Author: Insightful Commentary

Disclaimer: This report is compiled and analyzed based on the research report "What the Iran Conflict Means for the Dollar: The Perfect Storm of Petrodollars" released by Deutsche Bank Research Institute on March 24, 2026, combined with extended knowledge points from Q&A discussions. It is for research reference only and does not constitute any investment advice.

Table of Contents

- I. The Underlying Logic of Dollar Hegemony

- II. The Historical Origin and Operating Mechanism of Petrodollars

- III. The Correlation Between Crude Oil and U.S. Treasuries

- IV. The Three Layers of Pressure on the Petrodollar System

- V. The Failure of Old Logic in the Current Conflict

- VI. Buffer Factors and Scenario Analysis

- VII. Conclusion: The Long-Term Implications of Slow Variables

The long-term legacy of the Iran conflict may lie in its impact on the foundation of the petrodollar system. The petrodollar recycling has supported the U.S. dollar's global reserve currency status since 1974: The world buys oil with dollars → Oil-producing countries' surpluses recycle back to purchase U.S. Treasuries → The dollar's dominant position in international trade is self-reinforcing. However, this system is facing superimposed pressures: pre-existing structural cracks before the conflict, new shocks triggered by the war, and the long-term threat posed by the energy transition. There is an interactive transmission mechanism between crude oil prices and U.S. Treasury yields. Understanding these mechanisms is crucial for judging the impact of the current geopolitical conflict on global asset prices.

Chapter I: The Underlying Logic of Dollar Hegemony

1.1 From the Gold Standard to the Oil Standard

To understand the current crisis, one must start with the historical evolution of dollar hegemony. The international status of the dollar is not static; it has undergone two major institutional transformations.

First Phase (1945–1971): The Bretton Woods System. After World War II, the United States, with its overwhelming economic and military power, led the establishment of an international monetary system centered on the U.S. dollar. Central banks could exchange dollars for gold from the Federal Reserve at a fixed rate of $35 per ounce. The dollar was essentially a "gold receipt," its credit backed by U.S. gold reserves.

Second Phase (1971–present): The Era of Pure Fiat Dollar. In August 1971, President Nixon announced the decoupling of the dollar from gold (historically known as the "Nixon Shock"), leading to the collapse of the Bretton Woods system. The dollar thus entered the era of pure fiat money, its value no longer backed by gold reserves but dependent on U.S. sovereign credit and the sustained global demand for dollar assets.

Key Question: After the gold decoupling, what maintained the dollar's global dominance? — The Petrodollar System.

1.2 Why "The World Saves in Dollars" Stems from "The World Pays in Dollars"

The dollar's reserve currency status is essentially a derivative of its trade currency status, not the other way around. Many people think the world uses the dollar because the U.S. is powerful, but the more accurate causal chain is:

- Global oil transactions are priced and settled in U.S. dollars.

- Oil is a core cost input for all manufacturing (from petrochemicals, fertilizers, transportation to factory operations).

- Companies naturally tend to price their end products in dollars, forming a natural hedge against dollar-denominated costs.

- The global trade system is thus dollar-denominated, generating large dollar surpluses.

- These surpluses are primarily invested in U.S. Treasuries, creating structural demand for dollar assets.

- Central banks accumulate dollar reserves to provide liquidity support when their currencies are under pressure.

This is a self-reinforcing closed loop, whose core driving force is the dollar pricing mechanism for oil.

1.3 Network Externality: Why Dollar Hegemony is So Hard to Shake

There is a concept in economics called "Network Externality"—the more users a currency has, the higher the value for each participant using it. This logic is identical to that of telephone networks or social platforms. The network effect of the dollar is reflected at three levels:

- Liquidity Advantage: The dollar asset market is the deepest and broadest globally, with the smallest bid-ask spreads and the lowest impact costs for large-scale transactions. This makes the opportunity cost of holding dollar assets the lowest among all currencies.

- Infrastructure Advantage: The SWIFT international settlement system and the Correspondent Banking system both operate with the dollar at their core. The default track for global cross-border payments is the dollar track.

- Contract Convention Advantage: Standard terms for commodity contracts and trade finance letters of credit are defaulted to dollar denomination. Changing this convention requires synchronized coordination among global trade participants, incurring extremely high transaction costs.

For this reason, "de-dollarization" has been called for decades but progress has been slow. Breaking this network requires a sufficiently large external shock or a competitor that can simultaneously provide alternative infrastructure. These two conditions are gradually converging in the current conflict.

