下周, 13 个项目迎来代币解锁事件。DYDX、YGG、PRIME 将有大额解锁,DYDX 解锁量占当前流通市值的 11.1% 。

具体解锁详情如下:

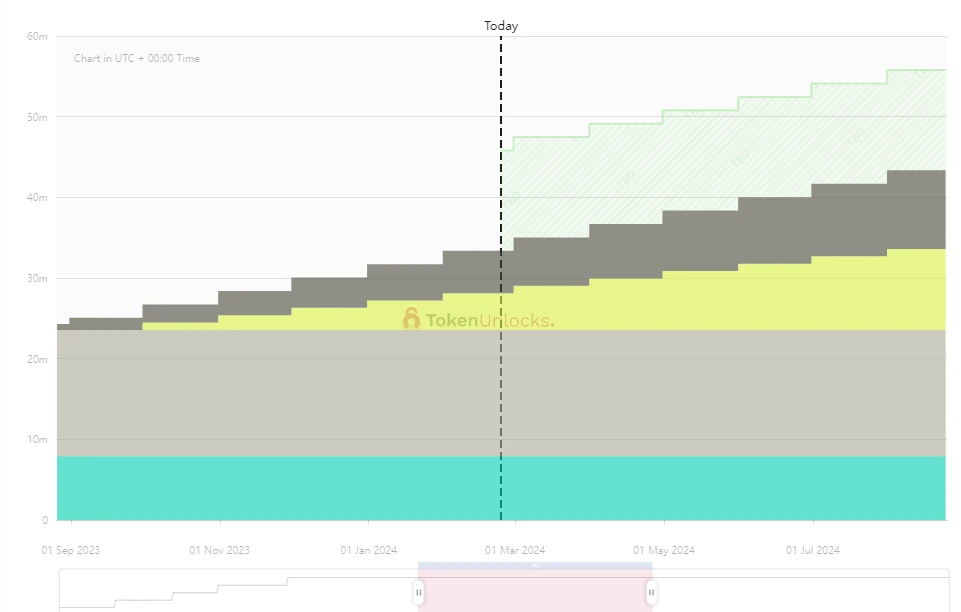

dYdX

项目推特:https://twitter.com/dydxfoundation

项目官网:https://dydx.trade/

本次解锁数量: 3350 万枚

本次解锁金额:约 1.29 亿美元

dYdX 是用于永续合约和保证金交易的去中心化衍生品交易所,提供订单簿式的区块链数字资产交易服务,并提供杠杆和合约的交易功能。dYdX 采用链下撮合 + 链上结算的订单模式。操作体验更接近于传统的 CEX,可以实现限价交易、止损等操作。

DYDX 本轮解锁的主要对象包括投资者和团队。其中投资者份额为 1849 万枚,价值 5435 万美元。其余面向团队的份额约 4370 万美元,将向创始人、员工和顾问分发价值 3000 万美元的 DYDX,并留存 1370 万美元的代币用于将来的员工雇佣。

值得注意的是,近期 dYdX 因 Uniswap 将向 UNI 分配手续费的热点而大幅上涨,存在获利出售的可能性。

具体释放曲线如下:

