自上周英伟达超预期的财报公布后,科技板块经历了惊人的涨幅,尽管周五因部分获利了结而稍显落后,但美股仍保持在历史高点附近。另一方画面,卖方经济学家一直在上修美国经济增长预测,普遍认为经济衰退的可能性已经降至 40% 不到, 2024 年经济增长预测的中位数为 2.1% ,高盛也因强劲的经济数据而将美联储首次降息的预测推迟至 6 月,当前互换市场对 5 , 6 月降息的概率分别定价在 22% 和 68% 左右。美债方面,十年期美债于周五美盘时段大幅跳水,现报 4.242% ,两年期回落至 4.682% 。

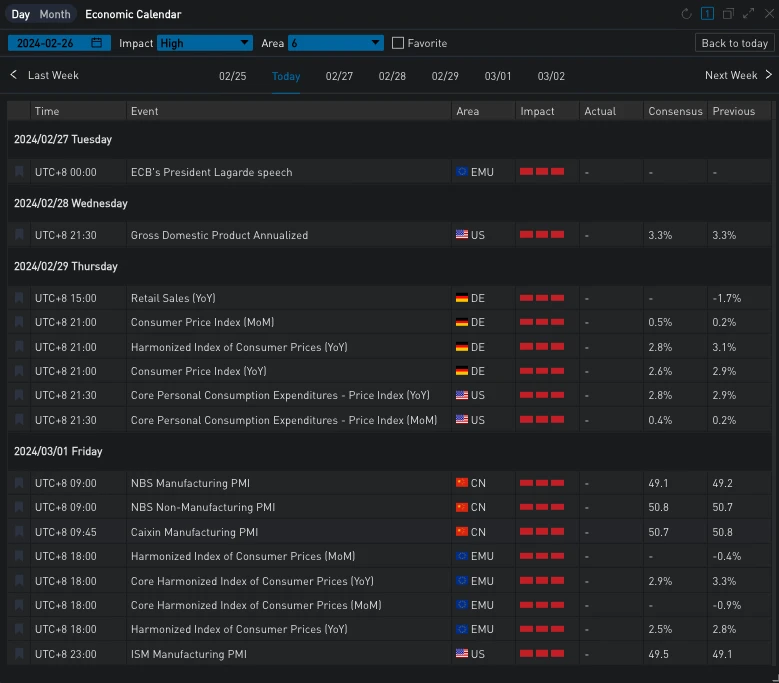

Source: SignalPlus, Economic Calendar

Source: Binance & TradingView

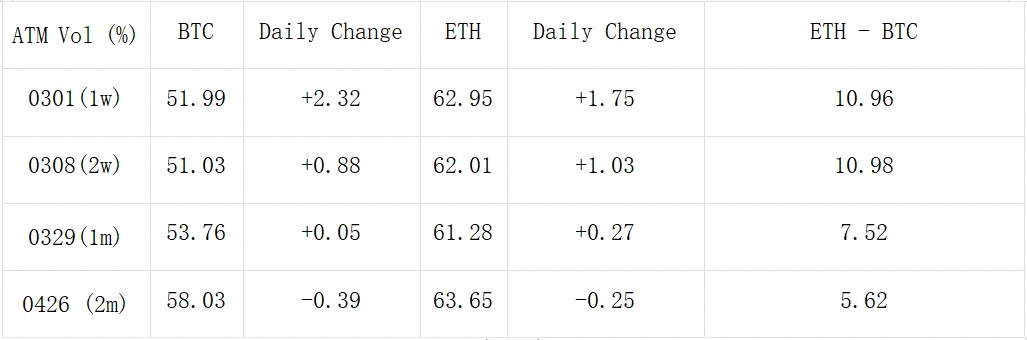

数字货币方面,BTC 已经在 51000-52000 美元附近横盘接近 12 天,ETH 则是实现了进一步的突破来到 3000 点上方,收报 3092 (+ 2% )。期权方面,ETH 隐含波动率仍然居于 60% 附近的高点,BTC 大多则是在 50% 附近,中前端 IV 差距高达 10% Vol。

