楼兰财经认为:核心通胀仍表现出较强的粘性。未来面临的主要干扰因素是美联储继续缩表过程中可能发生的金融风险事件。

——————————————————————————————————————

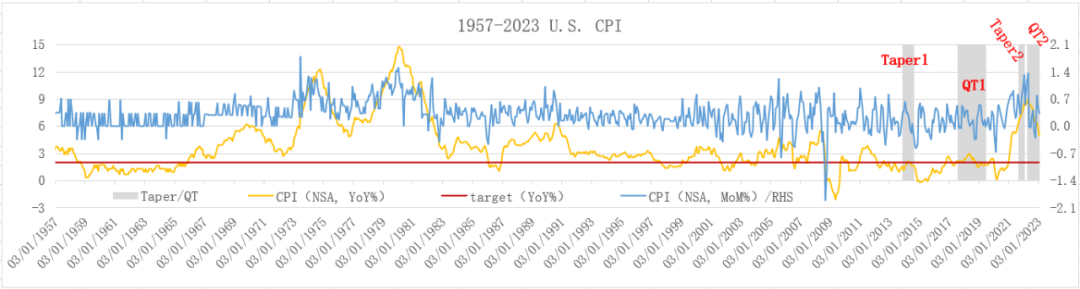

01美国3月CPI

2023年3月,美国CPI环比上涨0.3%,比2月低0.3个百分点;同比上涨5%,比2月大幅回落1个百分点,为本轮通胀过程中最大的月度回落幅度,主要原因包括美联储紧缩政策抑制总需求打击通胀取得效果、国际原油价格同比大幅下跌等。与美国本轮通胀峰值(2022年6月同比涨幅9.1%)相比,2023年3月CPI已经累计放缓4.1个百分点,同比涨幅创23个月最低,美联储打击通胀的努力取得较大进展。如图1所示(非季调)。

【图1】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

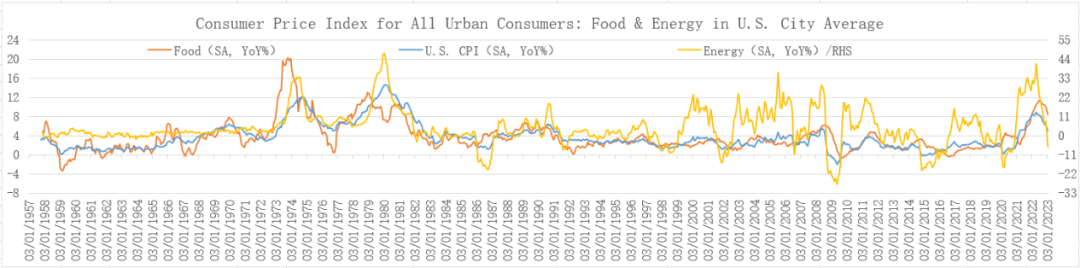

2023年3月,美国CPI同比上涨5%。其中,食品价格同比上涨8.5%,比2月低1个百分点;能源价格同比下跌6.4%,2月上涨5%。能源价格同比大幅下跌是3月CPI涨幅大幅放缓的重要原因。如图2所示(季调)。

【图2】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

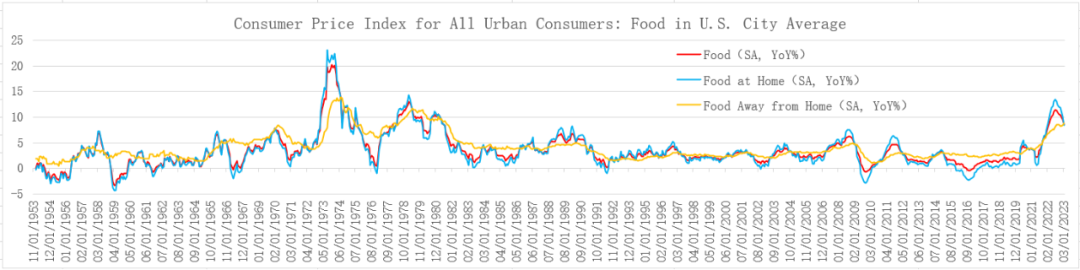

1、食品价格

2023年3月,美国食品价格同比8.5%,为13个月最低。其中家用食品价格同比8.3%,比2月低1.8个百分点,创14个月最低;外出用餐价格同比8.8%,比2月快0.4个百分点,创1981年9月以来最快。如图3(季调)。