Chapter II: The Historical Origin and Operating Mechanism of Petrodollars

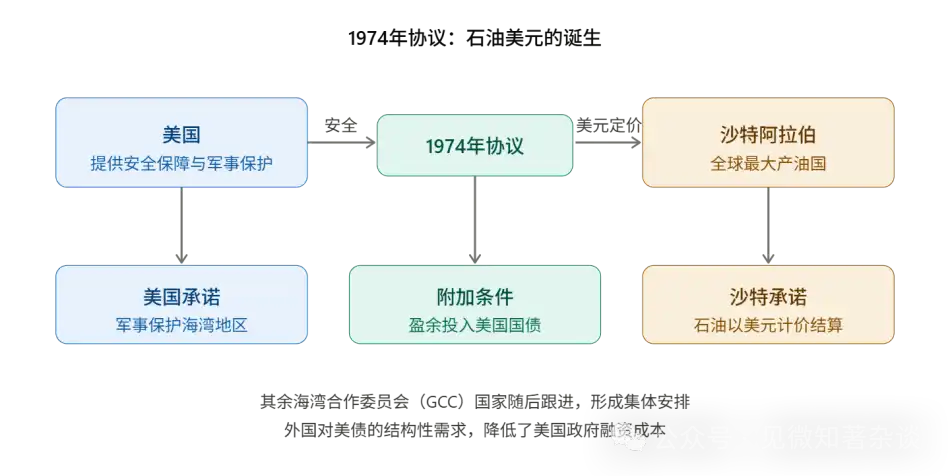

2.1 1974: A Historically Underestimated Deal

The origin of the petrodollar system can be traced back to the 1974 U.S.-Saudi agreement, but the deep meaning of this deal far exceeds its literal content.

-

Historical Context: After the collapse of the Bretton Woods system in 1971, the dollar lost its gold backing and faced a severe crisis of confidence. Meanwhile, the 1973 Arab oil embargo caused oil prices to quadruple in just a few months. The U.S. realized it must find a new way to anchor the dollar's global status.

Core Content of the Deal: Saudi Arabia agreed to price its oil exports in U.S. dollars and invest its oil surpluses in U.S. Treasuries; in return, the U.S. provided security guarantees and military protection. Other Gulf Cooperation Council (GCC) countries followed suit, forming a collective institutional arrangement.

Deep Strategic Implication: The U.S. used military power as collateral to back the dollar's credit. In essence, after the collapse of Bretton Woods, the dollar switched from a "gold standard" to an "oil standard"—its value was no longer backed by gold reserves but by the geopolitical ability to control global energy trade.

Implicit Subsidy Mechanism: The structural demand from oil-producing countries to buy U.S. Treasuries continuously suppresses the U.S. government's financing costs. This is equivalent to an indirect subsidy to the U.S. Treasury market from every instance of global economic growth driving energy demand. It is the most powerful and hidden economic advantage of dollar hegemony.

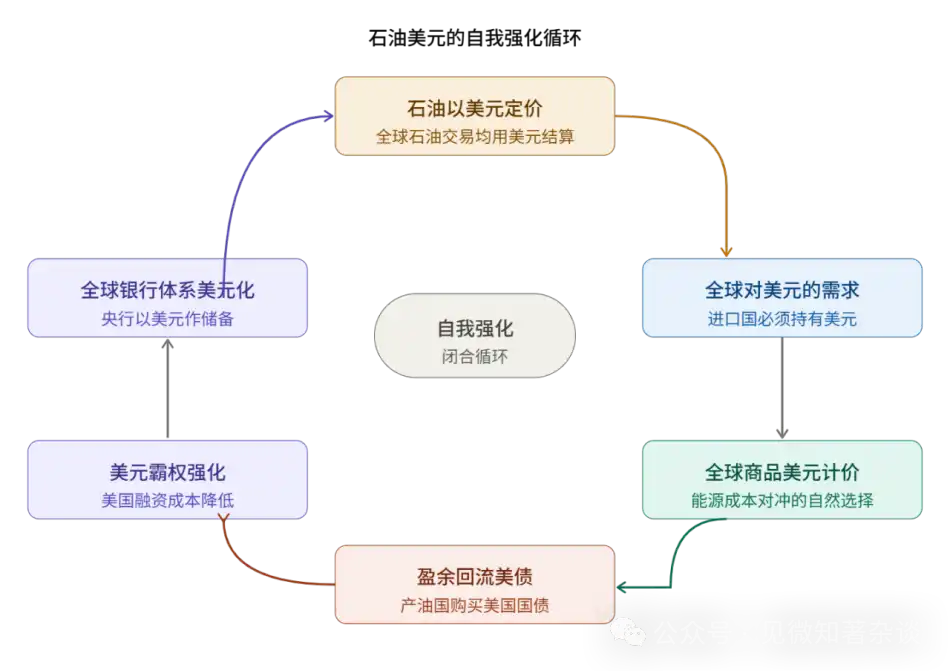

2.2 The Self-Reinforcing Cycle of Petrodollars: Six Nodes

The petrodollar cycle is not a simple causal chain but a closed loop consisting of six nodes, each reinforcing the others:

The key characteristic of this cycle is its self-reinforcing nature: The cost for any single participant to exit is extremely high because it must abandon the liquidity and convenience advantages brought by the entire network. This explains why, even as the relative international status of the U.S. declines, dollar dominance stubbornly persists.

