随着《2022 年打击洗钱及恐怖分子资金筹集(修订)条例草案》在 2022 年 12 月获立法会通过,专为提供非证券型代币交易服务的(中心化的)虚拟资产交易平台而设的全新发牌制度将在 2023 年 6 月 1 日生效。

今日香港证券及期货事务监察委员会(证监会)就适用于虚拟资产交易平台营运者的建议规定展开咨询。

待新制度实施后,所有在香港经营业务或向香港投资者积极推广其服务的虚拟资产交易平台,不论它们有否提供证券型代币交易服务,将需获证监会发牌并受其监管。

在证监会发布的长达 312 页、近 20 万字的咨询文件中,阐述了适用于持牌虚拟资产交易平台营运者的主要建议监管规定,以及有关新制度的过渡安排和其他实施细节。该咨询文件邀请市场参与者和相关人士于 2023 年 3 月 31 日或之前,就咨询文件讨论的各项建议或可能对这些建议产生重大影响的相关事宜提交书面意见。

对此,Foresight News 梳理了港证监会的咨询文件要点,以下为核心要点:

1、港证监会将发布《适用于虚拟资产交易平台营运者的指引》(《虚拟资产交易平台指引》)。

2、获证监会发牌的虚拟资产交易平台须遵守《虚拟资产交易平台指引》。

3、建议的《虚拟资产交易平台指引》根据适用于《证券及期货条例》下的持牌平台营运者的现行监管规定(《虚拟资产交易平台条款及条件》)拟备而成。

4、在《打击洗钱条例》下的虚拟资产服务提供者制度生效后,现时作为发牌条件施加于《证券及期货条例》下的持牌虚拟资产交易平台的《虚拟资产交易平台条款及条件》将被取代。证监会将会从现有《证券及期货条例》下的持牌平台营运者的牌照中删除相应的发牌条件。日后,所有平台营运者(不论是否根据《证券及期货条例》及 / 或《打击洗钱条例》 获发牌)将须受到《虚拟资产交易平台指引》的规限。

5、证监会建议容许各类投资者(包括零售投资者)使用由持牌虚拟资产交易平台营运者提供的交易服务,前提是有关平台遵守相关妥善投资者保障措施,包括对投资者进行正式评估及培训规定、评估客户的风险承受水平和风险状况,以及根据用户个人财政情况为每名客户设定上限(机构专业投资者除外),设立代币纳入及检讨委员会等。

7、证监会还列出了平台营运者在纳入虚拟资产以供买卖时应考虑的一般纳入准则,如管理层或开发团队的背景、监管状况、虚拟资产的供求、市场成熟程度及流通性、技术层面、推广材料、开发情况、市场风险、法律风险、效用或用力等。另外,持牌平台营运者如有意向零售客户提供虚拟资产,亦应确保所挑选的虚拟资产属于合资格的大市值虚拟资产,并符合下列特定代币纳入准则,即,「符合资格的大市值虚拟资产」指获纳入由至少两个独立指数提供者所推出的至少两个「获接纳的指数」中的虚拟资产,该该指数应是可供投资的,有关的成分虚拟资产应具备充足的流通性。

8、持牌平台营运者如有意提供符合一般代币纳入准则但不符特定代币纳入准则的虚拟资产以供零售投资者买卖,应向证监会提交一份建议书以供讨论。

9、持牌平台营运者应披露足够的产品资料,使客户能够评估其投资的状况,如:

a)虚拟资产在该平台上的价格及成交量,例如过去 24 小时的价格及成交量;

b)有关虚拟资产管理团队或开发者的背景资料;

c)虚拟资产的发行日期;

d)对虚拟资产的条款和特点的扼要描述;

e)虚拟资产官方网站的链接 ( 如有 );

f)虚拟资产智能合约审计报告的链接 ( 如有 );

g)若虚拟资产设有投票权,持牌平台营运者将如何处理这些投票权。

10、关于投资者保护保险规定,证监会建议:

a)持牌平台营运者就与保管客户虚拟资产有关的风险应设有经证监会核准的补偿安排。

b)持牌平台营运者应每日监察其所保管的客户虚拟资产的总值,确保遵守有关的补偿规定。

c)持牌平台营运者如为遵从有关规定而拨出自身的资金或与其属同一公司集团的法团的资金,便应确保该等资金乃以信托方式持有并指定作有关用途。该等资金亦应从持牌平台营运者、其有联系实体或与持牌平台营运者属同一公司集团的法团的资产分隔出来。

11、根据《证券及期货条例》下的现行制度,持牌平台营运者不得就虚拟资产期货合约或相关衍生工具进行销售、交易或买卖。随着业界对销售虚拟资产衍生工具兴趣渐浓,证监会希望更清楚地了解持牌平台营运者可能首先采取的业务模式和销售的虚拟资产衍生工具种类,以及市场需求。

