Author: Long Yue

Recently, memory prices, which had been rising for several months, suddenly reversed course, sparking market concerns that the memory cycle has peaked.

According to market tracking data, DDR5 memory from multiple US retailers has seen widespread price cuts, with single-kit reductions reaching up to $100. Taking Corsair's VENGEANCE series as an example, its 32GB capacity, 6400MHz maximum frequency model is currently priced at approximately $379.99, a significant drop from the recent peak of $490, representing a single-kit reduction of over $110.

The domestic market in China is also facing impact. A wholesaler told the "China Business Journal" that the price of mainstream 16G memory modules "dropped over one hundred RMB in a single day," and major players who had stockpiled goods earlier are now frantically selling off their inventory.

"Starting last Saturday, the prices just crashed," said Boss Wang, a wholesaler with years of experience in the storage equipment business at Bainaohui, candidly telling the media. He showed an extreme price curve for a mainstream 16G 3200MHz memory module: it was only a little over 130 RMB in May last year, then skyrocketed to a peak of 980 RMB in December. However, after fluctuating at high levels for months, the current spot price has fallen back to around 700 RMB.

Boss Wang expressed helplessness, stating that because the price increase had overdrawn consumer expectations, "those who aren't in urgent need won't buy. Compared to before November last year, our sales have dropped by more than 60%."

At the same time, Google published a paper on a new compression algorithm named "TurboQuant." The research indicates that this technology can reduce the Key-Value cache (KV Cache) memory usage during large language model runtime by at least 60%. Investors quickly priced this in as: the AI hardware shortage issue will be fundamentally alleviated, and memory demand will be significantly reduced.

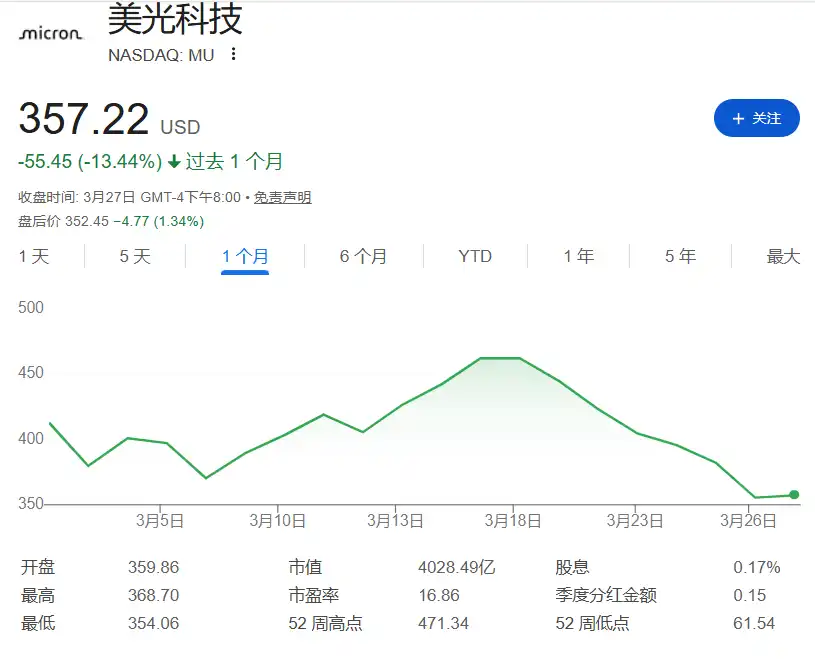

The chill from the spot market quickly spread to the capital markets. Micron Technology's stock price has retreated over 24% from its recent high, and Western Digital has also fallen nearly 21% from its high of $777.60. Simultaneously, the US memory chip sector lost nearly $100 billion in market value last week.

Faced with the price plunge and stock crash, market participants are severely divided on the prospects of the memory industry. Some investors believe the traditional memory "hog cycle" has peaked, while HSBC's institutional research believes the market is overly worried, and the current situation is the mid-point of an AI-driven memory super cycle, with strong demand for high-end products like HBM, and the memory shortage may persist for one to two years.

The Buyer Says 'No': A Repeat of the Traditional "Hog Cycle"?