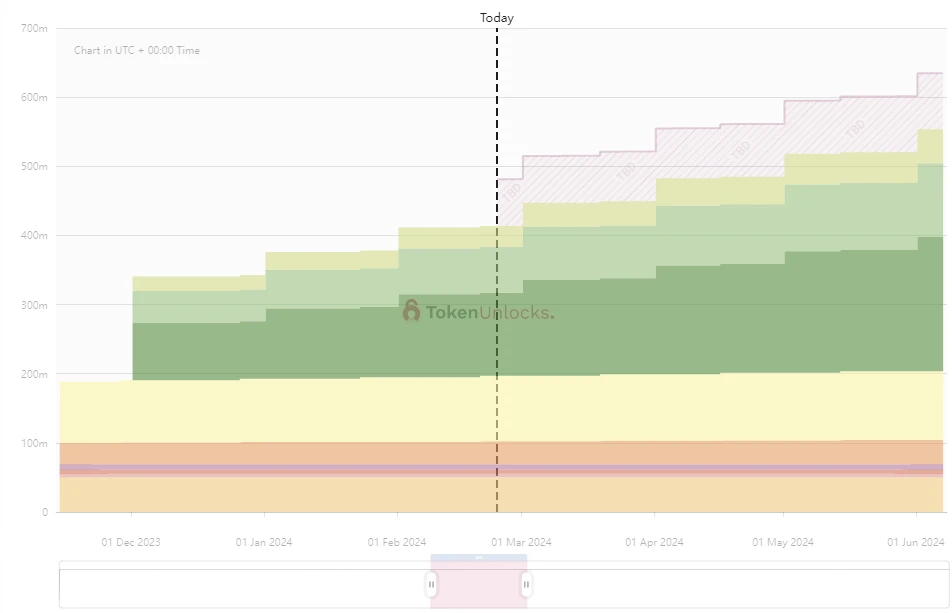

YGG

项目推特:https://twitter.com/YieldGuild

本次解锁数量: 1667 万枚

本次解锁金额:约 887 万美元

Yield Guild Games (YGG)是一个去中心化的自治组织 (DAO),用于投资基于虚拟世界和区块链游戏的 NFT。

YGG 本轮释放的各对象配额较为均衡,最高者为社区的 701 万枚,最低者为财库的 231 万枚。当前 YGG 总量已解锁了 57% ,并且进入较为均衡的释放阶段,虽释放占比达 5.6% 但项目市值较小,预计影响不大。

具体释放曲线如下:

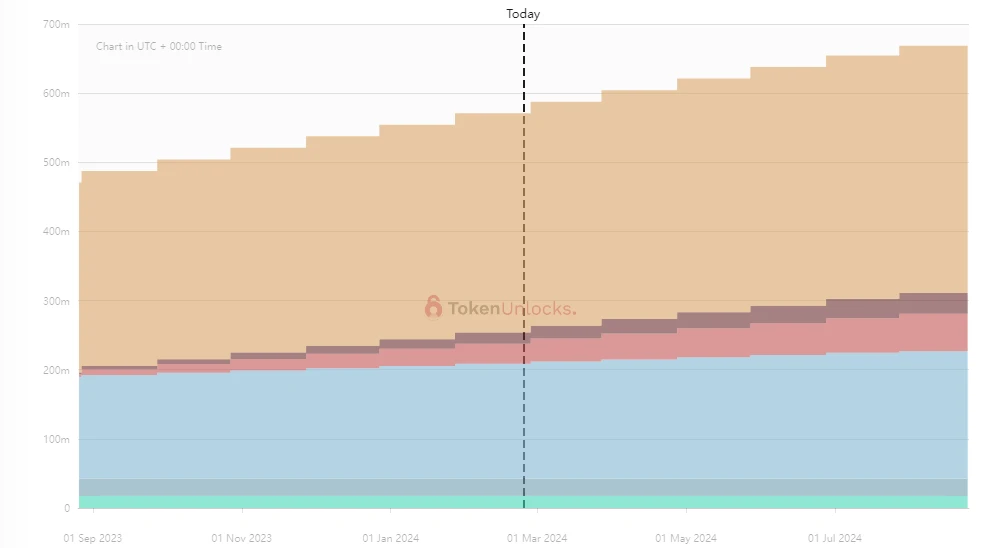

Prime

项目推特:https://twitter.com/EchelonFND

项目官网:https://echelon.io/

本次解锁数量: 167 万枚

本次解锁金额:约 1567 万美元

Echelon Prime 是一个链游平台,目前已宣发推出两款游戏,分别为卡牌游戏 Parallel TCG,以及模拟类游戏 Parallel Colony。PRIME 是 Echelon 及其游戏生态系统的实用代币,用于购买各类产品、服务和游戏体验。

本轮代币解锁主要面向两类对象,分别为 Parallel 工作室的储备资金和投资者,前者将分发价值 1128 万美元的代币,后者分发 928 万美元的代币。此外据 token.unlocks 图表显示,还有价值 1.52 亿美元的基金会份额待解锁,具体规则尚未宣布。

具体释放曲线如下: