原创 | Odaily星球日报

作者 | Azuma

今日午后,加密货币市场短线急跌,比特币回落至 43000 美元下方,一小时内全网爆仓逾 3000 万美元。

环顾同一时间的消息面动态,对行情走势影响最大的莫过于市场开始传播“部分用户表示已收到来自 Mt.Gox 的赔偿款”。

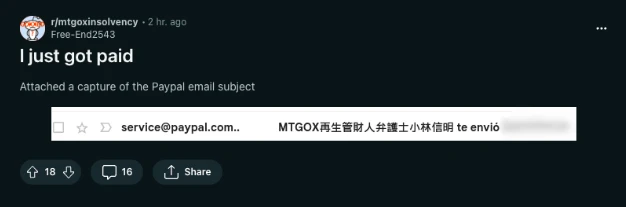

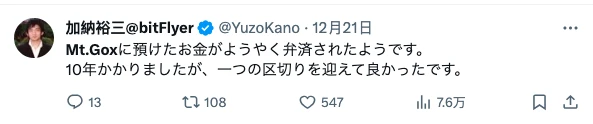

经 Odaily星球日报查证,除了目前多家媒体所报道的 Reddit 用户 @Free-end 254 声称已收到赔款之外,早在 12 月 21 日,便已有多位日语区用户在社交媒体上发声称已收到赔偿,其中还包括日本头部交易所 bitFlyer 的创始人加纳裕三。

Free-end 254 声称收到赔款。

加纳裕三表示 Mt.Gox 已开始赔款。

社交媒体上可查到的最早的关于赔款启动的消息。

综合目前多位用户的披露来看,本次偿还系以法币形式(日元),渠道则是通过 PayPal 支付。

查询 Mt.Gox 过往曾披露过的赔偿计划可知,Mt.Gox 曾在今年 9 月将原定于 2023 年 10 月 31 日的赔款(基础还款、提前一次性还款和中期还款)截止日期推迟至 2024 年 10 月 31 日,但同时也表示对于已经向 Mt.Gox 提供了必要信息的债权人,预计将于今年年底开始依次赔偿。

而在 11 月中旬,Mt. Gox 破产清算人小林信明曾再次通过邮件告知用户,正努力在 2023 年内开始进行现金偿还,然而鉴于债权人众多,偿还过程将可能持续到 2024 年。此外,赔偿给具体债权人的具体时间并未确定,因此无法提前通知每个债权人获得赔偿的具体时间,但债权人可以在其赔偿文件系统中检查实时状态。

值得一提的是,在 11 月 22 日发送给债权人的另一份文件中,小林信明还指出其已于 11 月 17 日从破产信托中赎回了 70 亿日元(价值约合 4690 万美元)以进行后续的赔偿操作,该笔赎回完成后信托内的剩余资产价值约为 88 亿日元(约合 5896 万美元)。

结合上述信息可知,本次 Mt.Gox 针对部分用户所进行的赔款基本符合了小林信明此前所预告的赔偿节奏,资金则大概率来自于小林信明 11 月 17 日从破产信托中赎回的 70 亿日元。

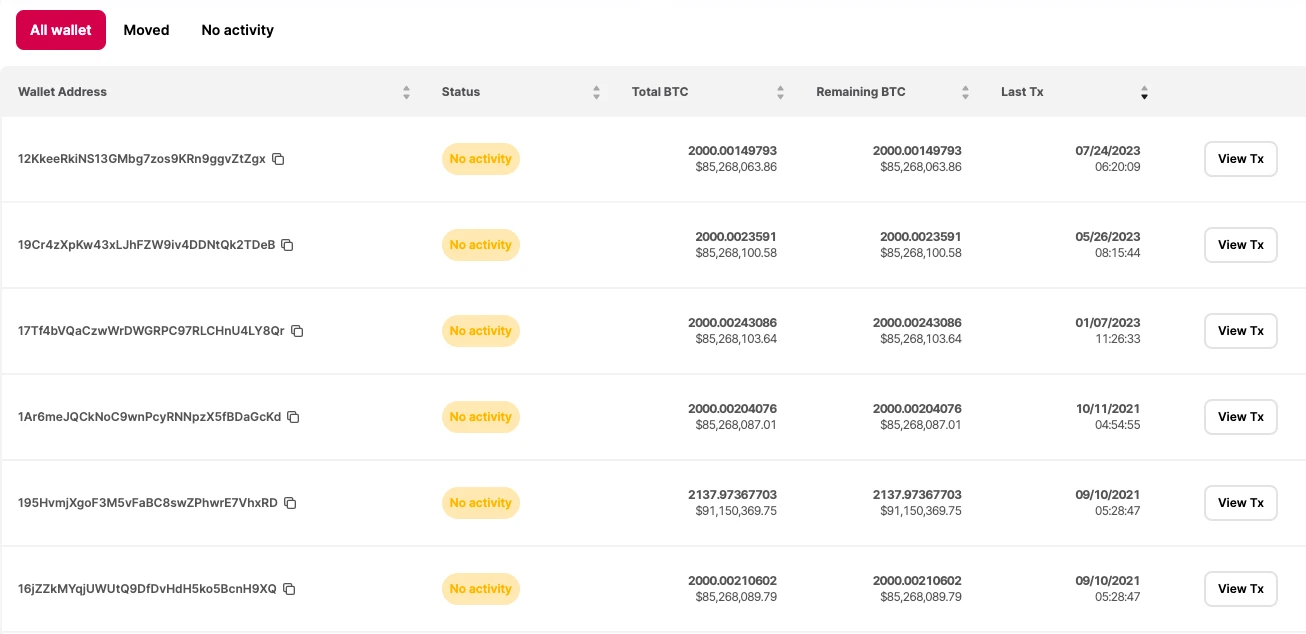

至于 Mt.Gox 是否正在砸盘?结合 Unlocks 对于 Mt.Gox 所披露的 BTC 钱包的追踪情况可知,Mt.Gox 相关钱包最近的一笔 BTC 链上动态发生在 2023 年 7 月 24 日,该笔交易也仅仅转出了极小额的 BTC(约 1 美元),看起来更像是在检查地址控制权限。

Mt.Gox 相关钱包动态追踪。

最近一笔交易仅涉及小额转账。

综合来看,目前可以确认的信息包括,Mt.Gox 历经十年之久确实已启动了对部分客户的赔偿,但赔偿暂时均为法币形式,其所持有的 BTC 至少当前从链上追踪状态来看并未出现异动迹象。