Original Author:Raoul Pal, CEO of Real Vision and GMI

Compiled by:CryptoLeo(@LeoAndCrypto)

This morning, Raoul Pal, CEO of Real Vision and GMI (Raoul Pal's investment bible), published an article titled "False Narratives....and Other Thoughts". Through data comparison and macro analysis, he explained the recent downturn and crisis in the crypto industry, indicating that the industry winter will soon pass, and everyone needs to be patient and not lose confidence in the industry. Odaily Planet Daily translates it as follows:

These were the insights I wrote for GMI over the weekend, hoping to bring you some confidence. I would have kept this content for GMI and Pro Macro discussions, but I know you all need this to ease your tense nerves.

Mainstream Narrative: Is Crypto Over?

The mainstream view is that Bitcoin and cryptocurrencies have crashed, this cycle is over, everything is finished, and it can't be like before. Cryptocurrencies have decoupled from other assets, this is CZ's fault, it's BlackRock's fault, etc. This is undoubtedly an attractive narrative trap, especially when mainstream coin prices are plummeting every day.

But yesterday, a GMI hedge fund client sent me a message asking if they should buy the dip in SaaS stocks, or, as everyone is saying, if Claude Code has already killed the SaaS industry.

So I started researching SaaS, and in the process, I found conclusions that debunk both the mainstream narrative about Bitcoin and the narrative about the SaaS industry. The charts for SaaS and BTC look exactly the same?

UBS SaaS Index vs. Bitcoin Trend

Indicating there is another factor that everyone is ignoring affecting this trend.

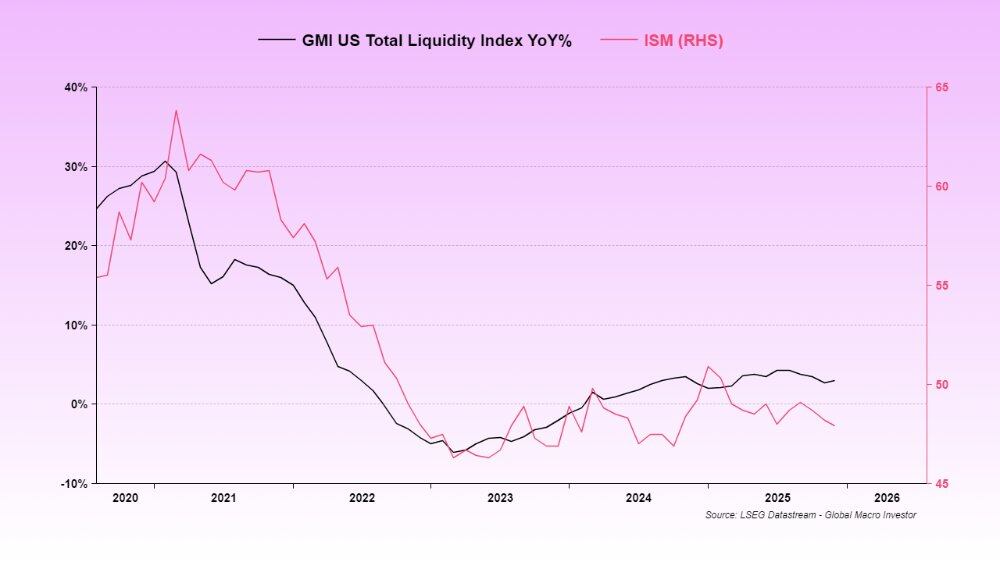

This factor is: Due to two shutdowns and issues with the US financial system's infrastructure (the reverse repo mechanism's liquidity was only fully replenished in 2024), US liquidity has been constrained. Therefore, the TGA (Treasury General Account) rebuilding in July and August had no corresponding monetary offset measures, leading to a reduction in liquidity.

So far, the low liquidity is the reason the ISM Manufacturing Index has remained low.