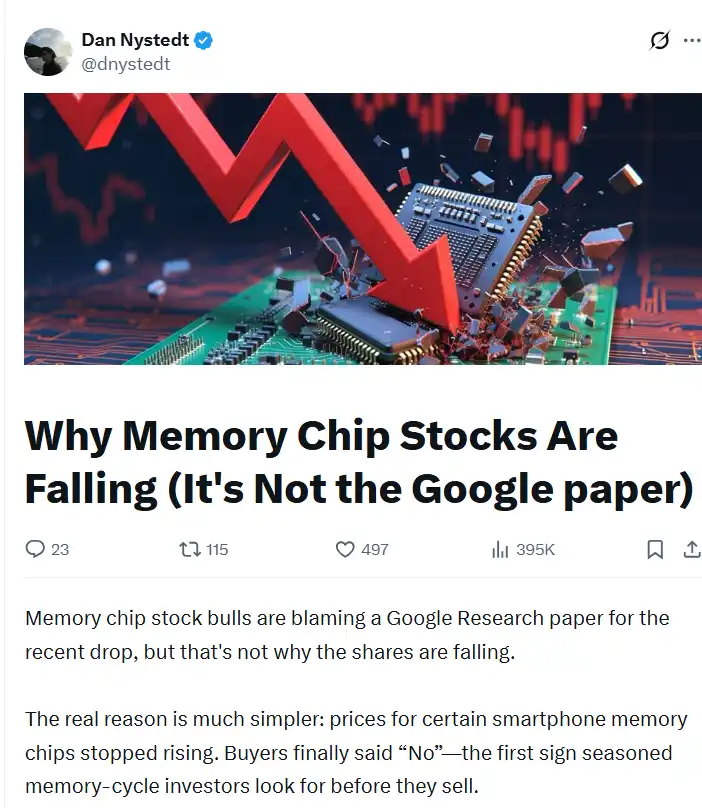

For traders following the traditional cycle, the market crash is not that simple. Former journalist and renowned Taiwan-based semiconductor analyst Dan Nystedt pointed out that many bulls blame the recent plunge on the Google paper, but this is just the surface. Dan believes the real reason is that prices for some smartphone memory chips have stopped rising.

"The real reason is much simpler: prices for some smartphone memory chips stopped rising. Buyers finally said 'no'—this is the first peak signal experienced memory cycle investors look for before selling," said Dan Nystedt. Due to excessively high DRAM and NAND prices, some smartphone manufacturers plan to reduce or even cancel the production of low to mid-range phones in 2026. He revealed that buyers rejected higher DDR4 prices two weeks ago.

Dan Nystedt compared the memory industry to the "hog cycle" in agriculture: high prices prompt companies to expand production, but building factories takes time, and when new capacity is released simultaneously, prices plummet. He believes investors following this script have quickly withdrawn, leading to significant corrections in the stock prices of Micron and SanDisk (Note: likely refers to Western Digital which acquired SanDisk).

Over the past 50 years, memory chips have experienced over a dozen major boom/bust cycles. Since 2010 alone, there have been three: the 2012-2015 3G/4G and cloud computing explosion; the 2016-2019 5G and cloud service provider expansion; and the 2020-2023 pandemic-driven PC/server surge. The cycle starting in 2024 is an upcycle driven by AI servers (HBM and SRAM).

"Whenever someone writes 'this time is different,' that is usually a classic sign of bullish sentiment running wild," Nystedt quoted legendary trader Jesse Livermore: "The market is always right, and opinions are often wrong." He reminded investors that when chip buyers stop panic buying, and when rallies repeatedly face sustained selling, seasoned money will quickly retreat according to the script.

Structural Change: Are Memory Companies No Longer "Cyclical Stocks"?

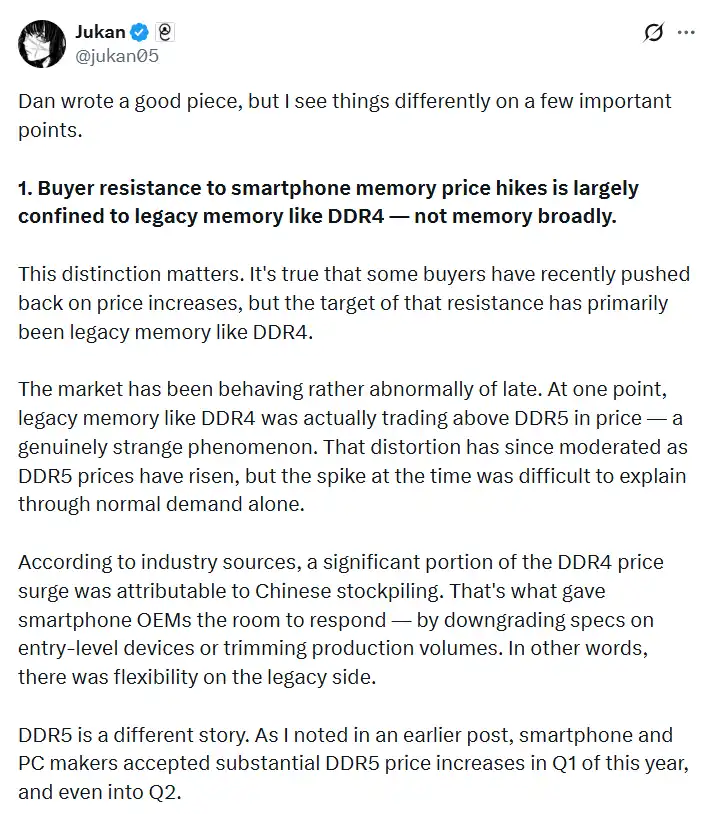

However, independent analyst Jukan offered a different perspective on Dan Nystedt's analysis.

