原创 | Odaily星球日报

作者 | 南枳

12 月 18 日 19: 03 ,在比特币区块高度达到 821716 时,Nostr Assets Protocol 的首次 Fair Mint 抽奖环节正式开始。随着前几十次抽奖的进行,参与用户发现出现了“幸运度”极高的个别抽奖池子,仅需投入约 3000 枚抽奖代币(Treat 和 Trick,下文简称双 T),就能获得 2160 枚 NOSTR 的头奖。而目前 NOSTR 的场外 OTC 价格已经来到 4 U/枚以上,接近无成本盈利 1 万美元。

Odaily 将于本文复盘各池子投入情况,以及抽奖策略情况,作为后续相似活动的参考。

Fair Mint 规则简述

Nostr Assets Protocol 的首次 Fair Mint 分为投入、抽奖、分发环节,前两个环节细节如下:

投入阶段

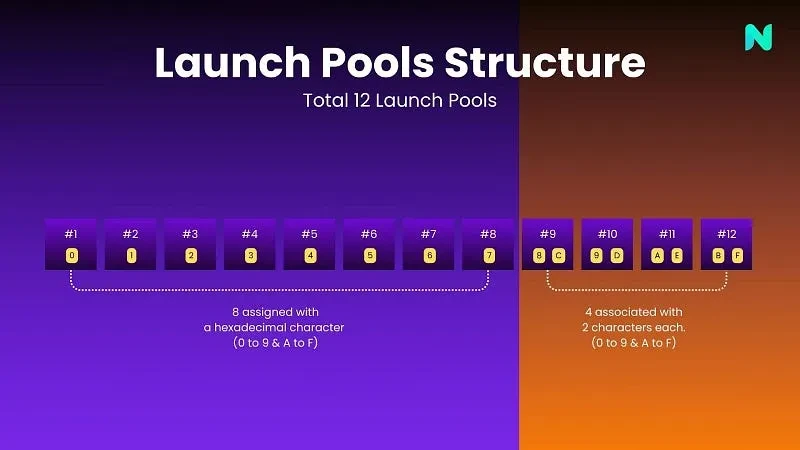

开始时间为 2023 年 12 月 11 日。官方设置了 12 个奖池,后四个奖池获奖概率为前八个奖池的双倍。

用户选择 12 个奖池中的 1 个,投入 Treat 和 Trick 资产,并获得池内排名。投入阶段可以持续增加投入资产,排名也是实时的,直至阶段结束。

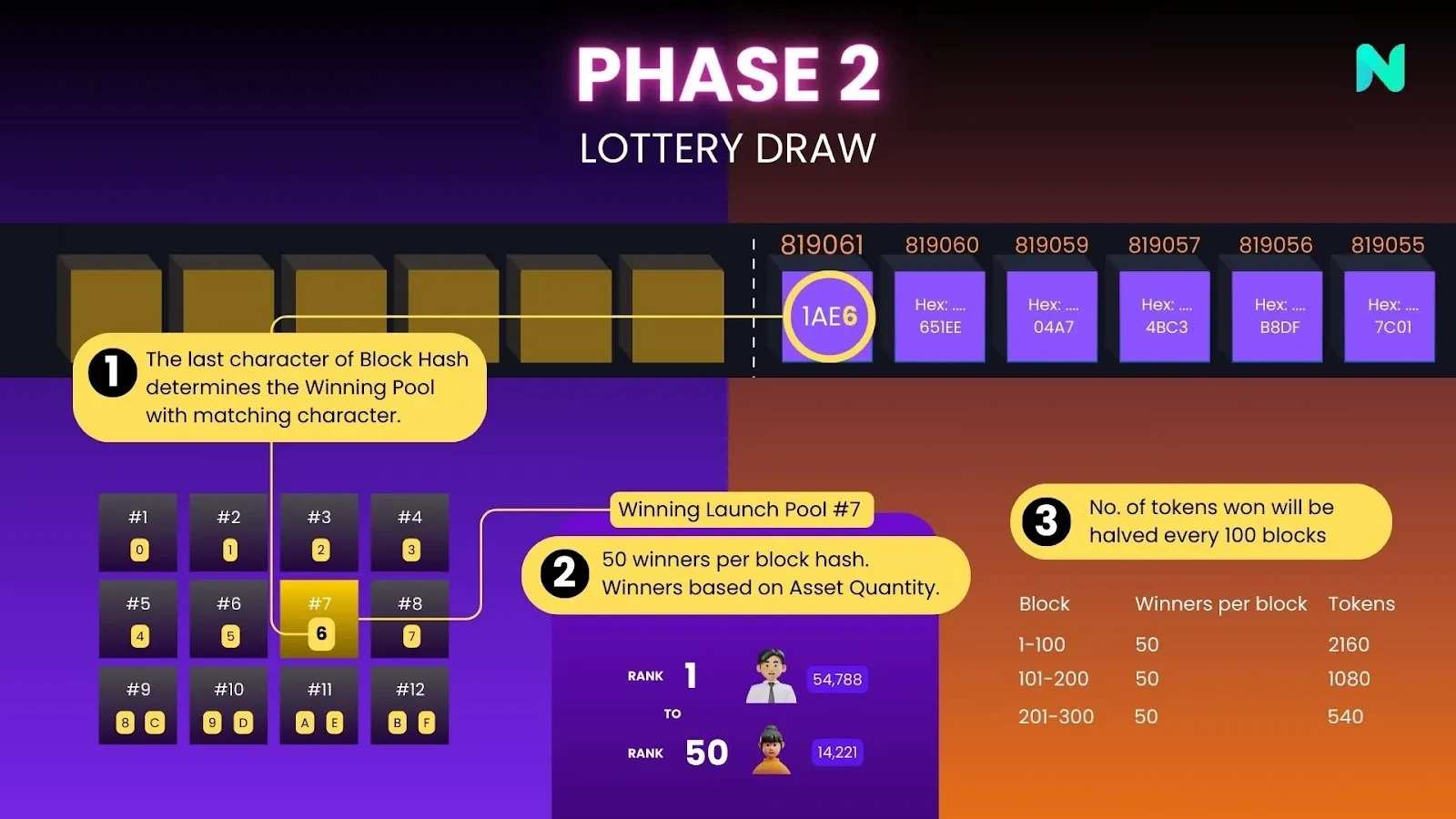

抽奖阶段

每个区块,按照区块哈希值的十六进制尾号,选择 12 个奖池中的 1 个;

抽中的奖池前 50 名获得一次奖励(再次抽中则为 51-100 名);

共抽取 300 次, 15000 个获奖地址,前 100 次获得 2160 枚 NOSTR, 101-200 名为 1080 枚, 201-300 名为 540 枚。

理论策略与实际情况

据官方公布,目前的双 T 流通量约8700 万枚(总量 4.2 亿枚),按照均分计算,则每个地址投入 5600 枚(全凭运气抽,实际上不会有这样的情况)。按照产出与投入成正比计算,三档投入比例为 4: 2: 1 ,因此最低投入数为 8700000/15000/7* 3 = 2484 枚,最高为 2484 × 4 = 9936 枚。

而最终的抽奖结果如下图所示,有以下几个结论:

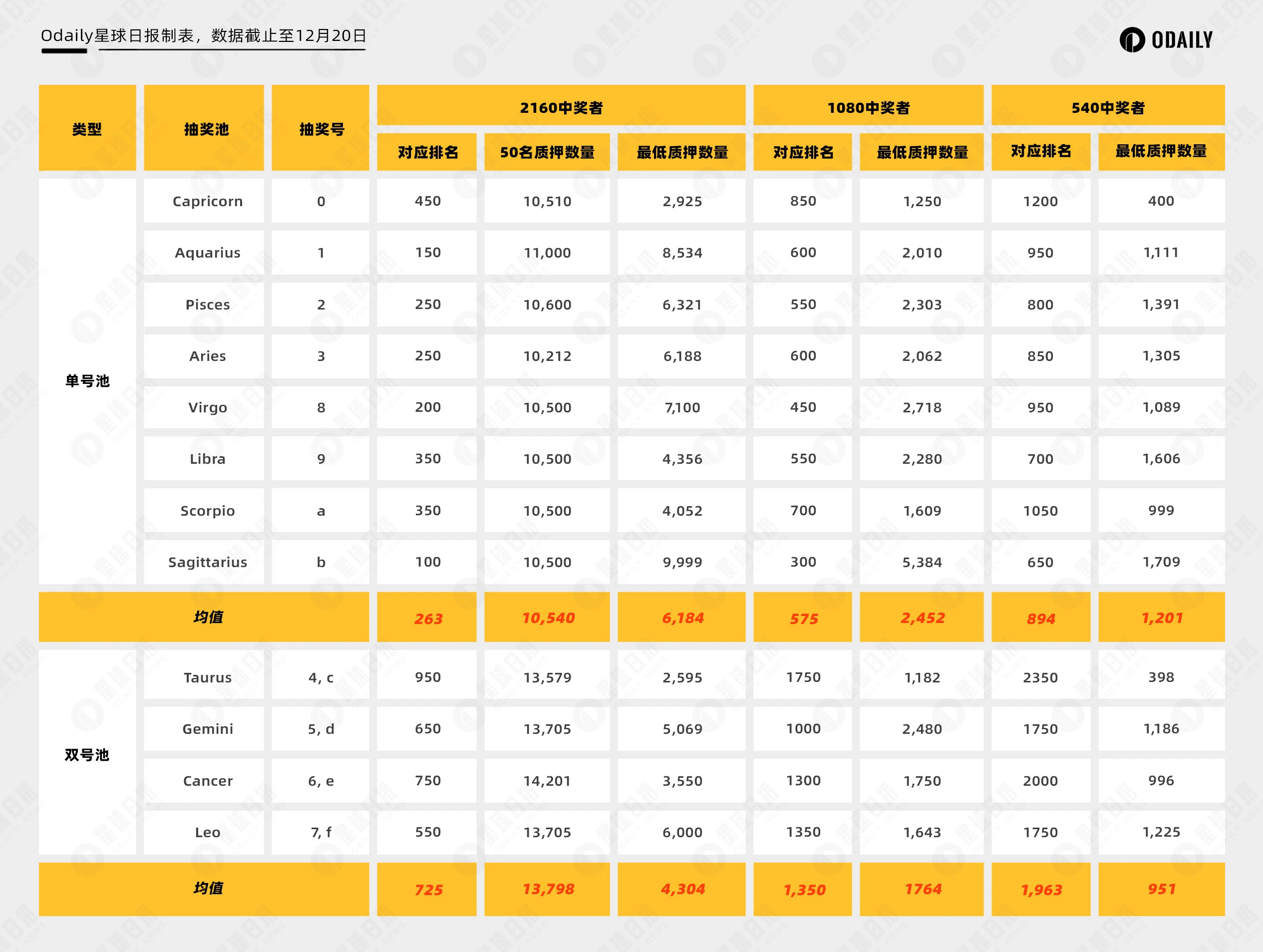

双号池的平均幸运程度好于单号池,随着抽奖的进行逐步恢复正常概率(但最终未完全均衡);

单号池和双号池各出现了一个极度幸运的池子 Capricorn 和 Taurus,即摩羯座和金牛座,抽奖号为“ 0 ”和“ 4, c”。这两个池子全程保持高幸运程度,并未向正常概率接近;

另外单号池还出现了一个特别倒霉的 Sagittarius(人马座),抽奖号为“b”,也是全程保持高倒霉程度。

为何获奖所需数量显著低于理论值?

例如在 Gemini 池中,有 766 名用户投入了少于 400 枚的双 T,即使在幸运池中也不可能获奖,则相应的至少约有 15 万枚双 T 浪费,随机抽取部分池子情况如下:

双号池 Taurus 中, 785 名用户少于 400 枚;

双号池 Leo 中, 684 名用户少于 400 枚;

单号池 Scorpio 中, 511 名用户少于 400 枚;

单号池 Aries 中, 517 名用户少于 400 枚;

基于以上数据,至少有百万枚双 T 以接近零的中奖概率投入了池中。进一步地,单号池约 800 名用户少于 1200 枚,双号池约 1100 名少于 950 枚,意味着近千万枚双 T 获奖概率低,因此有结论如下:

存在很多超小量投入博小概率幸运的投入策略,但投入过少,导致正常投入的概率增加;

总投入量约 7200 万,占流通量的 82.7% ,提升了概率;

出现了很多名一次投入 5 万枚以上双 T 的用户,最多者在一个账户中投入了 25 万枚,产生了极大的浪费,导致其他用户概率增加。

