This report is authored by Tiger Research. The cryptocurrency industry is entering the mainstream. Institutions have become key players in the market. Capital is flowing to projects that generate real yield. Short-term price fluctuations are no longer important. Sustainable business models have become crucial. Tiger Research predicts ten major shifts in the cryptocurrency market by 2026.

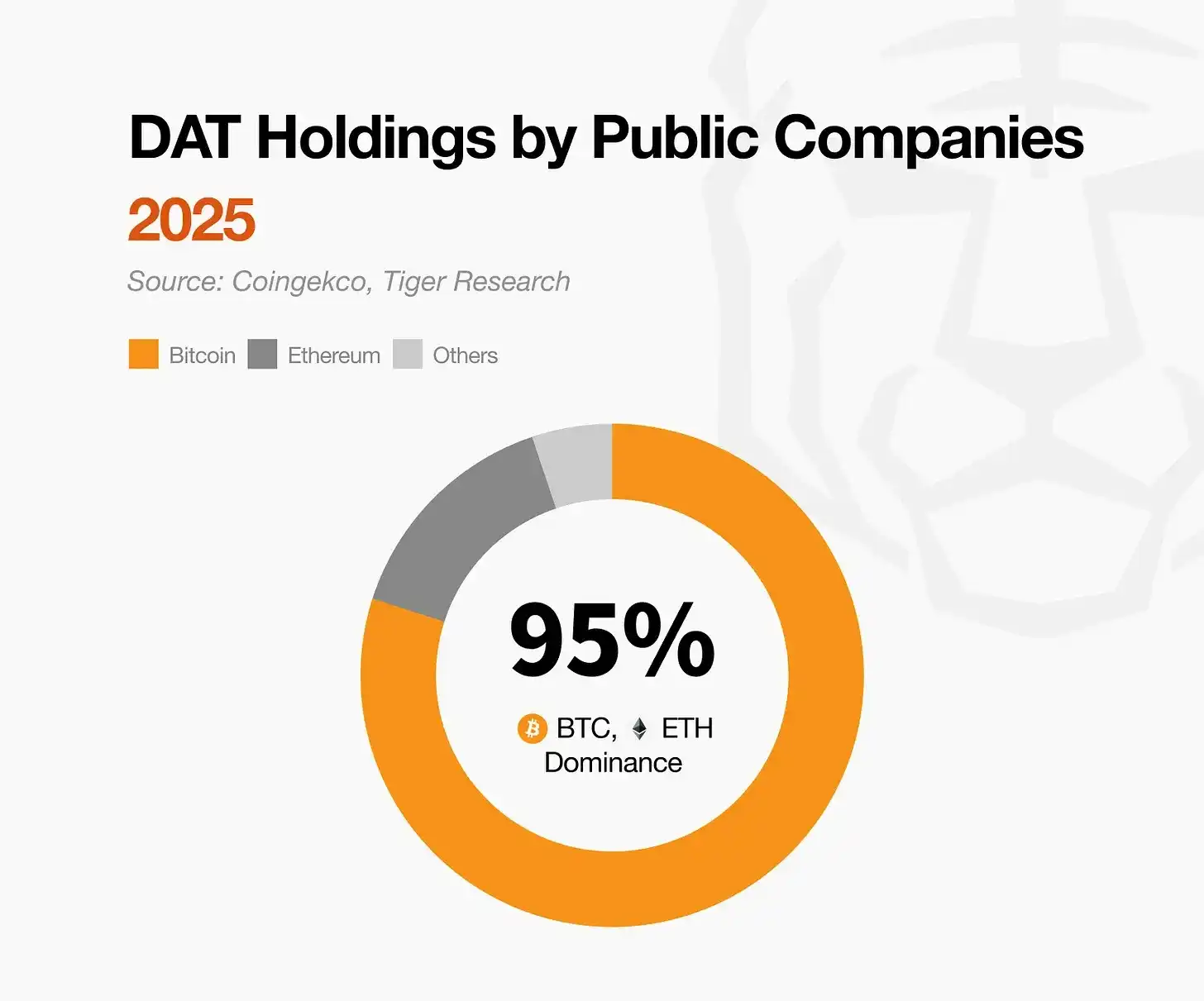

1. Institutional Capital Continues to Stay in Bitcoin

Source: Tiger Research

As institutions dominate the market, capital flows have become more cautious. These investors avoid unverified assets, limiting their scope to Bitcoin and Ethereum. This trend is likely to continue. Market growth will be concentrated only on assets that meet institutional standards.