Chapter III: The Correlation Between Crude Oil and U.S. Treasuries

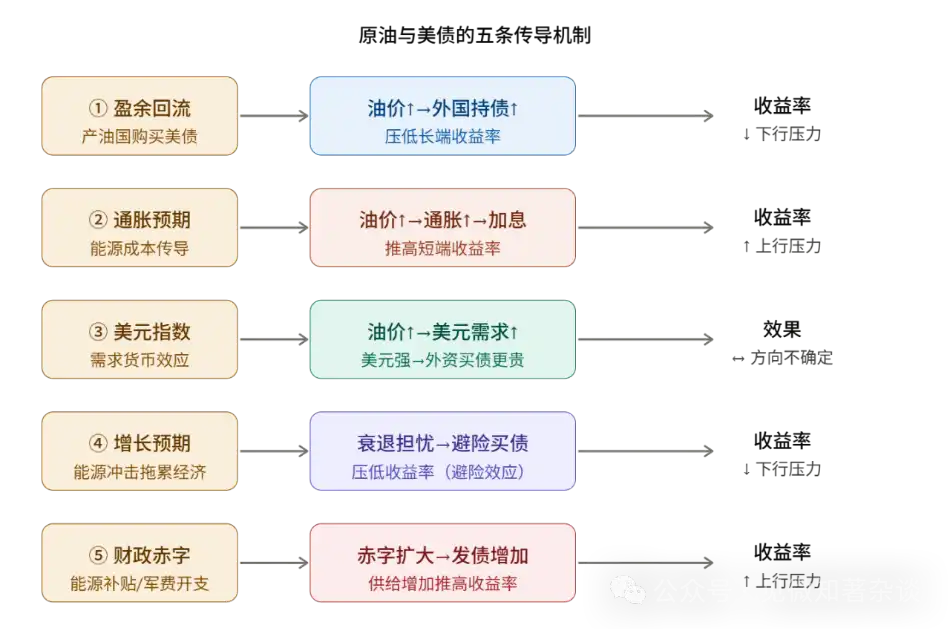

Understanding the relationship between oil prices and U.S. Treasury yields is one of the core analytical tasks of this report. This relationship is far more complex than "oil up, Treasuries up" or "oil down, Treasuries down". In fact, rising oil prices simultaneously activate five transmission mechanisms in different directions. The final net effect depends on the relative strength of these five mechanisms in a specific context.

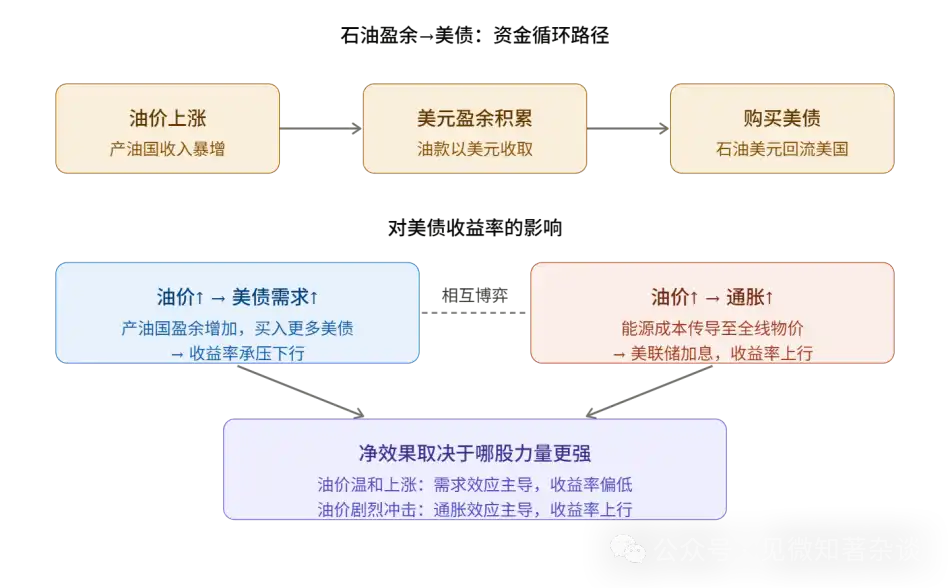

3.1 Mechanism One: Surplus Recycling Effect (Lowers Yields)

Transmission Path: Oil prices rise → Oil-producing countries' dollar income increases → Dollar surpluses accumulate → Purchase of U.S. Treasuries → Bond demand rises → Yields face downward pressure.

This is the most direct manifestation of the petrodollar cycle. Taking Saudi Arabia as an example, during the mid-2000s when oil prices rose from $30/barrel to $147/barrel, the dollar surpluses of GCC countries increased significantly, and their purchases of U.S. Treasuries rose markedly, creating sustained external demand.

Historical Case: 2004–2006, the Federal Reserve raised interest rates 17 consecutive times, raising the federal funds rate from 1% to 5.25%, but the 10-year Treasury yield remained almost unchanged. Then Fed Chairman Greenspan called this a "conundrum." One important academic explanation was petrodollar recycling—the demand from oil-producing countries to buy bonds, driven by rising oil prices, continuously suppressed long-term yields.