理论计算:有多幸运就有多倒霉

对于双号池,其单次抽中的概率应该是 12.5% ,理论抽中次数是 37.5 次,而 Taurus 抽中了 47 次。在三百次的标准“有放回抽样”中(抽中可能性从 0 次到 300 次均有,概率不同),抽中 37 次或 38 次的概率分别为 6.96% 和 6.88% ,而抽中 47 次的概率仅为 1.74% ,可以说 Taurus 获得了四倍的幸运加成。

而对于倒霉的 Sagittarius 而言,理论应抽中 18.75 次,最终抽中了 13 次。在三百次的标准“有放回抽样”中,抽中 19 次的概率为 9.4% ,而抽中 13 次的概率 3.9% ,Sagittarius 的倒霉程度放大了 2 倍。

活动收益如何?

在 Nostr 公布使用双 T 进行抽奖前,双 T 的价格约为 0.2 USDT 以上,后续公布后开始飙升,主要区间在 0.35 USDT~ 0.5 USDT 之间,在抽奖前因为需要补位冲名次,一度上升至 0.7 USDT。

而截止发文时,NOSTR 场外的价格约为 4 U/枚,则单号最大收益约为 8000 USDT。

截止发文时,双 T 的市场价格约为 0.39 USDT,与平均交易价格相近,收益率根据不同用户成本变化极大,但多数用户可以做到接近 0 成本,对于空投用户则大幅获利。

小结

Nostr Assets 使用哈希值进行抽奖的方式理论上较为公平,但由于抽奖次数仍不够多,导致结果不能符合大数定律。若后续 Nostr Assets 仍使用双 T 进行类似的抽奖,建议有足够数量代币的用户分号以平均概率,避免极端情况。