【图3】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

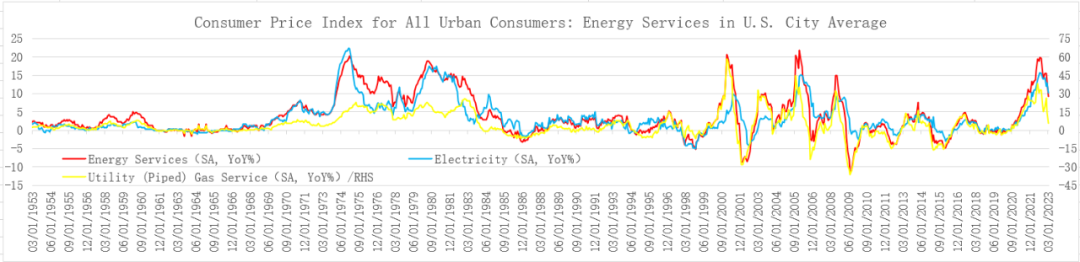

2、能源价格

2023年3月,美国能源价格同比下跌6.4%,为2021年2月以来首次下跌。其中,能源商品价格同比下跌17%,跌幅比2月扩大15.6个百分点,为28个月最低;能源服务价格同比上涨9.2%,比2月低4.1个百分点,为18个月最低。如图4所示(季调)。

【图4】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

1)能源商品

2023年3月,美国能源商品价格下跌17%。其中,汽油价格同比下跌17.4%,跌幅比2月扩大15.4个百分点,创28个月最低;燃油价格同比下跌10.4%,为2021年2月以来首次下跌,2月上涨5.7%。如图5所示(季调)。

【图5】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

2)能源服务

2023年3月,美国能源服务价格同比上涨9.2%。其中,电力价格同比10.2%,比2月低2.7个百分点,创13个月最低;管道天然气价格同比5.5%,比2月回落8.8个百分点,创26个月最低。如图6所示(季调)。

【图6】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

数据表明,美国大部分部品和服务价格同比涨幅持续回落,其中能源商品价格同比出现较大幅度的下跌,推动整体CPI大幅放缓,通胀形势好转。

02美国3月核心CPI

2023年3月,美国核心CPI环比上涨0.5%,比2月低0.2个百分点;但同比上涨5.6%,比2月小幅反弹0.1个百分点,显示美国核心通胀仍有粘性,主要原因包括劳动力市场持续紧张、服务业通胀压力较大,以及房租继续加快上涨。如图7所示(非季调)。

【图7】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

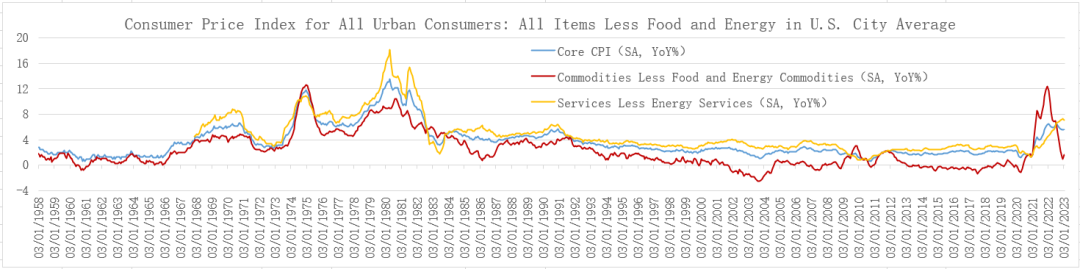

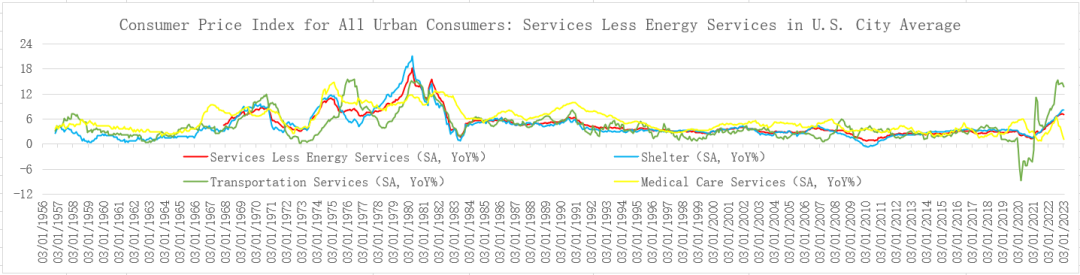

2023年3月,美国核心CPI同比上涨5.6%。其中,核心商品(扣除食品和能源商品)价格同比上涨1.6%,比2月加快0.6个百分点;核心服务(扣除能源服务)价格同比上涨7.1%,比2月低0.2个百分点,为20个月以来首次回落。如图8所示(季调)。