12、证监会建议移除将《虚拟资产交易平台条款及条件》当中有关「证券型代币」的规定纳入《虚拟资产交易平台指引》内,日后,持牌平台营运者应遵守《虚拟资产交易平台指引》下的一般代币纳入准则,以及证监会将在适当时候发布的证券型代币分销指引。

13、对于持牌平台运营者,如有关虚拟资产仅售予专业投资者,持牌平台营运者只须于计划在其交易平台上加入或移除有关产品前预先通知证监会即可,而无须征求证监会批准。如有关虚拟资产是售予零售客户的,便会沿用先前的做法,即持牌平台营运者应就有关计划预先征求证监会批准,然后才可纳入有关虚拟资产以供买卖。

14、关于《打击洗钱条例》所订的虚拟资产转帐的特别规定,持牌平台营运者在以虚拟资产转帐的汇款机构身份行事时,便须取得和记录所需汇款人及收款人资料,并立即且安全地向收款机构提交该等资料;持牌平台营运者在以收款机构的身分行事时,便须取得和记录由汇款机构或中介机构提交的所需资料;以及对虚拟资产转帐对手方(即参与虚拟资产转帐的汇款机构、中介机 构或收款机构)进行尽职审查。

`

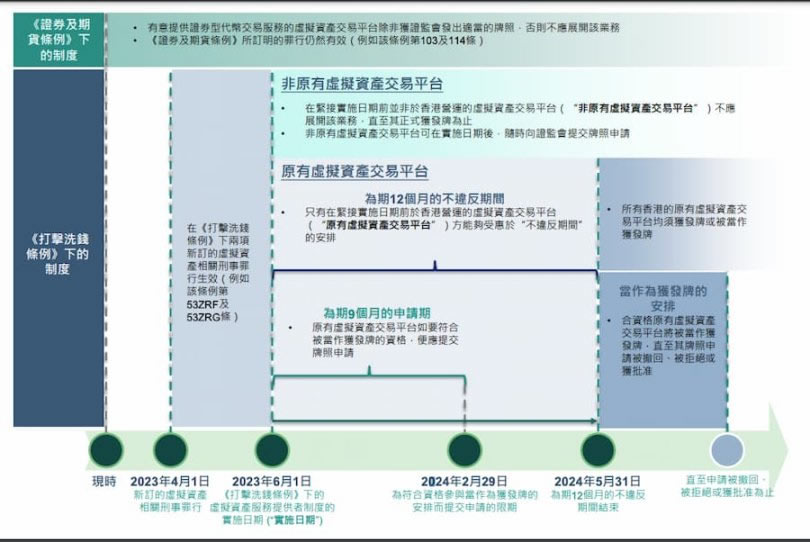

过渡安排

2023 年 6 月 1 日起,任何在香港经营其业务或是向香港投资者积极推广其服务的虚拟资产交易平台,如并无有效牌照,即属违反《打击洗钱条例》下的虚拟资产服务提供者制度中的发牌规定,除非符合参与过渡安排的资格。

证监会建议订立为期 12 个月的过渡期,以便《证券及期货条例》下的持牌平台营运者遵守与其现有客户或其现时销售的虚拟资产有关的规定。待《虚拟资产交易平台指引》、 《适用于持牌法团及获证监会发牌的虚拟资产服务提供者的打击洗钱指引》及其他指引的规定作最后定稿后,会提供过渡安排细节。

虚拟资产交易平台必须是原有平台,且在 2023 年 6 月 1 日前已于香港营运并设具意义且实质的业务,方合资格参与过渡安排。在符合《打击洗钱条例》条件后才可于 2023 年 6 月 1 日至 2024 年 5 月 31 日内继续在香港营运。具体考虑因素包括是否于香港成立发团、是否在香港有实体办公室、香港员工是否有中央管理或控制权、关键人员是否驻于香港、运作是否已投入服务并于香港拥有大量的客户及交易活动。

原有虚拟资产交易平台如要符合资格参与当作为获发牌的安排,必须在 2023 年 6 月 1 日至 2024 年 2 月 29 日期间(即由 2023 年 6 月 1 日起计九个月内)内,根据《打击洗钱条例》下的虚拟资产服务提供者制度在网上提交牌照申请。

在紧接 2023 年 6 月 1 日前并非于香港营运的虚拟资产交易平台,仅可在根据《打击洗钱条例》下的虚拟资产服务提供者制度获正式发牌后,方可于香港经营其业务或积极地 向香港投资者推广其服务。进行任何无牌活动乃属刑事罪行。