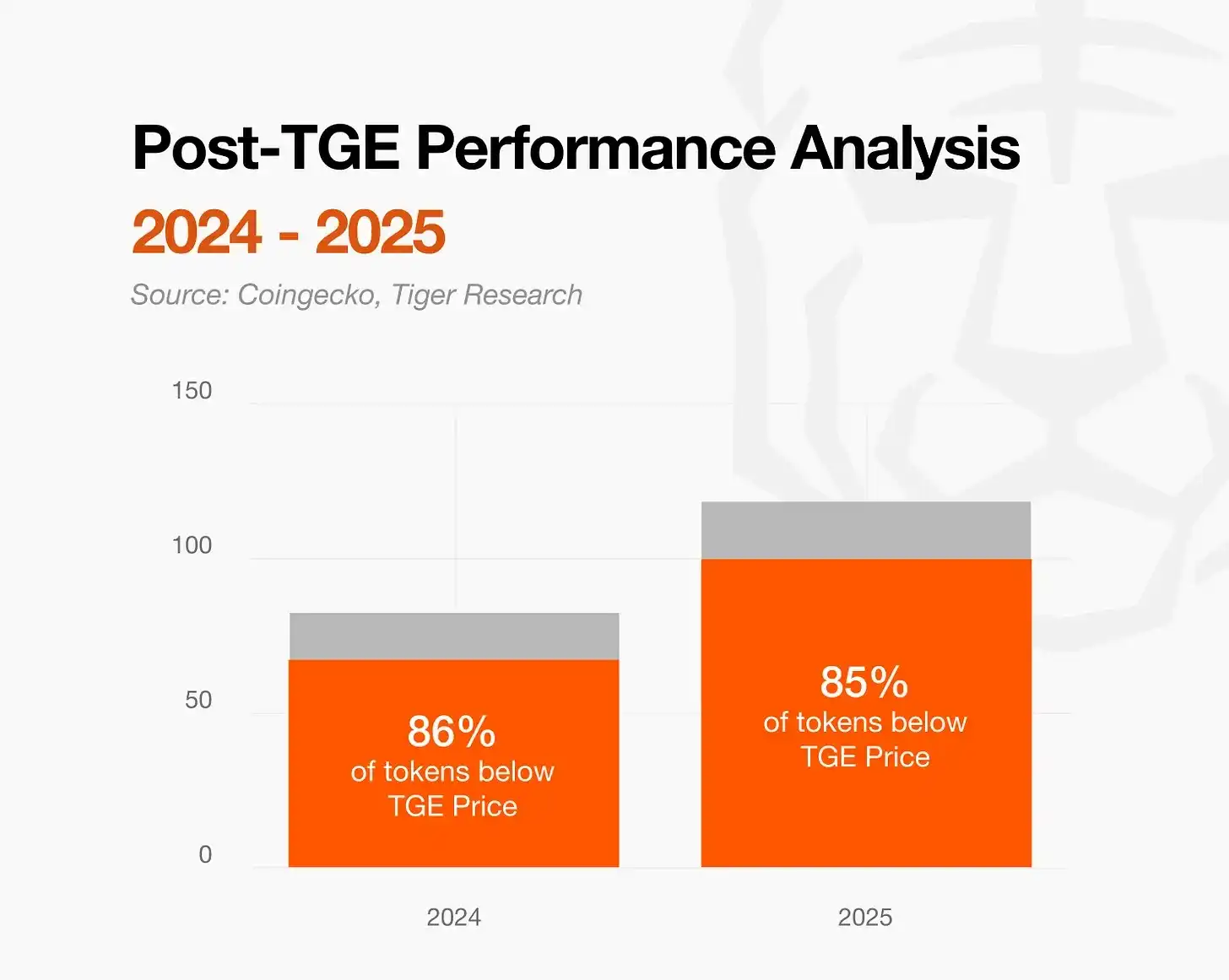

2. Profitless Projects Face Market Elimination

Source: Tiger Research

85% of new tokens decline in price after TGE, exposing the limitations of narrative-driven growth. Hype-based projects will be replaced by new trends at an increasingly rapid pace. The market will shift towards projects that generate real yield and demonstrate robust fundamentals.