【图8】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

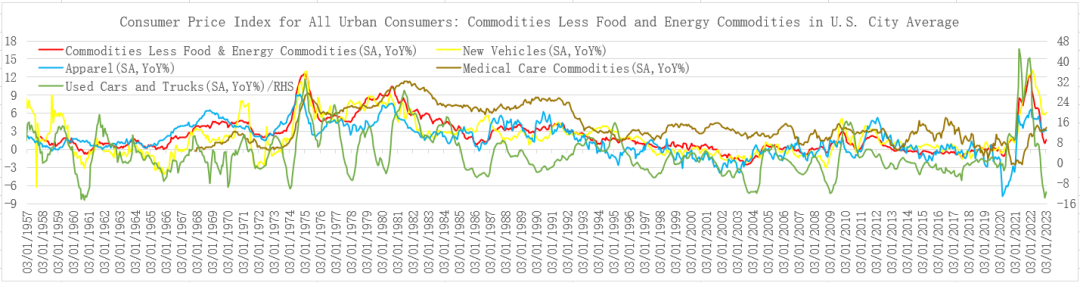

1、核心商品(扣除食品和能源商品)价格

2023年3月,美国核心商品(扣除食品和能源商品)价格同比上涨1.6%。其中,其中,新车价格同比上涨6.1%,和2月加快0.3个百分点,比本轮峰值(2022年4月13.2%)回落7.1个百分点;二手车价格同比下跌11.2%,跌幅比2月缩窄2.4个百分点,本轮峰值为2021年6月同比上涨44.9%;服装价格同比上涨3.2%,比2月低0.1个百分点,比本轮峰值(2022年3月6.7%)回落3.5个百分点;医疗用品价格同比上涨3.6%,比2月加快0.4个百分点,比本轮峰值(2022年8月4.1%)回落0.5个百分点。如图9所示(季调)。

【图9】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

2、核心服务(扣除能源服务)价格

2023年3月,美国核心服务(扣除能源服务)价格同比上涨7.1%。其中,住房支出价格同比上涨8.2%,比2月加快0.1个百分点,刷新1982年7月以来最快,表明2020年以来的房价快速上涨仍在向租金传导,预计房租涨幅会在2023年8月前后见顶回落;交通服务价格同比上涨13.8%,比2月低0.8个百分点,比本轮峰值(2022年10月15.3%)回落1.5个百分点;医疗服务价格同比上涨1%,比2月低1.1个百分点,比本轮峰值(2022年9月6.5%)大幅回落5.5个百分点。如图10 所示(季调)。

【图10】来源:美联储FED,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

核心CPI项目中,除租金同比持续加快上涨,新车价格也比2月有所反弹,二手车价格跌幅缩窄,加上工资上涨仍然较快,因此核心通胀仍表现出较强的粘性。

03美国通胀形势

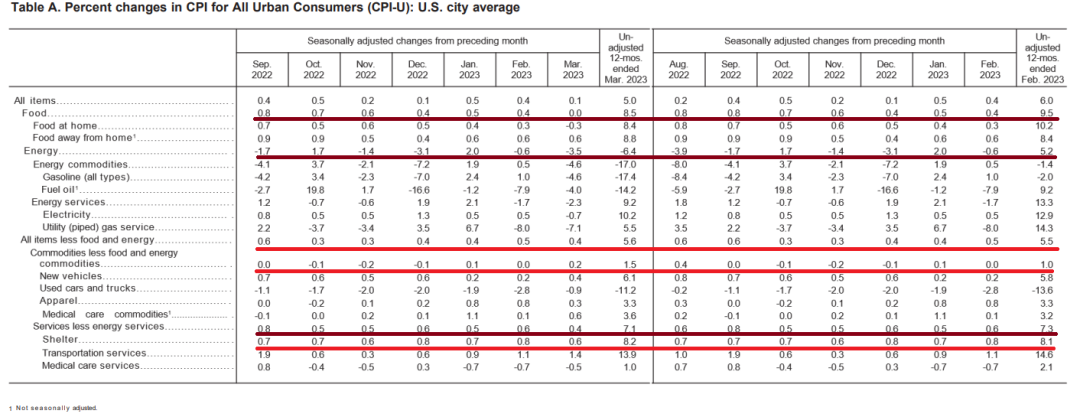

美国3月和2月的CPI细分数据如下(非季调)。整体CPI中,3月食品价格和能源价涨幅均呈回落趋势,其中食品价格同比上涨8.5%,比2月低1个百分点;能源价格同比下跌6.4%,2月为上涨5.2%。