He pointed out that buyer resistance to price increases is mainly concentrated on traditional memory like DDR4, not the entire memory market. The abnormal spike in DDR4 prices was partly attributed to stockpiling in the Chinese market, which gave smartphone manufacturers room to adjust the specifications of low-end devices.

"But DDR5 is a completely different story," Jukan noted. Smartphone and PC manufacturers dutifully accepted the significant price increases for DDR5 in Q1 and even Q2 of this year. In the current AI and high-end device ecosystem, DDR5 is not a negotiable item but a core input that buyers must secure even by paying a premium. Flagship products built around DDR5 simply cannot have their specifications reduced.

Secondly, the market has completely ignored the fundamental transformation in the business models of memory giants. Jukan expressed disdain for so-called "sophisticated investors" who blindly sell based on spot price declines.

"Memory companies are no longer operating in the old mode of blind capacity expansion," Jukan敏锐地 (sharply) pointed out. The three giants—Samsung, SK Hynix, and Micron—are moving closer to TSMC's business model: namely, building capacity only after securing advance payments and long-term demand visibility from core customers.

Recently, Korean media reported that Samsung is discussing prepayment-based cooperation agreements with giants like Microsoft. Memory giants understand the pain of capacity过剩 (excess) destroying cycles better than anyone. Therefore, they are now pursuing extremely restrained capacity expansion, not reflexive overbuilding.

Investment Banks Bullish: Memory Super Cycle Only at Midpoint, Market's Five Major Worries Overblown

In contrast to the panic in the spot market, investment banks remain confident in the long-term prospects of the memory industry. HSBC stated clearly in a research report released on March 30, "In our view, the current concerns are overblown; we are at the midpoint of an AI-driven super cycle."

The report listed five specific current market worries as overreactions:

1) Negative impact of rising raw material and electricity prices due to Middle East conflicts;

2) Slowing memory price growth in the second half of 2026;

3) Industry technologies like Google's "TurboQuant" and NVIDIA's "KVTC" that reduce memory usage in AI systems;

4) Gradually increasing capital expenditure plans by major memory manufacturers;

5) Intensifying competition from Chinese memory manufacturers.

The report pointed out that Middle East conflicts have no substantial impact on memory manufacturers' procurement of raw materials. The absolute growth in profits will have a far greater impact on stock prices than the slowing slope of DRAM price increases. Simultaneously, memory manufacturers remain highly清醒 (clear-headed) and restrained in their execution of capital expenditures.

Regarding the Google TurboQuant technology that triggered the market sell-off, the bank believes it is too early to worry. The commercialization of this technology will take about a year, and its reference parameter scale is smaller than the current AI environment. More importantly, the bank noted that TurboQuant alleviates the memory bandwidth bottleneck, will improve system efficiency, reduce token costs, and thus accelerate the commercialization and popularization of AI. The report wrote:

"The net impact is, we believe efficiency gains will accelerate AI development—a positive event that should trigger a sharp increase in AI adoption rates."

Meanwhile, the bank forecasts that AI server shipments will surge 28% year-on-year in 2026. From 2026 to 2027, the average DRAM content per server will achieve strong growth of 17%. With the explosion of AI inference demand, enterprise Solid State Drives (eSSD) are ushering in a golden age. The report expects the share of eSSD in total NAND demand to soar from 18% in 2023 to 40% by 2027. AI servers will consume 62% of that.

The bank believes the current market is at the midpoint of an AI-driven super cycle, comparable in scale to the six-year DRAM shortage triggered by office automation from 1990-1995. Looking back at history, from 1990 to 1995, alongside the popularization of Windows 3.0 and subsequent operating systems, office automation caused a structural DRAM shortage lasting six years, driving the DRAM market size to soar sixfold from $7 billion in 1990 to $41 billion in 1995.

The bank believes that the infrastructure construction催生 (spawned) by large models, agentic AI, and physical AI (like autonomous driving) will cause memory shortages to persist for at least one to two years.

Based on these assessments, the report is firmly optimistic about their certainty of benefiting from the memory super cycle. Regarding the recent暴跌 (plunge), the report wrote: "We believe any pullback provides an additional buying opportunity."