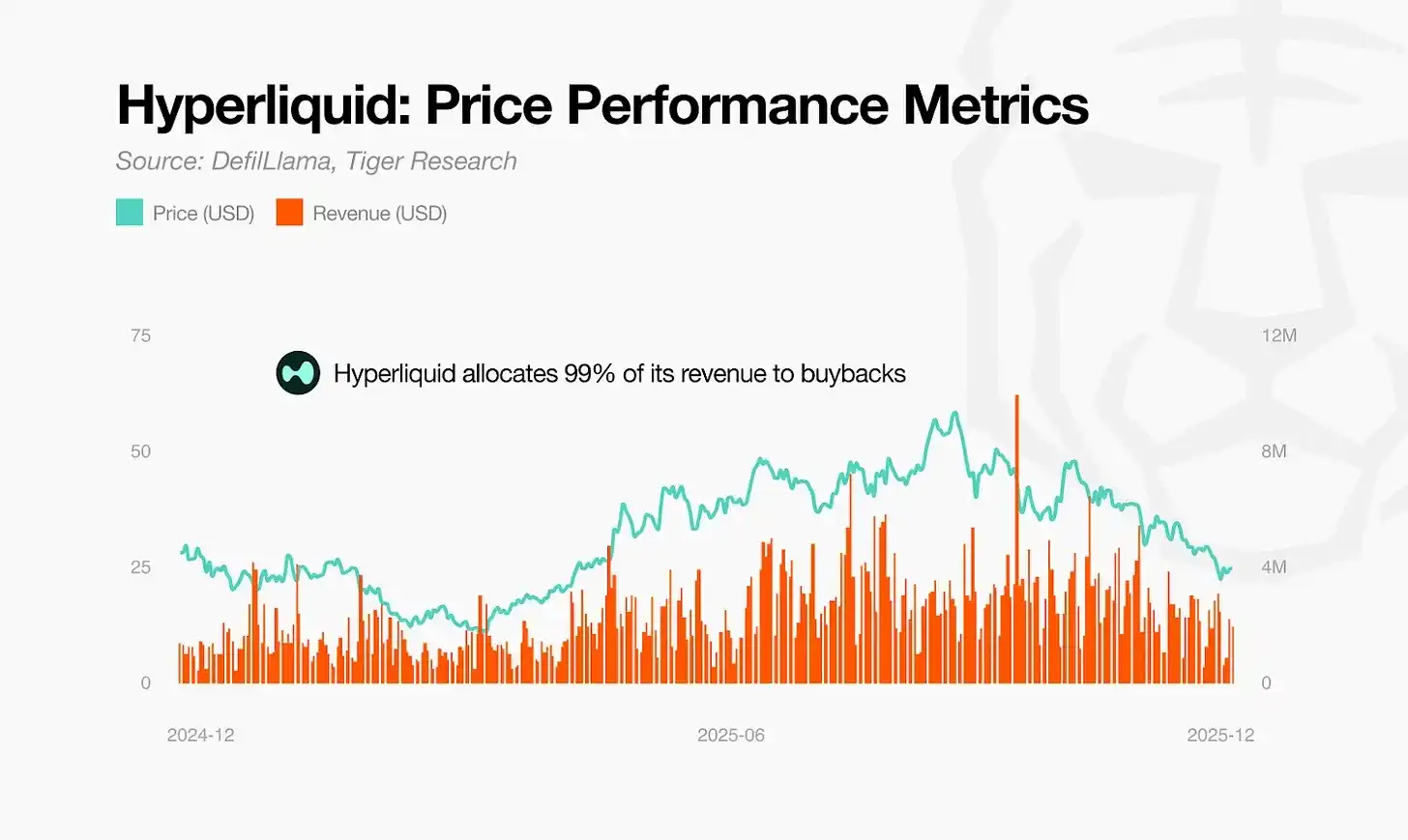

3. Utility Has Failed, Buybacks Are the Only Answer

Source: Tiger Research

Tokenomics focused on utility have failed. Governance voting rights have failed to attract investors. Complex structures are unsustainable. The market now demands clear value returns. Models that provide direct returns through buybacks and burns will survive. Structures where protocol growth directly impacts token price will also survive. New innovative models will emerge from this shift.