3.2 Mechanism Two: Inflation Expectation Effect (Raises Yields)

Transmission Path: Oil prices rise → Energy costs transmit to all prices → Inflation expectations heat up → Market expects Fed to raise rates → Short-term yields rise → Subsequently driving long-term yields higher.

Energy is a basic input for industrial production. Rising oil prices transmit to final consumer prices through direct channels (fuel costs) and indirect channels (transportation costs, raw material costs), producing broad inflationary effects. The Federal Reserve, as the ultimate gatekeeper of inflation, typically has no choice when facing inflationary pressure—it must tighten monetary policy, pushing market interest rates higher.

This mechanism works in the opposite direction to Mechanism One, forming a hedging relationship. Which one dominates depends on the nature of the oil price shock:

1) Demand-driven oil price rise (increased demand due to global economic boom): Usually, the surplus recycling effect is stronger, yields are lower.

2) Supply-shock driven oil price surge (geopolitical supply disruption): Usually, the inflation effect is stronger, with greater upward pressure on yields.

3.3 Mechanism Three: U.S. Dollar Index Effect (Direction Uncertain)

Transmission Path: Oil prices rise → Global demand for dollars increases (to buy oil, one must first buy dollars) → Dollar strengthens → The conversion cost of dollar assets for foreign investors rises → Foreign demand for bonds is marginally suppressed.

This mechanism is more subtle. Buying oil requires dollars. Rising oil prices mean increased global dollar demand, pushing the U.S. Dollar Index (DXY) higher. But a stronger dollar is a double-edged sword for U.S. Treasuries:

For domestic investors: No exchange rate impact, demand unchanged.

For foreign investors: A stronger dollar means a higher cost to convert their local currency into dollars, increasing the real cost of investing in U.S. Treasuries and marginally reducing their willingness to buy bonds.

Therefore, the net effect of this mechanism depends on the marginal influence of foreign investors in the Treasury market. The direction is uncertain, and it is usually a moderating factor that weakens other mechanisms.

3.4 Mechanism Four: Growth Expectation Effect (Lowers Yields)

Transmission Path: Oil prices surge sharply → Expectations of impaired economic growth → Market turns to safe-haven assets → U.S. Treasuries, as the world's safest asset, see capital inflows → Yields fall.

When a sharp rise in oil prices triggers fears of an economic recession, global funds flow into U.S. Treasuries seeking safety. This "flight to safety" effect can be very strong in extreme cases, even overwhelming the upward force of inflation expectations.

Historical lesson from 1979–1980: The Iranian Revolution triggered the second oil crisis. Oil prices surged while the global economy fell into stagflation. Fed Chairman Volcker, to break inflation expectations, raised the federal funds rate to 20%. This is an extreme case where the inflation effect压倒一切 other mechanisms. It also shows that when a supply shock is severe enough, the Fed's policy response becomes the decisive factor for yield movements.

3.5 Mechanism Five: Fiscal Deficit Effect (Raises Yields)

Transmission Path: Oil price shock → Governments of energy-importing countries are forced to expand energy subsidies + increase military spending → Fiscal deficit widens → Treasury supply increases → All else equal, bond prices fall, yields rise.

This mechanism is particularly prominent in the current conflict. War not only increases military spending but also forces governments to subsidize energy costs for households and businesses to prevent social unrest. This dual pressure widens the fiscal deficit. More importantly, as the scale of U.S. debt continues to expand, the market requires a higher yield premium to absorb the new supply, especially when foreign buyers are reducing their purchases.

3.6 Historical Pattern Comparison of the Five Mechanisms

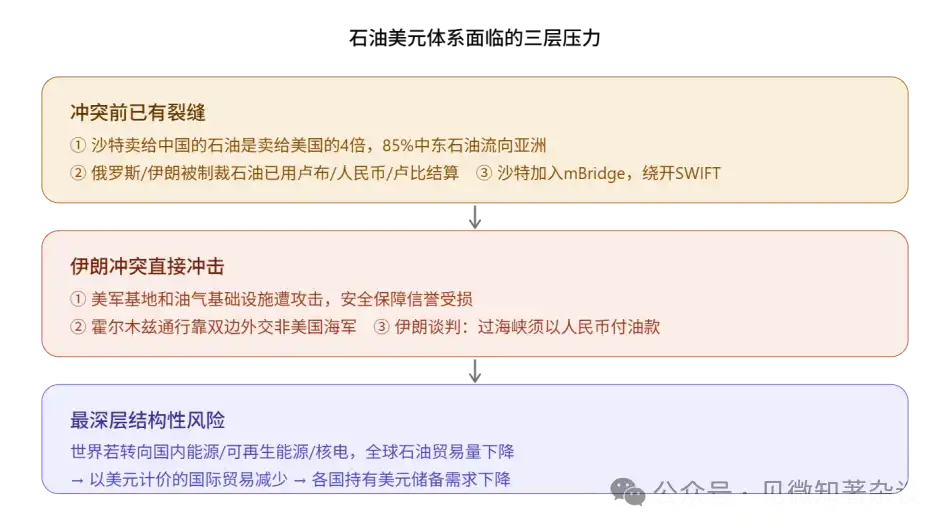

Chapter IV: The Three Layers of Pressure on the Petrodollar System

4.1 Layer One: Pre-Conflict Structural Cracks

The process of shaking the petrodollar system began long before the Iran conflict erupted. The following four structural changes are necessary background for understanding the current crisis:

