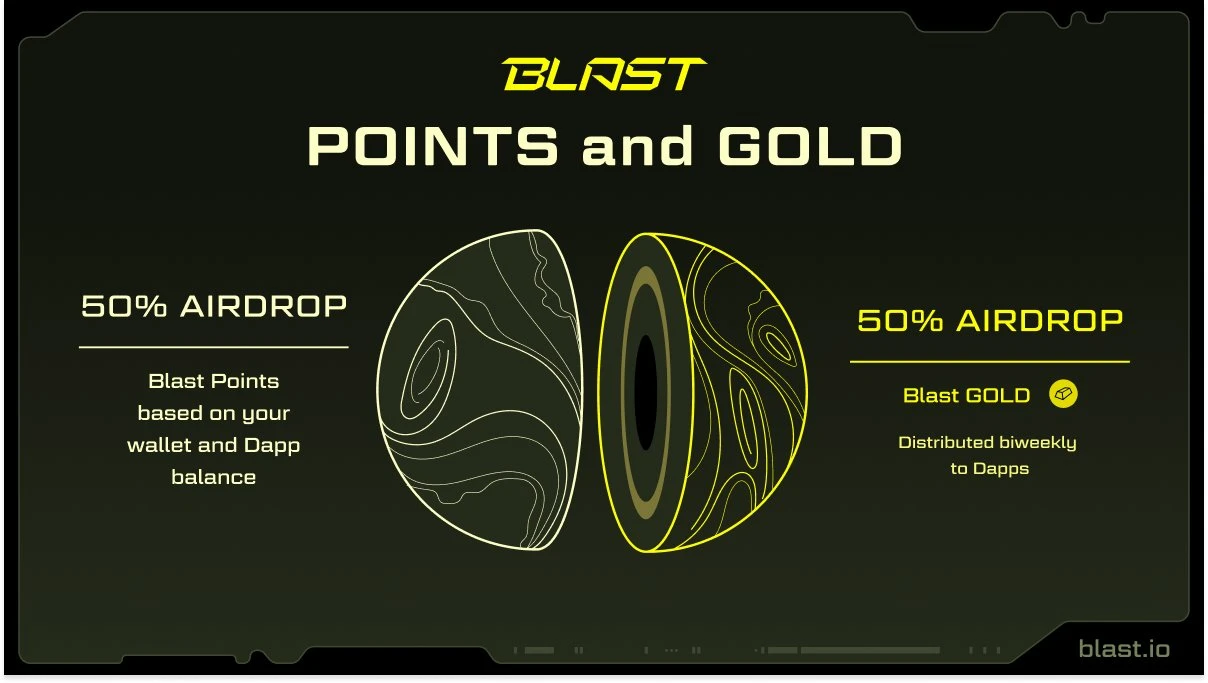

具体规则为:主网用户将继续赚取 Blast 积分,主网 DApp 现能够赚取 BlastGold(Blast 金币)。Blast 空投的 50% 分配给 Blast 积分(用户), 50% 分配给 Blast 金币(DApp)。金币将每两周分发给 DApp。Dapp 可以为自己保留金币,但部分 DApp 已经承诺将所有金币给用户。

