If you've been in the industry for more than one cycle, you've undoubtedly witnessed this recurring scene:

During extreme market conditions, prices flash crash, oracles deliver distorted prices, liquidation bots swarm in, and a batch of positions gets liquidated in a chain reaction within minutes. The selling pressure continues to cascade downward, eventually evolving into a liquidity run on the entire ecosystem. Starting from the "312" event in 2020, through subsequent crashes like "519" and "1011", forced liquidations have consistently been the most criticized trigger.

Facing this dilemma, Vitalik Buterin published a research concept earlier this month titled Building index-tracking assets on top of options instead of debt, posing a rather disruptive question: Can DeFi replace the traditional CDP (Collateralized Debt Position) and forced liquidation model with an option-based mechanism?

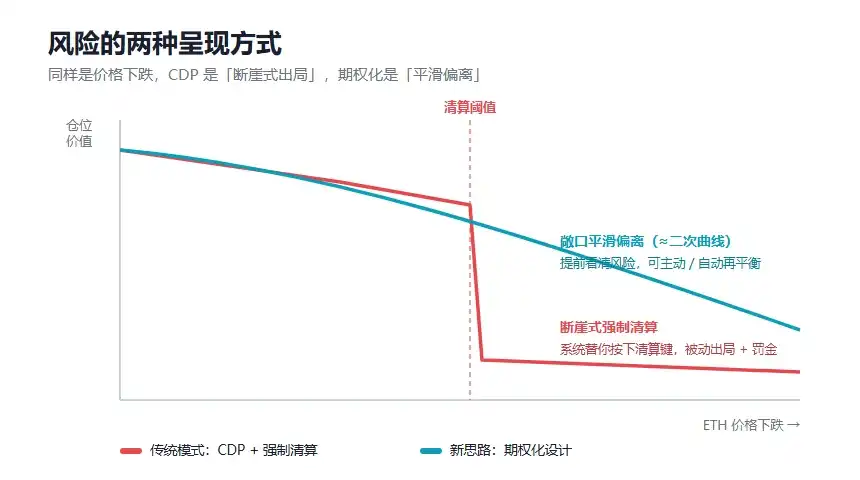

According to Vitalik's conception, the core advantage of this design is the potential use of "slow oracles" to replace real-time oracles, thereby significantly reducing the risk of oracle manipulation. A user's exposure to the index would deviate from the target in a smooth (approximately quadratic) manner, rather than experiencing instantaneous forced liquidation.

I. The Achilles' Heel of Traditional DeFi

Before discussing Vitalik's new line of thinking, it's necessary to revisit why "CDP + forced liquidation" became the core model of DeFi, and why it also became its weakness.

As is well known, represented by classic lending protocols like MakerDAO/Sky, Aave, and Compound, one of the most important early financial innovations in DeFi was allowing users to collateralize on-chain assets to borrow another asset.

This mechanism can be simply understood as users depositing assets like ETH into a protocol, obtaining a borrowing limit. As long as the collateral value remains sufficiently high, the position is safe; however, once the collateral price falls below a certain threshold, the protocol triggers a liquidation, selling the collateral to repay the debt and protect the system's solvency.

It may seem mundane today, but this mechanism was crucial for early DeFi. It transformed assets like ETH from "passively held" into "reusable" financial base assets for the first time, enabling them to enter more complex systems like lending, leverage, stablecoins, and yield strategies.

It can be said that CDPs and lending protocols laid the earliest and most critical foundation for DeFi's composability.

However, its problems are also evident:

- Forced liquidation relies on real-time and highly reliable oracles: Protocols must rely on external oracles for second-by-second price feeds. If an oracle experiences delays, manipulation, extreme network congestion, or if certain assets themselves have insufficient liquidity, the protocol may execute liquidations based on temporarily distorted prices.

- Forced liquidation amplifies pressure during extreme market conditions: When collateral prices fall rapidly, liquidators and MEV bots compete intensely for liquidation opportunities. The concentrated selling of collateral further exacerbates market pressure, potentially triggering a liquidity run across the entire ecosystem.

- Illusion of liquidity: Traditional lending protocols assume "the market will always have sufficient liquidity to absorb liquidation selling pressure." However, in truly extreme market environments, liquidity can evaporate instantly. This leads to a situation where the price falls further, fewer people are willing to take on the risk, making liquidations harder to complete smoothly. If a protocol cannot promptly handle bad positions, it may be left with bad debt.

So, objectively speaking, CDP + forced liquidation is not a flawed design. It was an extremely important and effective foundational module in early DeFi. However, as DeFi has entered a stage of larger capital scale and more complex structures, the costs of this model have become increasingly prominent:

It concentrates risk highly on a single liquidation threshold—before the threshold is triggered, everything seems normal; once it's touched, users often have no choice but to passively endure the outcome.

II. Vitalik's New Approach: Reconstructing Lending with an 'Options Mindset'

Vitalik's new approach essentially seeks to change the underlying way DeFi handles risk.