来源:美国劳工统计局BLS,整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

核心CPI中,核心商品(扣除食品和能源商品)价格同比上涨1.5%,比2月加快0.5个百分点;核心服务(扣除能源服务)价格同比上涨7.1%,比2月低0.2个百分点。值得注意的是,核心服务价格中,比重最大的租金同比上涨8.2%,比2月加快0.1个百分点,成为推动3月核心CPI小幅反弹的主要因素。

美联储3月会议纪要显示,美联储预计2023全年美国PCE通胀率为2.8%,核心PCE通胀率为3.5%。其中,核心商品价格涨幅有望进一步回落,住房支出成本(租金)涨幅年内将见顶回落,扣除租金的核心服务通胀将缓慢降低,原因是名义工资涨幅将逐步回落;综合考虑生产、劳动力市场转弱,2024年核心通胀压力将显著缓解。由于能源价格大幅下跌,食品价格涨幅显著回落,2023年整体通胀率将大幅下行。

2024-2025年,预计PCE通胀、核心PCE通胀都将回落至接近美联储目标2%的水平。3月部分银行出现流动性风险将造成信贷条件收紧,这在一定程度上会抑制经济增长、就业和通胀。如果银行超预期减少信贷发放,会对经济活动和通胀产生下行压力。

04美联储政策前瞻

美国3月CPI数据公布后,市场预计美联储5月会议加息25个基点的概率小幅修正为66.8%。市场对政策的分歧仍然存在,且3月核心CPI小幅反弹,通胀压力继续维持较高水平。综合考虑各种因素,可以认为美联储5月加息基本确定,然后大概率宣布暂停加息,但会继续实施缩表。

美国3月核心CPI粘性较强的主要原因有两个,一是前一阶段房价快速上涨仍在向租金传导,租金同比涨幅仍在加快,但预期会在2023年8月前后见顶回落;二是劳动力市场仍然紧张,但已经出现边际转弱迹象,失业金申请人数增加,职位空缺数量减少,工资增速放缓,预计2024年服务业通胀压力会显著缓解。

继2023年2月加息25个基点、美联储政策利率超过美国核心PCE通胀之后,3月美联储加息25个基点、预计政策利率超过PCE通胀(数据未公布),预计美联储5月加息25点,政策利率将超过CPI,到时候只有核心CPI仍高于政策利率。此时暂停加息、继续缩表,紧缩政策效应继续传导,预计下半年政策利率阶段性超过核心CPI通胀指标、实际利率全面转正可期。目前市场对美联储利率政策的预期如下。

来源:芝商所美联储观察工具(CME FedWatch Tool),整理:对冲研投 bestanalyst.cn/楼兰财经Kroraina Finance

未来一段时间是美国经济转弱、周期转换的关键时期,在不同的阶段,美联储政策信号和金融市场的表现会有相应变化。如果美联储在5月会议加息25个基点的同时,正式宣布加息周期结束,市场压力将有所减轻,预计美股会有短期反弹行情;暂停加息之后的关键是关注美国经济数据隐含的衰退信号,出现衰退信号将利空美股。一旦美国衰退被证实,关注的重点转为美联储市场沟通中传递的政策转向信号,如果美联储释放宽松信号将利多美股。

未来面临的主要干扰因素是美联储继续缩表过程中可能发生的金融风险事件。硅谷银行流动性危机造成的冲击已经告一段落,但要警惕其他风险因素的积聚。美联储上一轮缩表后期,2019年9月17日,美国一般抵押融资(GCF)市场流动性紧张、利率暴涨,市场一度陷入短期动荡。美联储吸取上次的教训,于2021年7月28日创设了常备回购便利(SRF)工具,提前为本轮加息缩表做好了准备。如果缩表到一定阶段出现系统流动性紧张状况,美联储可以启用SRF工具应对。