原创 | Odaily星球日报

作者 | Azuma

随着比特币现货 ETF 的审批关口临近,加密市场情绪继续升温。

昨晚至今晨,市场再次迎来大幅上涨。欧易 OKX 行情显示,BTC 短时突破 45000 USDT,最高一度触及 45406.7 USDT, 24 小时涨幅 5.66% ;ETH 则一路逼近 2400 USDT,最高一度触及 2397.76 USDT, 24 小时涨幅 2.7% 。

除 BTC、ETH 外,部分近期势头强劲的 Alt-coin 也延续了亮眼的表现,截至发文,SOL 暂报 111.57 USDT, 24 小时涨幅 7.4% ;ARB 暂报 1.74 USDT, 24 小时涨幅 9.8% ;TIA 暂报 13.85 USDT, 24 小时涨幅 14.8% ;SEI 暂报 0.7879 USDT, 24 小时涨幅 35.19% 。

受整体行情上行影响,加密货币总市值也迅猛增长。CoinGecko 数据显示,目前加密总市值突破 1.81 万亿美元, 24 小时上涨 4.8% 。加密用户交易热情亦明显上升,今日恐慌与贪婪指数已达 71 ,等级为“贪婪”。

衍生品交易方面,Coinglass 数据显示,过去 12 小时全网爆仓 1.11 亿美元,其中绝大部分为空单爆仓,数额达 9292.59 万美元。从币种来看,其中 BTC 爆仓 5705 万美元,ETH 爆仓 1440 万美元。

ETF 审批关口临近

环顾消息面,当下对于市场走势影响最为显著的莫过于比特币现货 ETF 的审批动态。

截至上周五,包括贝莱德、VanEck、Valkyrie、Bitwise、Fidelity、WisdomTree、Ark、 21 Shares 在内的多家 ETF 发行申请方均已向监管机构提交了最新的申请文件,完善说明了关于授权参与商(Authorized Participant,即承销商)的细节安排,以确保 ETF 上线之后的交易流动性。

根据申请规定,美国证券交易委员会(SEC)对于上述多支 ETF 申请的最终审批截止日为 1 月 10 日,这也意味着 SEC 必须在 1 月 10 日之前就“批准”或“拒绝”作出抉择。

此前,多位 ETF 专家均曾预测过 SEC 做出最终审批的时间窗口。The ETF Store 总裁 Nate Geraci 认为 SEC 最早可能在 1 月 2 日(今天!)便做出决定;彭博分析师 James Seyffart 则认为 SEC 可能在 1 月 5 日到 1 月 10 日期间发布公告;Swan Bitcoin 首席执行官 Cory Klippsten 预测的时间窗口则是 1 月 8 日至 1 月 10 日。

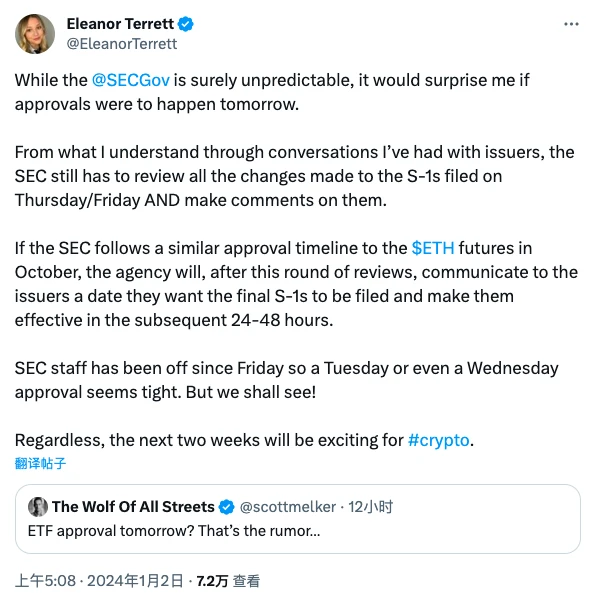

不过,根据今日早间 FOX 记者 Eleanor Terrett 的最新报道,由于 SEC 仍需时间来审查上周四、周五各大 ETF 申请方所提交的关于授权参与商的更新文件,且需要对此发表评论,同时考虑到自上周五以来 SEC 一直在休新年假期,因此不太可能在本周初(周二、周三)返工之后立即作出关于 ETF 的决定。

Odaily 星球日报注:有消息称“贝莱德透露 SEC 可能会在周末做出决定”,该消息实为误报,另一位 FOX 记者 Charles Gasparino 确认贝莱德已被 SEC 下发了静默令,不会就此事发表评论。

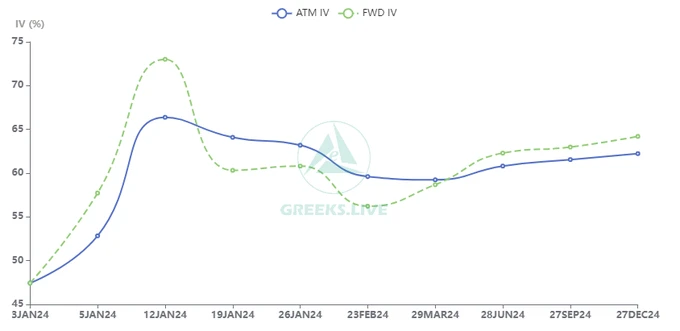

从期权市场的结构来看,市场似乎也更加倾向于 Eleanor 的说法,Greeks.live 宏观研究员 Adam 在 X 平台发文表示:“尽管市场有传言本周 BTC 现货 ETF 可能通过,但是期权市场数据显示 IV 最高的仍然是 1 月 12 日到期的期权。目前 1 月 12 日到期的平值期权 IV 接近 70% ,明显高于假期前,且显著高于中远期 IV 60% 的平均水平,机构投资者仍认为第二周(即更接近 1 月 10 日)会是 ETF 消息落地的时间点。”

yes or no?仍是未知数

尽管从当下的投资情绪来看,市场似乎对于比特币现货 ETF 的获批普遍抱以积极态度,但正如 Eleanor 所强调的:“SEC 是不可预测的。”

在 SEC 做出最终决策之前,没有人知道审批的结果是 yes 还是 no。

上周,SEC 互联网执法办公室前主任 John Reed Stark 结合其个人在 SEC 长达 20 年的工作经验就此事的结果进行了评论。John 表示,尽管其个人持反对态度,但如果过去一段时间关于 SEC 和所有 ETF 申请方之间会面讨论的报道都是真实的,那么根据其个人经验,SEC 批准现货比特币 ETF 似乎是可能的。

但与此同时,市面之上也有一些声音认为 SEC 暂时仍不会打开绿灯,比如 LD Capital 联合创始人 Joy Lou 就表示:“我认为不会过,BTC 价格也不会有很大波动。”

最终的结果究竟如何?八天之内,分晓立见。