本文来源:Pantera Capital

译者:Odaily 星球日报 Azuma

编者按:昨夜至今晨,加密市场再次迎来行情突变,BTC 一度突破 57000 美元,单日大涨 10% 。值此关键时刻,许多投资者都在努力寻找各类利多信号,试图为 BTC 的突然上涨寻找答案,但 Odaily星球日报却发现 Pantera Capital 在近期发布的一篇报告《The Absence of Bad Things》中提供了一种很别致的思路 —— 当前市场最大的特点在于找不到任何利空事件,这本身就是最大的利好。

以下为 Pantera Capital 报告总述部分内容,由 Odaily 星球日报编译。

去年六月,我在彭博投资大会(Bloomberg Invest Conference)与美国证券交易委员会(SEC)前主席 Jay Clayton 一起就银行危机、宏观市场以及区块链进行了讨论。

在讨论结束之际,主持人问了我一个问题:“我们应该留意哪些潜在的黑天鹅事件?”

我当时的回答是:“在黑天鹅发生之前,每个人都会选择忽视,一旦发生了,大家又会想着讨论‘下一个(黑天鹅)会是什么’。在我看来,目前最好的消息就是我们在过去一年间已见证了所有潜在黑天鹅的落地,不会再有什么更疯狂的事情发生了……如果你非要让我说些什么,我只能说监管态度是没人预料到的,这可能导致好几种不同的结果。”

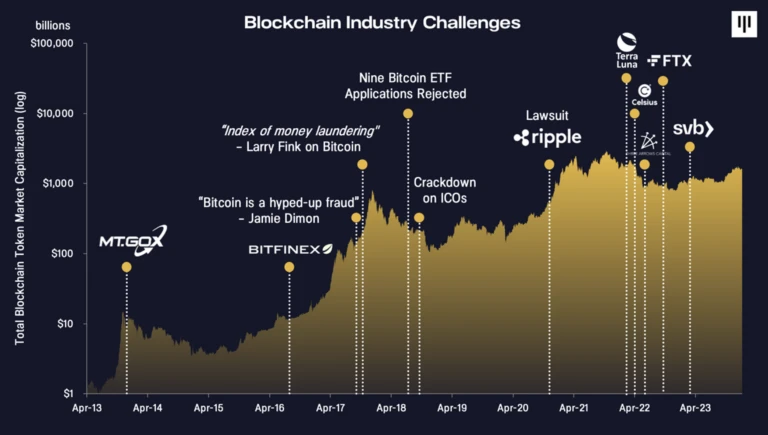

关于当前的市场状况,一个非常重要的主题就是坏消息的缺席。

在 2022 年和 2023 年的大部分时间里,各种罕见到疯狂的坏消息不停地在出现。

全球宏观市场经历了史无前例的波动。专门从事历史投资回报相关研究的圣塔克拉拉大学名誉教授 Edward McQuarrie 曾表示, 2022 年是美国债券投资者经历过的最差年份 —— “即使你回溯 250 年,也找不到比 2022 年更糟糕的一年。”

2022 年也是“经典 60/40 股债组合”自大萧条以来表现最糟糕的一年。

私募市场所遭受的影响更大,这直接影响了我们的风投业务。与上一年相比,IPO 募资总额减少了 95% ,交易量则减少了 85% 。

加密货币市场同样无法幸免,FTX 的暴雷以及六家借贷机构荒谬的杠杆操作导致加密货币总市值缩水了逾 70% 。

在我看来,这些本都应该是一代人才会遇见一次的疯狂事件。在接下来的 10 年或 15 年里,不会再有人给加密货币对冲基金借款,尤其是那些没有抵押物、业务不透明的机构,但凭借我超过 25 年的周期性观察经验,再往下一代肯定会有人再次这么做。

下面是区块链历史上灾难性事件的直观视觉展现。

这些黑天鹅并没有杀死加密货币,而它们的缺席,反过来则成为新一轮周期的巨大利好。

还有另一项巨大的利好,加密货币行业之前面临的一些监管障碍已经消除,特别是对于那些希望基于该新兴资产类别进行构建的金融机构而言。

过去一年间,Ripple、Grayscale 的胜诉以及 ETF 的获批都预示着区块链领域的监管环境可能正在趋于明朗。

自一月份比特币现货 ETF 获批上线之后,机构端的采用速度看起来似乎已在加速。

鉴于比特币还将在 2024 年 4 月底迎来减半,我们相信这些利好的相互作用将推动 BTC 走向下一轮牛市。

此外,区块链行业可能正在经历从“拨号上网”向“宽带”时代的跃迁。我们可以通过以太坊 Layer 2 和其他高性能 Layer 1 的增长上见证这一跃迁,这将是我们三月投资者沟通的主要内容,且将成为我们下一次主题研讨会的焦点。

Pantera Capital 聚焦于加密货币行业的时间可能比任何公司都长 —— 超过十年,见证了多次牛熊轮回。我们已经经历了三个完整的周期,见证了多次暴涨与暴跌。我们认为,市场现在正处在第四个大周期的开端。

2022 年的股市崩盘对机构投资者造成了巨大的冲击,许多机构已撤出私募市场。现在,随着股市重回历史高点,它们将会再次杀回私募市场,因此我认为,在接下来的 18 到 24 个月,加密货币市场很可能会迎来一波强劲的牛市。

当前正是一个转折性时刻,过去几年金融市场和区块链领域的创伤已经成为过去,同时减半和监管趋缓等积极因素也都在同时发生,这一切都预示了未来的发展方向。