原创 | Odaily星球日报

作者 | 0xAyA

终于,BendDAO 也开始发铭文了——这个此前专注于 NFTFi 领域,致力于为蓝筹提供更多流动性的协议,最终也还是逃不过 BTC 生态和铭文滚滚而来的浪潮。早在两周前,BendDAO 就表示,团队计划提出解决方案来拥抱比特币 NFT 生态系统,新的解决方案将允许比特币 NFT 和 BendDAO 之间的无缝交互,并支持 WBTC 流动性池作为可借贷资产。

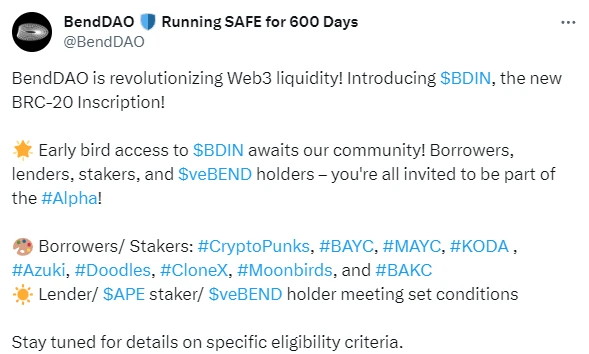

而后 BendDAO 宣布将连接 BRC 20 和 ERC 20 流动性,并即将推出 BendDAO BRC-20 ,为比特币生态提供借贷和跨链桥服务。就在昨天,官方正式宣布将推出 BRC-20 代币 BDIN,将向借款人、贷款人、质押者和 veBEND 持有者提供优先权益。

BRC 20 是在比特币网络上发行同质化代币的格式标准,它是通过利用 Ordinal 协议将铭文设置为 JSON 数据格式来配置代币合约、铸造和转移代币,我们可以将其理解为是一种变异的序数 NFT,NFT 上铭文刻录的是图片,BRC 20 上标识的铭文都是统一的 JSON 格式的文本数据(文本)。在 BRC 20 中,铭文亦是 BRC 20 代币的记账账本,可用于追踪每一次代币的变动。ERC 20 则是基于 EVM 依赖智能合约的代币,而由于 BTC 缺乏智能合约支持,所以在 BRC 20 上面发行的代币功能较少。

虽然两者同为代币标准,但 ERC 20 与 BRC 20 本质上来说较少有相通之处。BendDAO 提供跨链桥服务,毫无疑问将大大减少两者之间的隔阂,而这种跨链支持也能够提升两个最重要的生态系统之间的流动性,无论是提高资产的利用率,还是对未来比特币生态的整体发展,都具有潜在的重要意义。

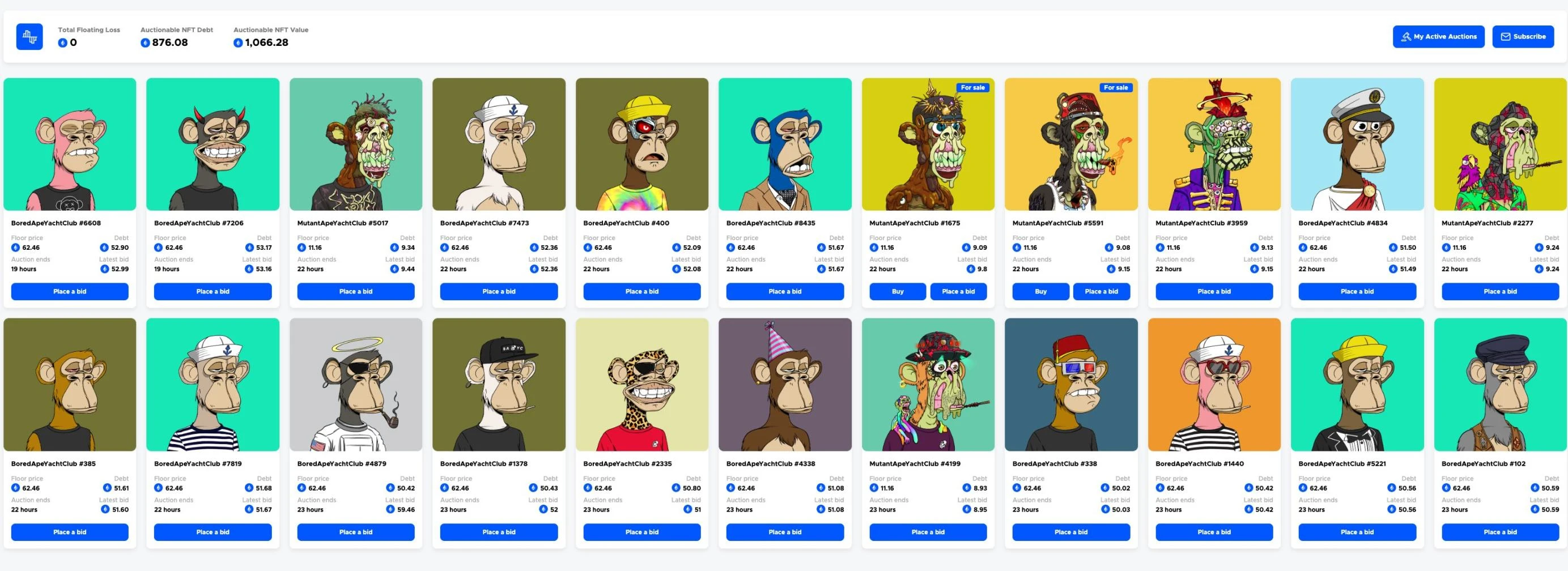

BendDAO 并不是第一次做这种增强流动性的布局——早在以太坊 NFT 叙事方兴未艾之时,BendDAO 就将目光瞄向了整个生态里最重要的一块蛋糕,即蓝筹 NFT 市场。通过“点对池”设计以及双向挖矿激励,BendDAO 很快就吸引了对资金效率极为敏感的蓝筹 NFT Holder 们,至此一个又一个 BAYC 被放入质押池中。

然而 BendDAO 本身的设计以及市场接连不断的暴雷事件,使得清算事件接二连三的发生,尽管项目方在 8 月份的清算事件过后很快调整了清算机制, 将清算阈值由 90% 逐步降低至 70% ,拍卖周期由 48 小时调整为 4 小时,取消“首次投标要高于地板价 95% ”的限制等。但依然还是无法避免流动性危机的产生。

随着市场对 NFT 的狂热逐渐消退,蓝筹 NFT 在这一年也陷入了阴跌困局中,头部项目的地板价离最高点纷纷腰斩一半有余,原本人声鼎沸的 NFTFi 叙事也变得鲜少有人问津。

BendDAO 此次的尝试,与其说是主动求变,更不如说是被市场大势所趋带动下的一种无奈之举——铭文和 Launchpad 热潮之下,HOOK,LEVER 等项目纷纷转型,而 BendDAO 也选择了这条路,他们此次的尝试能否成功?时间会给出答案。