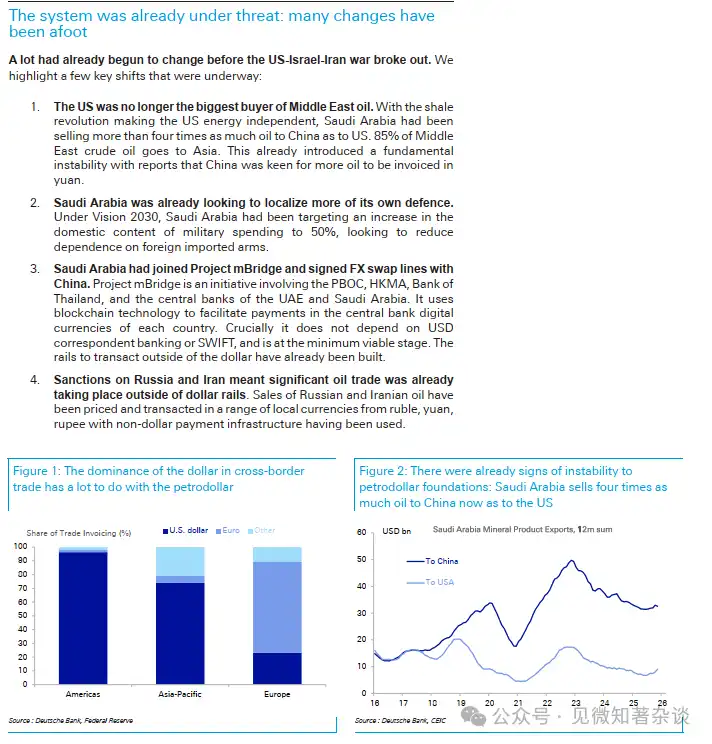

- Crack One: The U.S. is No Longer the Major Buyer of Middle Eastern Oil

The U.S. shale revolution (starting in 2008, fully爆发 in the 2010s) completely changed the global oil trade landscape. The U.S. achieved energy self-sufficiency, drastically reducing its dependence on Middle Eastern oil. Currently, Saudi Arabia exports four times more oil to China than to the U.S.; 85% of Middle Eastern crude flows to Asia.

There is a profound geopolitical logic矛盾 here: The U.S. uses taxpayers' money to provide security guarantees, but the primary beneficiaries of the oil flow are no longer the U.S. This矛盾 is increasingly difficult to explain to voters at the U.S. domestic political level, creating long-term structural pressure on the U.S.-Saudi alliance.

- Crack Two: Saudi Arabia Promotes Defense Autonomization

Under the Vision 2030 framework, Saudi Arabia set a goal to increase the localization rate of military procurement to 50%, actively promoting the localization of the defense industry. This is not just an industrial policy but also a geopolitical signal: When a country no longer relies entirely on an ally for weapons supply, its flexibility to adjust its political stance increases significantly.

- Crack Three: Project mBridge — Infrastructure Bypassing the Dollar Track

Project mBridge is a cross-border payment system jointly developed by the People's Bank of China, the Hong Kong Monetary Authority, and the central banks of Thailand, the UAE, and Saudi Arabia. It is based on blockchain technology and uses central bank digital currencies (CBDCs) for settlement, bypassing the SWIFT and dollar correspondent banking systems.

The operating logic of the existing dollar payment system is: Cross-border funds usually need to pass through U.S. correspondent banks for中转, and fund flows must pass through U.S. ledgers. Therefore, the U.S. can monitor and sanction global fund flows. The strategic significance of mBridge lies in: It establishes a set of international settlement infrastructure that operates completely outside the U.S. field of vision. The report specifically points out that this system has reached the "Minimum Viable Stage"—meaning it is technically ready for practical use, no longer just a concept.

The infrastructure to bypass the sanctions weapon is already in place. This is one of the most noteworthy structural changes in this crisis.

- Crack Four: Sanctions Give Rise to Alternative Systems

U.S. sanctions against Russia and Iran have objectively served as a "de-dollarization laboratory." Sanctioned countries are forced to develop alternative payment solutions. Russia-Iran, Russia-China, and Russia-India have already formed a large number of trade practices settled in local currencies. These experiences and infrastructure will remain and扩散 for use by more participants. The "weaponization" of sanctions has a significant backlash effect—the more frequent the sanctions, the stronger the global perception of the vulnerability of dollar dependence, and the greater the motivation for de-dollarization.