We can summarize his thinking in one sentence: Could DeFi stop using "debt" as its foundational component and instead use "options" as its foundational component?

Because the foundation of the traditional CDP model is debt. Users borrow assets, and there must be a mechanism to ensure the debt is always sufficiently collateralized. Once collateral becomes insufficient, the protocol can only resort to forced liquidation to prevent system bad debt.

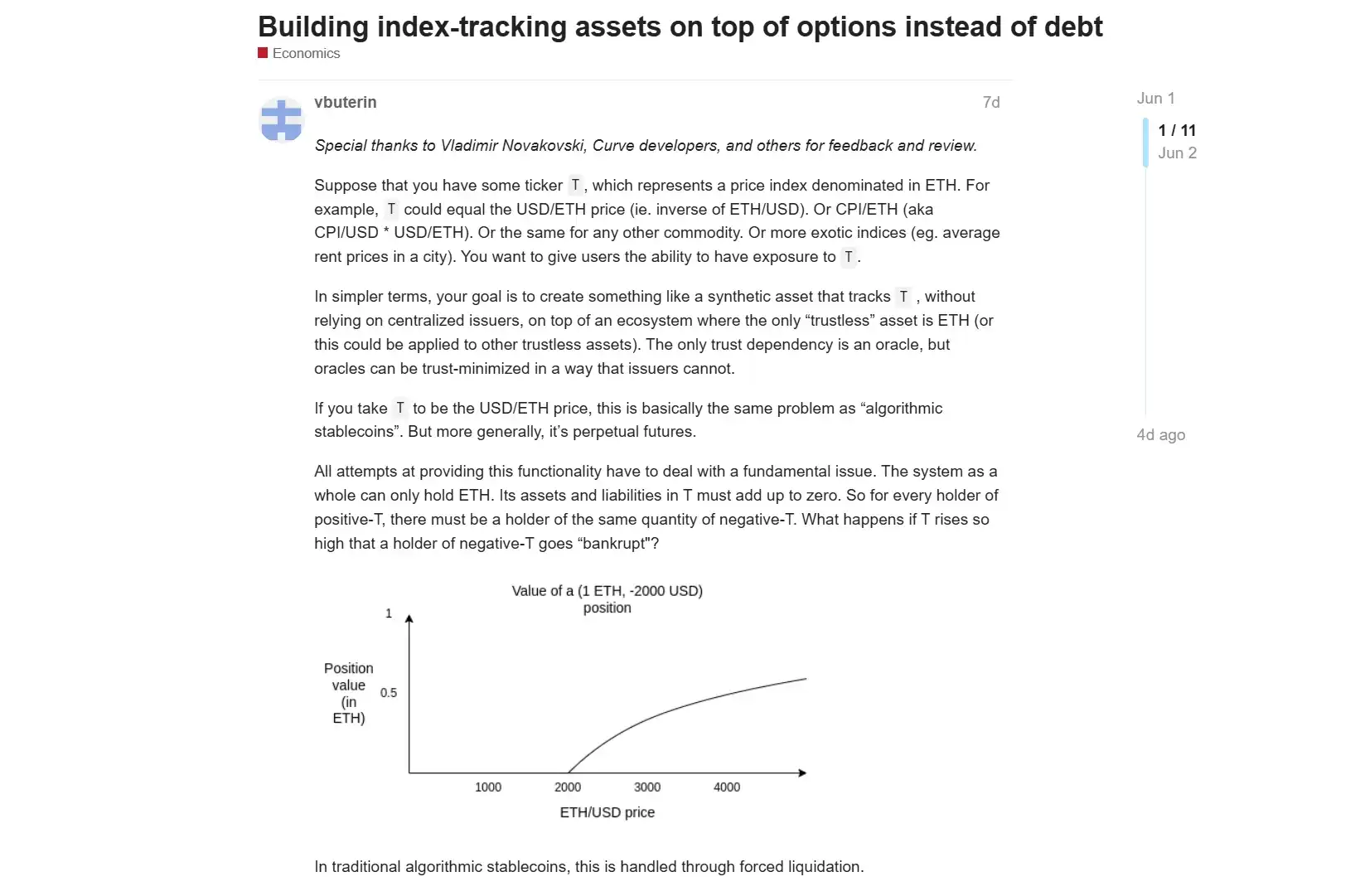

The design based on options takes a completely different approach. It doesn't have users create a debt that must be protected in real-time. Instead, it breaks down the underlying asset into a set of complementary contracts. Simply put, 1 ETH can be split into two types of assets: one closer to a stable or index-tracking exposure, and the other bearing the opposite risk and return. Regardless of price movements, the combined returns of these two assets always correspond to the underlying 1 ETH.

This means the system no longer needs to suddenly force-liquidate a user at a specific price point. In the traditional liquidation model, a user might be abruptly liquidated when the price hits the line. In the option-based model, users face a gradual deviation of their exposure from the target, requiring rebalancing at an appropriate time. Here's a more accessible analogy to understand this:

- The traditional model (CDP) is like you pledging $10,000 worth of ETH to a lending protocol, borrowing $5,000. The protocol monitors the price via an oracle; once ETH falls to a critical point, it directly sells your ETH without a second thought, charging you a hefty fee. You have no right to appeal.