Odaily星球日报在此提示,Blast 生态项目鱼龙混杂,决定参与前请 DYOR,谨防风险。

图源:官推

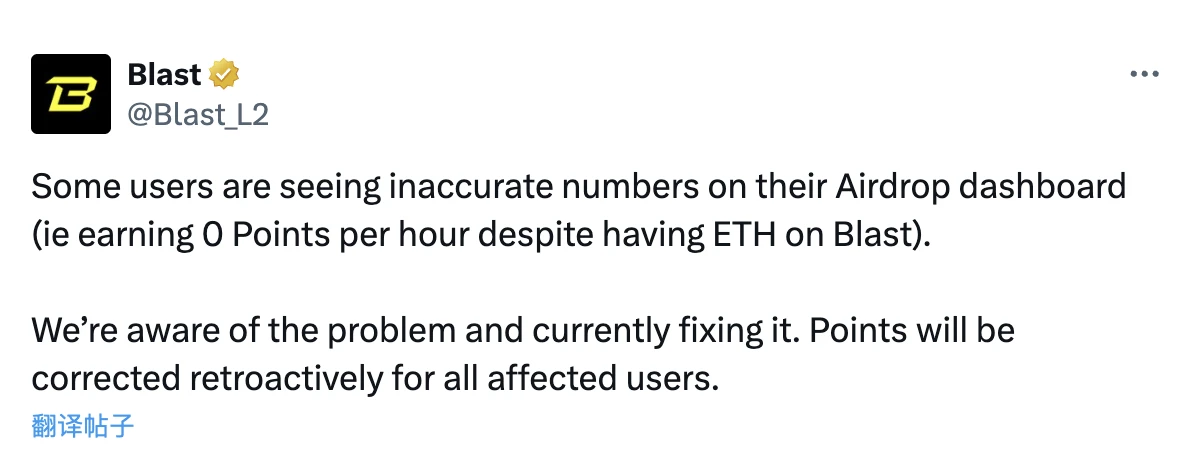

根据社区多名成员反馈,从测试网映射到 Blast 主网的积分出现严重 BUG,有些地址的积分显示并没有按照官方说的 10 倍积分,而是一个 0-10 倍的随机数,甚至有用户拿到了 0 积分。对此,官方在官推中第一时间出了公告:承认积分的计算出现问题,目前正在修复中,所有受影响用户的积分将被追溯纠正。

图源:官推

昂贵的迁移成本

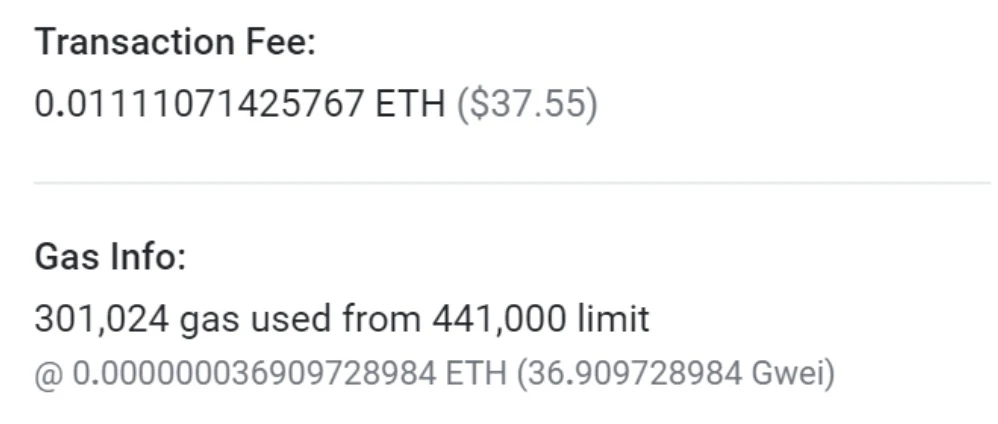

由于新的积分规则中有说明,迁移到 Blast 主网之后,每个小时都会增加积分,并且默认增加速度为 1 倍,最高增加速度为 12 倍,因此很多用户准备将 ETH 第一时间迁移到 Blast 主网,但本次手动迁移的 Gas 成本基本在 35-80 美元之间,一时间很多散户与多号用户怨声载道,抱怨迁移成本过高。图为社区用户在 Gwei 为 37 时的迁移的数据记录,成本为 37.55 美元。