4.2 Layer Two: Three Direct Shocks from the Iran Conflict

Shock One: Damage to U.S. Security Guarantee Credibility

Attacks on U.S. military bases in the Gulf region and strikes on oil and gas infrastructure have symbolic significance far exceeding their actual losses. The core premise of the 1974 agreement was that the U.S. could provide effective security guarantees. Now this premise is being publicly and repeatedly questioned. For GCC countries, this triggers a calculation: If security guarantees are no longer reliable, is it still worth paying the implicit fee of "dollar pricing"?

Shock Two: Political Restructuring of Strait of Hormuz Passage Rights

Some oil tankers passing through the Strait of Hormuz are granted passage through bilateral diplomacy rather than U.S. naval power—ships bound for China, India, and Japan have received passage permits. This means that control over the world's most important energy通道 is shifting from "U.S. military power" to "Iran's political will."

The Strait of Hormuz passes about 20 million barrels of oil per day, accounting for 20% of global seaborne oil trade. This is not abstract geopolitics but a practical issue directly affecting whether factories in Japan, South Korea, and Europe can operate.

Shock Three: Coercive Guidance of Petro-Yuan

The most explosive reports come from multiple media outlets: Iran is negotiating with some countries, offering the option to pay for oil in Chinese yuan in exchange for passage through the Strait of Hormuz. If this arrangement is implemented, its significance lies in the fact that passage rights themselves become a bargaining chip for oil pricing currency—this is a new type of directly linking geopolitical control with monetary policy, which can be understood as a coercive induced version of "petro-yuan."

Once this mechanism proves feasible, its demonstration effect will be profound. The oil trade route from the Middle East to Asia may gradually form an independent yuan-pricing region, operating in parallel with the dollar-pricing region in the Western Hemisphere—this is the core content of the report's "worst-case scenario."

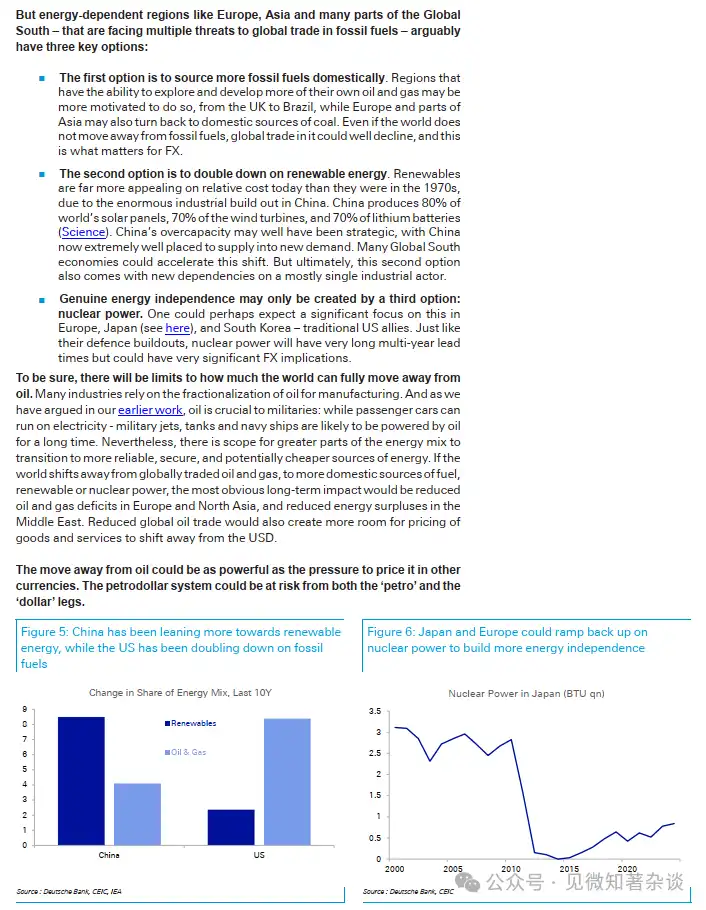

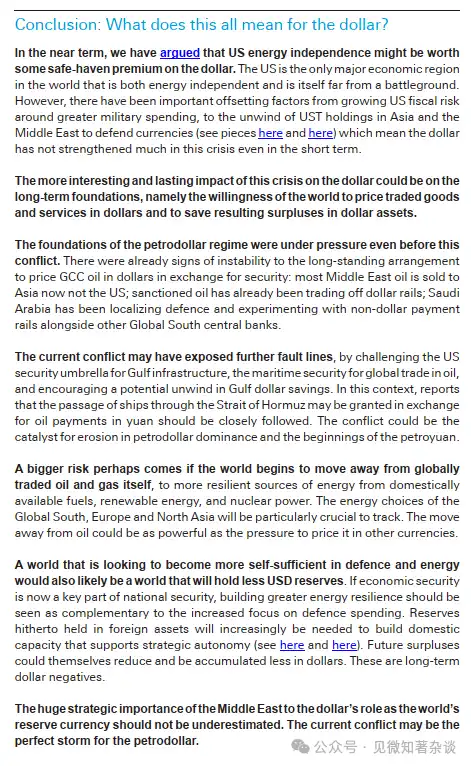

4.3 Layer Three: Energy Transition—A More Fundamental Threat to the Dollar

A risk deeper than oil-for-currency is the decline in the total volume of global oil trade. There is a key distinction here: What matters is not how much oil the world consumes, but how much oil is traded cross-border.