- In the new option-based model, you pledge ETH and still receive $5,000, but this isn't called a loan. Its form is more like a time-bound "right": before the agreed-upon time, no matter how much ETH falls, your position won't be liquidated mid-way—the initiative always remains in your hands. At expiration, if the price recovers, you can redeem your collateral; if the price falls, you can simply choose not to exercise the option, letting the protocol take the collateral. You've already secured the $5,000 in hand, rather than being "cleaned out" by a wick in your sleep.

Of course, this is a simplified analogy to aid understanding. Vitalik's original design is closer to a combination of "holding deep in-the-money options and gradually rolling them to lower strike prices as the price approaches."

Overall, the former is more like "the system presses the liquidation button for the user," while the latter is more like "the user sees the risk curve in advance and decides when to adjust the position themselves." This shift in mechanism will undoubtedly bring profound changes to DeFi on several levels:

- No more 'hard liquidation': Since borrowing positions are transformed into options with a time cycle, the protocol no longer needs to set a "liquidation line that explodes immediately upon touch." Users no longer need to anxiously watch the charts daily and won't be force-liquidated in their sleep due to a single malicious wick.

- Significantly reduced reliance on oracles: The new mechanism drastically reduces dependence on high-frequency, real-time oracle price feeds. The protocol only needs to settle at expiration or specific time nodes. This directly reduces the space for hackers to launch attacks using "flash loans + oracle manipulation."

- Inherently anti-MEV properties: Without instantaneous forced liquidation, on-chain gas wars triggered by "cascading liquidations" will no longer occur. MEV bots lose their most lucrative liquidation arbitrage scenario. Value created by the protocol is more likely to flow back to users and LPs, rather than being extracted by arbitrageurs and sequencers.

The significance of this change goes far beyond "more safety."

Because the future users DeFi aims to serve include not just high-risk traders, but also more ordinary users and real payment scenarios. For these groups, what truly matters often isn't pushing capital efficiency to the extreme, but rather whether they retain choice during extreme market conditions and can avoid being forcibly kicked out of the system by a short-term fluctuation.

III. Do Users Still Need Ethereum DeFi?

This question has become more pertinent today.

With the rise of emerging ecosystems like Hyperliquid, users are seeing another form of DeFi product. They can offer faster matching experiences, interactions closer to centralized exchanges, more concentrated liquidity, and more direct fulfillment of trading needs.

This represents real competitive pressure for Ethereum.

If we only compare transaction speed, fees, and front-end experience, Ethereum mainnet and some traditional DeFi protocols may not always hold the advantage. Users won't automatically believe a protocol is better just because it's deployed on Ethereum, nor will they ignore cheaper and more convenient alternatives just because a product is more "orthodox."

Therefore, Ethereum DeFi needs to re-answer the question: Why do users still need Ethereum DeFi?

The answer certainly can't just be "because Ethereum is the most secure" or "because Ethereum has the largest TVL." The truly compelling answer should stem from more fundamental financial design capabilities.

In the author's opinion, if Ethereum DeFi is to remain the core arena of on-chain finance, it cannot merely stay at replicating traditional financial products to simply increase leverage efficiency. It must build advantages in more challenging areas, such as more transparent risk boundaries, more robust oracle mechanisms, fewer forced system actions, stronger user autonomy, and protocol structures that can better withstand extreme scenario testing.

In other words, the competitive focus for the next generation of Ethereum DeFi might no longer be about who can make users earn more, but about who can help users avoid being passively forced out in complex financial environments and truly understand the risks they are taking.

For ordinary users, the option-based DeFi design proposed by Vitalik might still seem distant and may not quickly mature into products. However, the direction it signals is clear: DeFi shouldn't only pursue higher yields; it should also pursue clearer, more explainable, and more manageable risk structures.

In Conclusion

To be realistic, after frequent security incidents, a common voice asks: Since DeFi has so many risks, does it mean on-chain finance itself is not viable?

This judgment might be overly simplistic.

The problem with DeFi doesn't lie in the direction of "decentralization" itself, but in the fact that many products haven't truly completed the evolution from high-risk experiments to robust financial infrastructure. The industry has been too accustomed to proving value with growth and TVL, while relatively underestimating risk design and resilience in extreme scenarios.

The new approach proposed by Vitalik precisely serves as a reminder to the industry: The evolution of DeFi isn't just about porting old finance onto the chain. It's about leveraging the programmable and composable characteristics of the chain to design new risk structures that traditional finance might not easily achieve.

If we only compete on speed and speculative efficiency, Ethereum can hardly win. Ethereum must return to its foundational narrative: security, decentralization, and bottom-up innovation in financial paradigms.

This, perhaps, is the real opportunity for Ethereum DeFi.