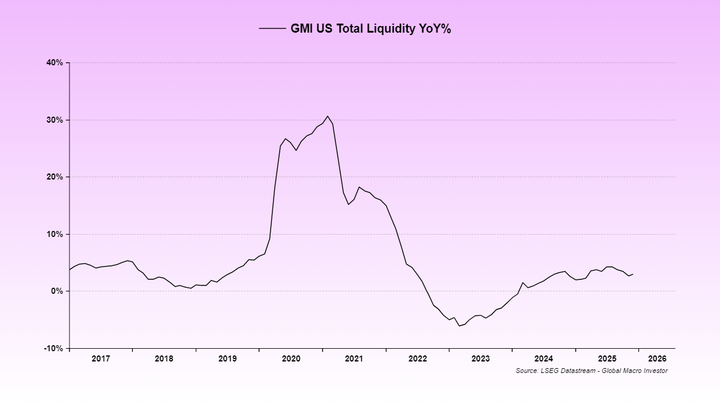

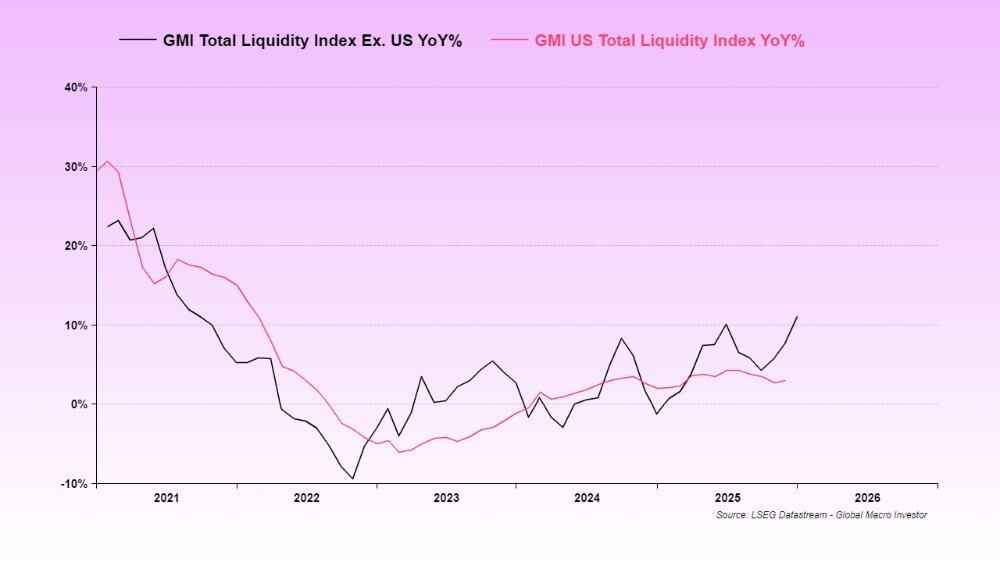

We usually use the Global Total Liquidity indicator because it has the highest long-term correlation with BTC and the Nasdaq, but at this stage, US Total Liquidity seems more important because the US is the main provider of global liquidity.

In this cycle, the GMI Global Total Liquidity Index leads the US Total Liquidity Index and is about to rebound (thus also driving the ISM index).

This is exactly what is affecting SaaS and BTC. Both assets are among the longest-duration assets in existence and have fallen due to the temporary withdrawal of liquidity.

Gold's rise has essentially sucked out the marginal liquidity from the system that might have flowed into the Bitcoin and SaaS markets. There isn't enough liquidity to support these assets, so high-risk assets are getting hit and falling. There's really no way around it.

Now, the US government is happening again, and the Treasury Department has taken preventive measures: after the last government shutdown, no TGA funds were used, and instead, the asset scale was increased (i.e., further loss of liquidity). This is the crisis we are facing now. It has caused violent price fluctuations, and our beloved cryptocurrency still lacks liquidity.

However,种种迹象表明,this government shutdown will be resolved this week, which will clear the last liquidity obstacle.

Odaily Note: US House Speaker Johnson said in an interview on NBC News' "Meet the Press" on Sunday that he believes he has secured Republican support votes to ensure the shutdown of some government agencies ends by Tuesday.

I have mentioned the risks of this government shutdown many times before, but it will soon be over, and then we can continue to deal with the upcoming liquidity injection, which includes measures from eSLR, partial TGA回流 (TGA回流 likely means TGA runoff or drawdown, context suggests funds returning to system), fiscal stimulus, interest rate cuts, etc., all related to the mid-term elections.

Odaily Note: US regulators' bill to relax leverage ratio requirements to ease capital pressure on several major banks like Bank of America (BAC.US).

In a full trading cycle, time is often more important than price. Price can be hit hard, but as time passes and the cycle evolves, everything will be resolved and eventually settle.

This is why I have always emphasized "patience". Events need to develop. Focusing solely on profit and loss ratios will only affect your mental health, not your investment portfolio.

The Fed's False Narrative

Regarding interest rate cuts, another false narrative is that Kevin Warsh is a hawk. This is complete nonsense; these statements are mainly from over 18 years ago.

Warsh's job and mission were to execute the strategies of the Greenspan era. Both Trump and Besant have said (details not discussed here, but the main direction is rate cuts) to keep the economy hot and assume that the productivity gains from AI will suppress core CPI increases (just like the 1995-2000 era).

Odaily Note: Greenspan is one of the longest-serving chairs in Fed history. His advocated monetary policy (controlling inflation + promoting maximum employment) was highly flexible but practically more anti-inflation prioritized, while also actively injecting liquidity during crises.

He doesn't like the balance sheet, but the system is reserve-constrained, so he likely won't change its current practices, otherwise it would destroy the credit market.

Warsh will cut rates and do nothing else. He will not interfere with Trump and Besant's actions to manage liquidity through banks. Fed Governor Milan will likely forcefully push for a full eSLR cut to accelerate this process.

If you don't believe me, believe Druck ↓

The above shows "investment guru" Stanley Druckenmiller's content on Warsh's monetary policy philosophy and his agreement with Besant upon becoming Fed Chair.

I know how difficult it is to hear optimistic narratives when the crypto market looks so dark. My SUI holdings are terrible, we don't know what or who to believe anymore. First, we have been through this many times before. When BTC falls 30%, altcoins can fall even 70%. But if they are high-quality alts, their rebound is also faster.

Mea Culpa (My Mistake)

GMI's mistake was not considering US liquidity as the current driving factor; usually, Global Total Liquidity dominates the entire cycle. But now the situation is clear, anything is possible.

The two are not unrelated. We just couldn't predict the combination punch of a series of events (reverse repo draining liquidity > TGA rebuilding > government shutdown > gold rising > another shutdown), or we failed to anticipate its impact.

It's almost over, and soon we can get back to normal work.

We cannot guarantee that every link is error-free (now with a deeper understanding), and we are still very bullish on the 2026 outlook because we understand the Trump/Besant/Warsh strategy. These three have repeatedly told us: we just need to listen and be patient. In full-cycle investing, time is more important than price.

If you are not a cycle investor and don't have such strong risk tolerance, that's completely fine. Everyone has their own style, but Julien (GMI Head of Macro Research) and I are not good at swing trading (we don't care about intra-cycle fluctuations), but we are proven and have a verifiable track record in full-cycle investing, leading the industry for the past 21 years. (Warning: We also make mistakes, like in 2009). Now is not the time to give up. Good luck, and let's achieve greater results in 2026.

Liquidity relief is on the way!