If Europe reduces oil imports through nuclear power and renewables, the export surpluses of the Middle East will contract, the amount of trade that needs to be settled in dollars will decrease, and global demand for dollars will decline—even if oil prices are high, the petrodollar mechanism will weaken.

Three Transition Paths for Energy-Dependent Economies:

Core Warning: The petrodollar system is facing pressure on both legs simultaneously—"oil" faces pressure from de-dollarized pricing, and the "dollar" faces pressure from declining demand caused by shrinking oil trade volume.

Chapter V: The Failure of Old Logic in the Current Conflict

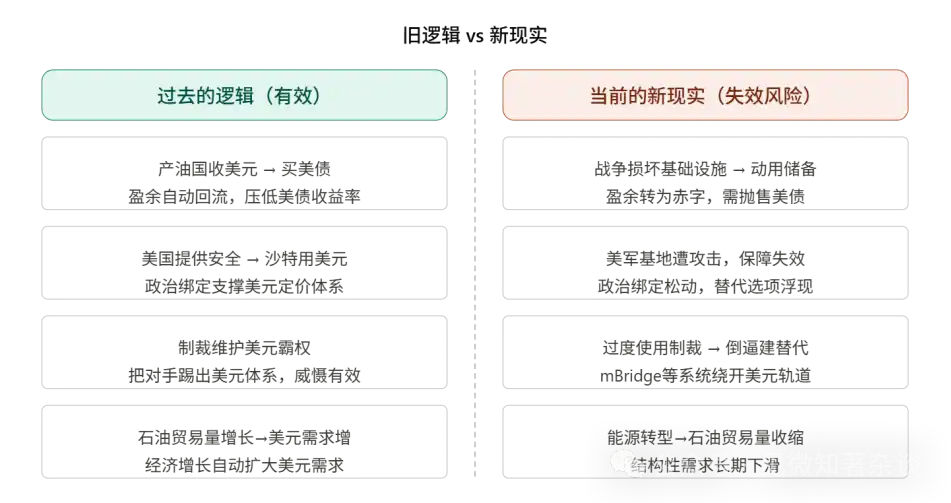

5.1 Surplus Reversal: From Largest Buyer to Potential Seller

Historically, oil price shocks were usually accompanied by an expansion of dollar surpluses in GCC countries, leading to greater demand for U.S. Treasuries. But the current conflict breaks this pattern: The war simultaneously damages the oil and gas infrastructure and production capacity of oil-producing countries. Gulf economies may transform from surplus entities into deficit entities that need to动用 reserves to repair their economies.

Scale Reference: The MENA region holds about $2 trillion in central bank managed reserves and about $6 trillion in sovereign wealth funds. These assets are primarily allocated to U.S. Treasuries. If large-scale redemptions are used for domestic reconstruction, the direction is恰恰 opposite to the historical petrodollar recycling—becoming net sellers of U.S. Treasuries.

5.2 Structural Pressure on the Supply Side of U.S. Treasuries

To understand the current U.S. Treasury market, one must overlay reduced demand with expanded supply:

- Demand Side: GCC reserves may shift from net buying to net selling; China's holdings of U.S. Treasuries have fallen from a peak of about $1.3 trillion to about $770 billion; Japan is continuously selling U.S. Treasuries to intervene in the forex market due to yen depreciation pressure.

- Supply Side: The U.S. fiscal deficit continues to widen, wartime military spending further increases expenditures, the outstanding U.S. debt exceeds $35 trillion, and annual net issuance hits record highs.

This means the U.S. Treasury market is undergoing a historic structural shift: From "foreign central banks being stable marginal buyers" to "foreign central banks becoming net sellers," and domestic buyers (the Federal Reserve, pension funds, commercial banks) must fill this gap, requiring a higher yield premium.

5.3 Why the Dollar Hasn't Strengthened This Time

Historically, geopolitical crises are usually accompanied by a stronger dollar (safe-haven effect). But the dollar's performance in this conflict is much weaker than expected, due to the对冲 of multiple factors:

Positive: U.S. energy self-sufficiency provides some safe-haven premium; it is the only major economy that is both energy independent and远离 the battlefield.

Negative (One): Rising fiscal expansion risks;激增 military spending加重 concerns about the U.S. fiscal deficit.

Negative (Two): Asian and Middle Eastern countries sell U.S. Treasuries to defend their local currencies (reverse petrodollar recycling).

Negative (Three): The petrodollar cycle weakens; the automatic mechanism that historically supported the dollar is failing.

This combination of "internal troubles and external threats" explains why the dollar's performance in this conflict is far less strong than historical patterns would suggest.