Source: Deribit (截至 26 FEB 16: 00 UTC+ 8)

Source: SignalPlus

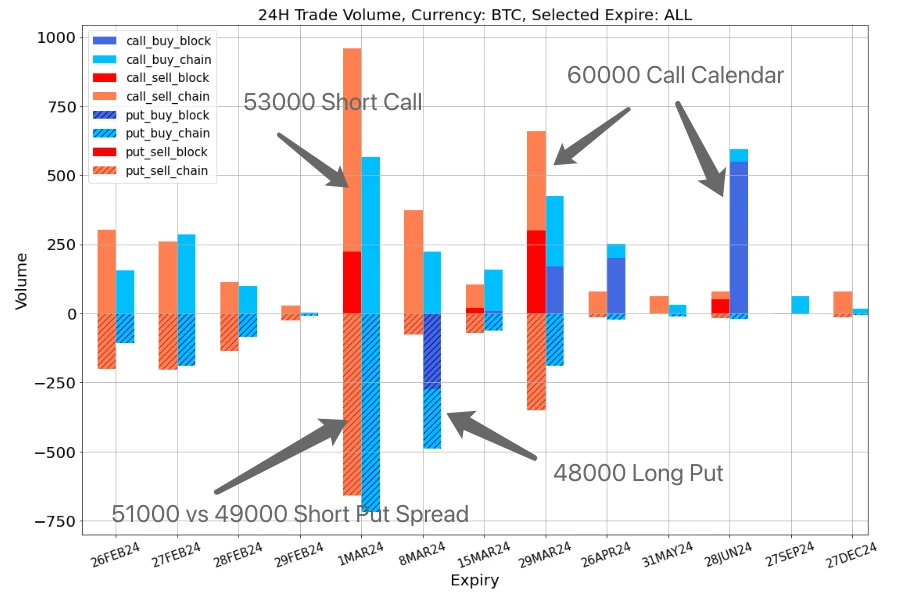

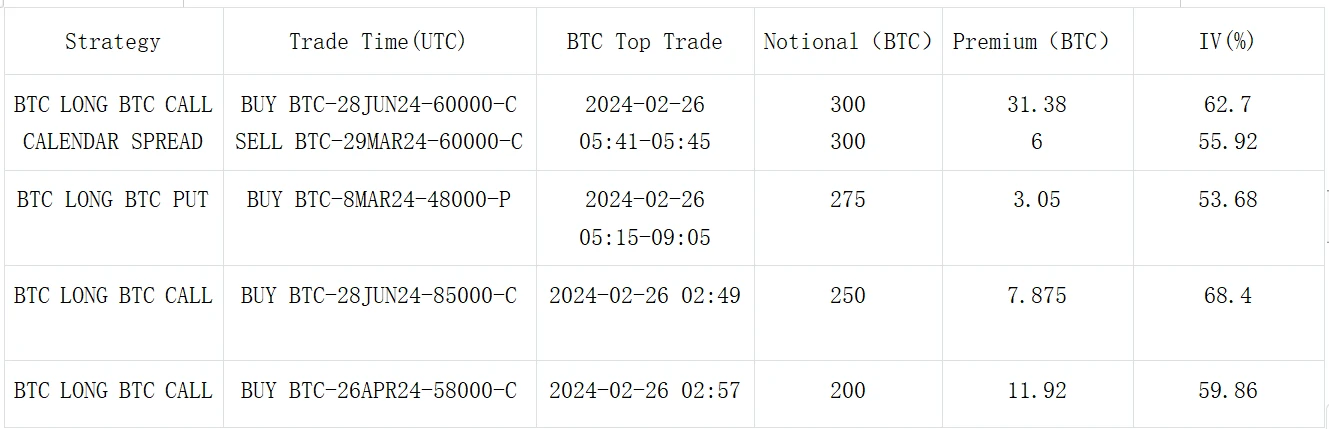

交易方面,BTC 六月底突然涌现看涨期权买入,主要来自大宗 85000 买 Call,以及一组 Buy 28 Jun Sell 29 Mar 60000-C 的日历价差;除此之外,尽管是上周买 Vol 的热门期限,过去 24 小时 1 MAR 的成交主要却以 Short Put Spread 和 Short Call 为主。