迁移成本

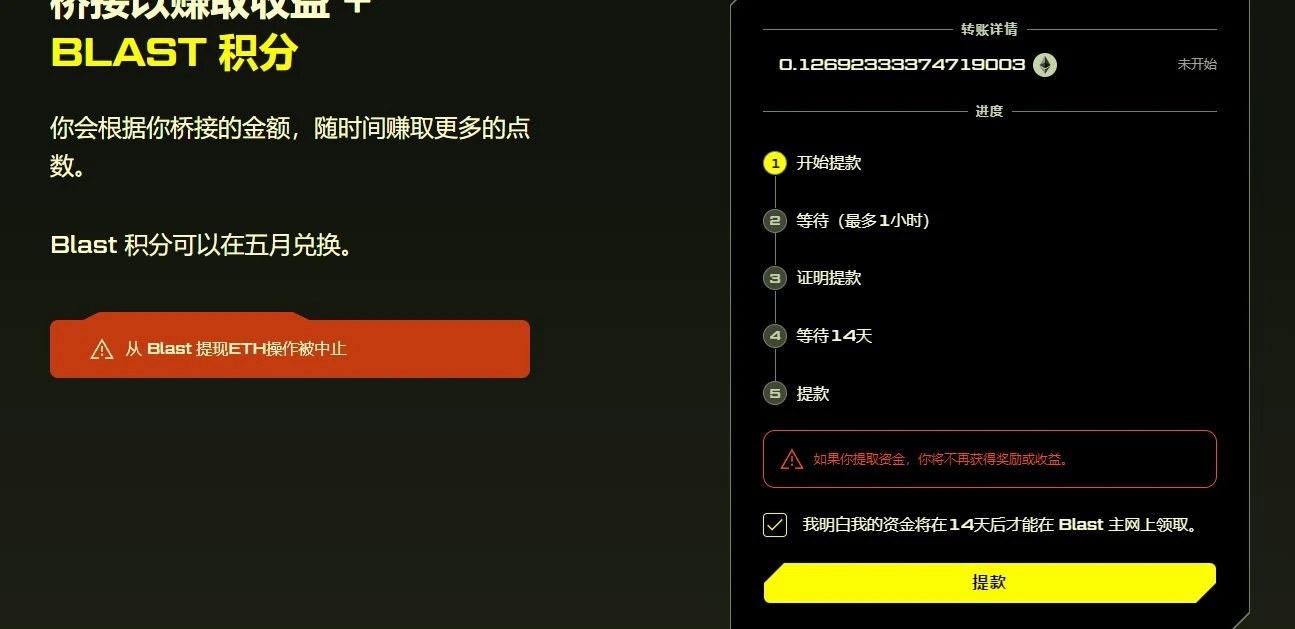

同时,有社区反馈,即便不想参与 Blast 主网的交互,也需要将 ETH 迁移到 Blast 主网之后才能提现到以太坊一层。目前,通过官方桥进行提现需要 14 天的等待时间,如下图。Odaily星球日报提醒用户,目前其他第三方跨链桥提现存在不确定性的风险,注意资金安全。

14 天等待期

热度很高,但质疑声不断

虽然 Blast 主网上线的几小时有着超高的链上热度、社区热度,但社交媒体上弥漫 KOL 和普通参与者的怨气:

“Blast 最傻 X 的地方是当时存进去 ETH 的 Gas 就不便宜,现在上了主网还要花钱跨。”

“Blast 跨到主网,Gas 比存进去的时候还高,请问是我的操作问题?”

“主网上线完全可以按照之前跨链映射,为什么要让全网 20 多万的用户再烧一次手续费呢?不是所有人都是巨鲸,不在乎这点手续费的。难道 Blast 不需要散户吗?”

“Blast 上还没有项目方官方支持的项目,全是土狗盘子群友创业,参与的还都是 ETH 链上的‘大割’,都是链上经验丰富,散户跑不快就等着被埋。”

“Blast 链就跟当年 BSC 链一样,一堆跑路项目,据说这段时间,铁顺天天跟中国项目方开会。”

“Blast 感觉‘含国量’太高了,上面的项目纯 PVP 博弈,晚跑一秒就不用跑了。”

……

综述

回顾 Blast 主网上线这半天,无论是大量新开盘的链上土狗项目迅速跑路,还是公布的新积分计划,再到主网迁移昂贵的 Gas 费,整个过程中用户的怨气不断积累。

若 Blast 主网上线后不能培育出一批优质项目,或从官方角度为用户谋些福利(不说增加积分系数,哪怕省点 gas),那么 Blast 的热度会逐渐被不良的体验浇灭。

毕竟,决定坚守在此的参与者还都瞄着下个重要时间节点(5 月)。在此之前,是继续通过积分 PUA 用户还是会短期来一次“空投盛宴”,Blast 可以多做考虑。