Chapter VI: Buffer Factors and Scenario Analysis

6.1 Countervailing Forces That Cannot Be Ignored

Understanding these important buffer factors helps form a more complete judgment:

The U.S. Could Become the Largest Oil Supplier

The U.S.,凭借 the shale revolution, has achieved energy independence. If it further integrates Western Hemisphere resources (Canada, Central and South America), its reserves will exceed OPEC's. As the largest supplier, the U.S. will have the ability to dominate the pricing terms of oil trade—shifting from "protecting buyers" to "controlling supply," maintaining the dollar pricing system under a new framework.

GCC Countries are Deeply Tied to the Dollar

The currencies of Gulf countries are pegged to the dollar, backed by trillions of dollars in foreign exchange reserves and sovereign wealth funds. The value of these reserves is directly linked to the dollar exchange rate. Any de-dollarization action would trigger speculative attacks on their own currencies, creating a powerful self-restraint mechanism.

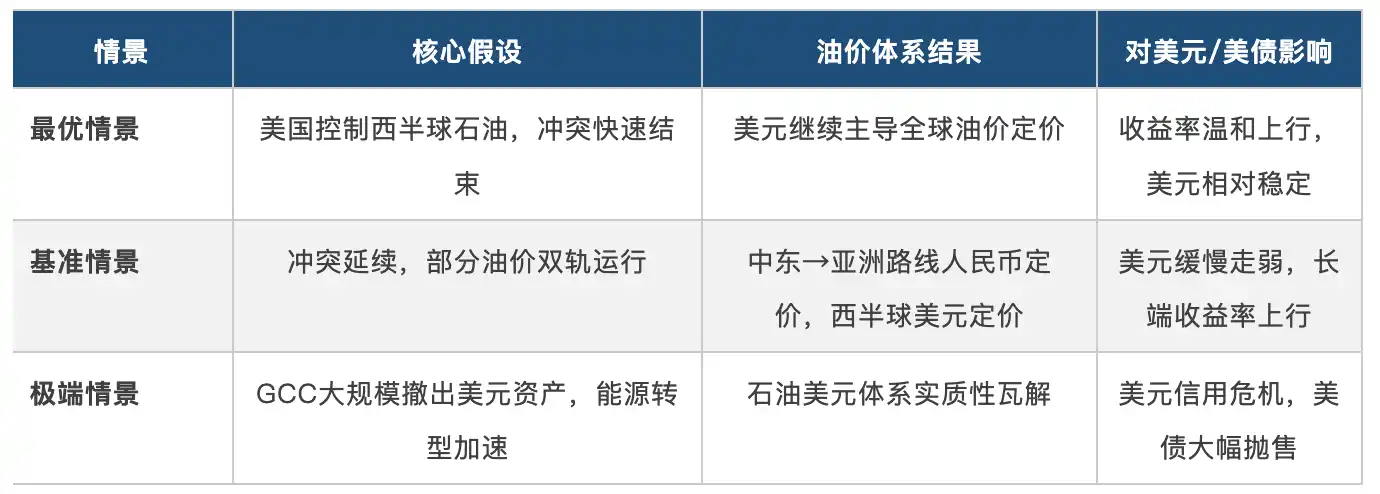

6.2 Scenario Analysis: Three Possible Futures

Chapter VII: Conclusion: The Long-Term Implications of Slow Variables

7.1 Distinction Between Short Term and Long Term

In the short term (1–3 years), U.S. energy independence provides some relative advantage. However, multiple adverse factors对冲 each other. The dollar may remain high but is unlikely to strengthen significantly. U.S. Treasury yields face upward risks due to fiscal deficits and inflationary pressures.

More noteworthy are the long-term structural changes (3–10+ years). The report identifies three long-term paths that suppress the dollar: Diversification of oil pricing currencies, decline in global oil trade volume (energy transition), and countries主动 reducing dollar reserves for strategic autonomy. These three paths are slow variables; they will not materialize急剧 in the short term, but once a trend forms, it will be difficult to reverse.

7.2 The Most Worth Tracking Signals

The following indicators are the most important observation windows for judging the direction of the petrodollar system:

Strait of Hormuz passage arrangements: Whether a fixed mechanism for yuan payment in exchange for passage rights is formed.

GCC sovereign wealth fund动向: Whether MENA region's U.S. Treasury holdings show a systematic decline.

Project mBridge usage scale: Whether actual transaction volume begins to scale.

Saudi oil settlement currency: Whether confirmed non-dollar oil contracts exist.

European/Japanese/South Korean nuclear power investment: Whether substantive de-fossil-fuel energy plans are formed.

7.3 The Final Core Judgment

The report's final core judgment is worth pondering: 【A world committed to defense and energy self-sufficiency will also be a world that holds fewer dollar reserves.】 This is not a prophecy about the collapse of the dollar, but a structural judgment about its slow retreat. When the optimal strategy for global countries shifts from "integrating into the dollar system" to "reducing vulnerability to the dollar," every node of the petrodollar cycle will weaken marginally. This is a slow variable measured in decades, but its direction has become clearer because of this conflict.