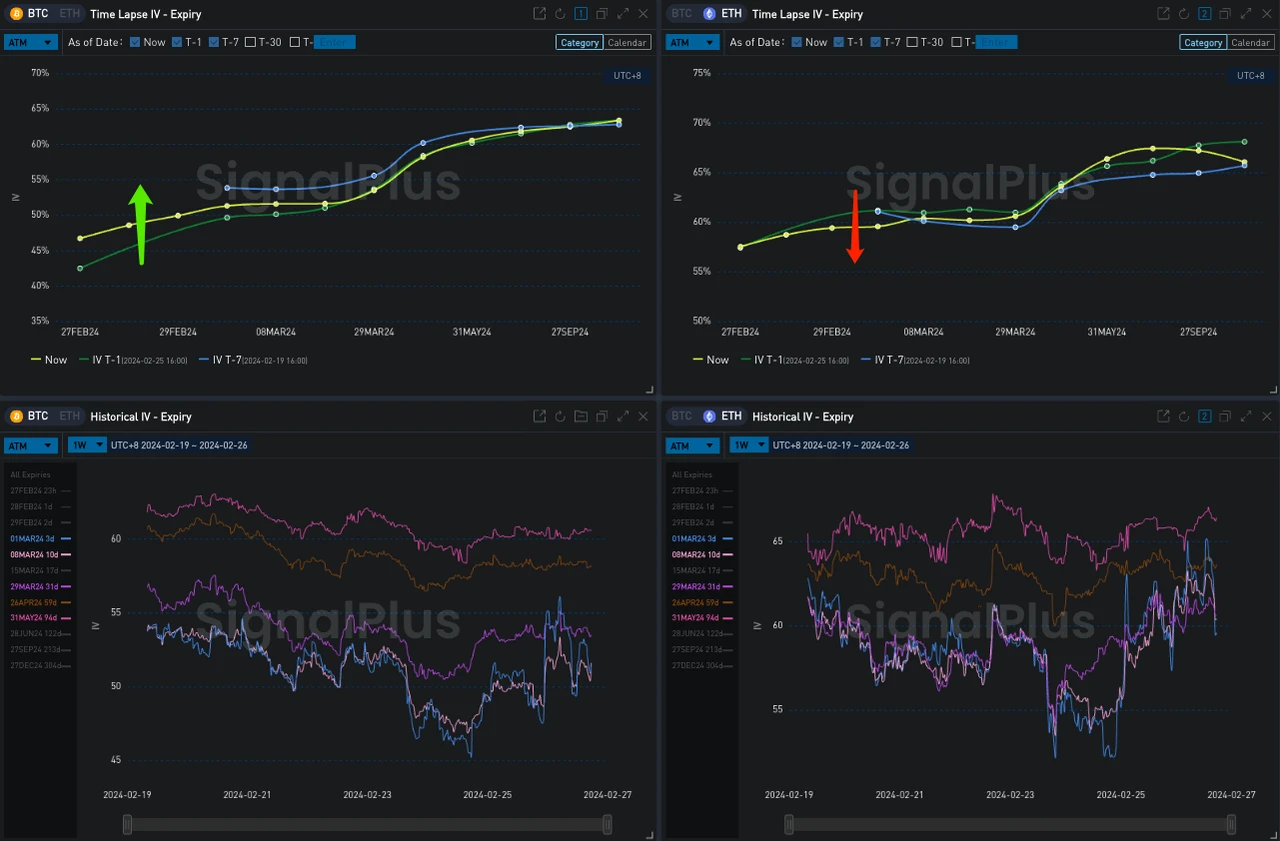

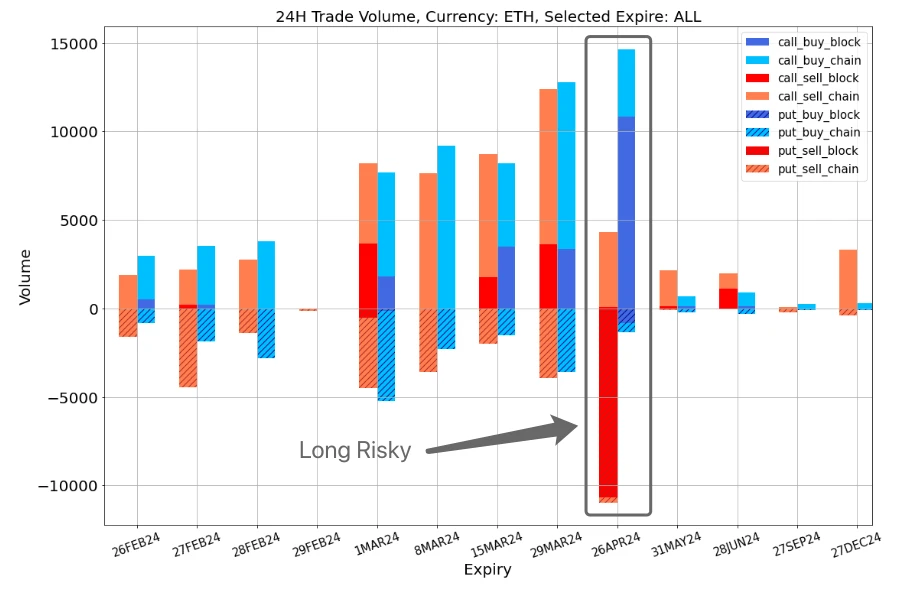

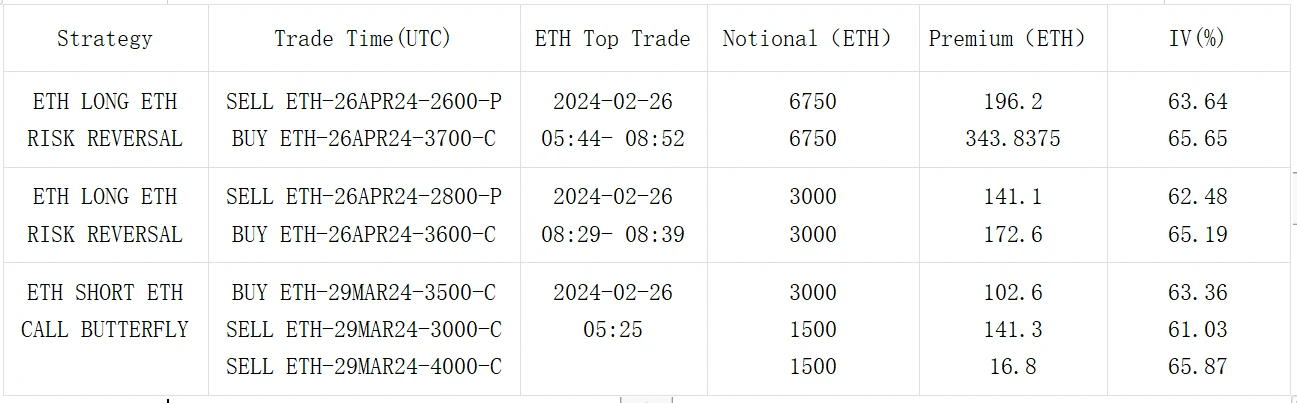

另一方面,观察到过去 24 小时 BTC/ETH 前端的 Vol Skew 明显下滑,三月往后的期限上扬,从交易上看,ETH 四月底出现了以 2600 vs 3700/ 2800 vs 3600 为代表的两组 Long Risky,总成交量逾 10000 组。

Data Source: Deribit,BTC 成交分布

Source: SignalPlus,前端 Vol Skew 下行

Data Source: Deribit,ETH 成交分布

Source: Deribit Block Trade

Source: Deribit Block Trade

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com