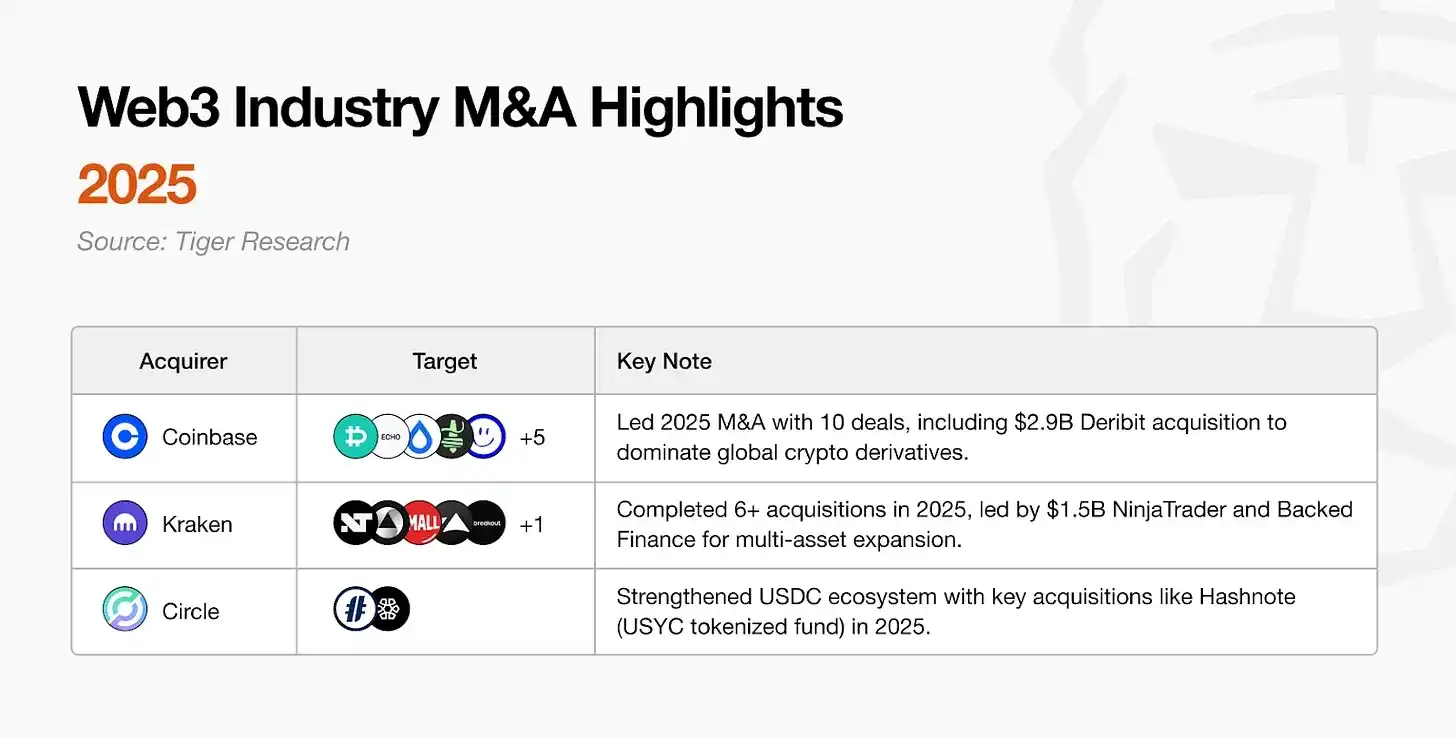

4. Increased M&A Opportunities Between Projects

Source: Tiger Research

Web3 is maturing. Competition for market dominance is intensifying. Mergers and acquisitions (M&A) are now the fastest way for companies to scale and enhance competitiveness. The winners will drive aggressive M&A activity. The market will be reshaped by businesspeople who create real profits.

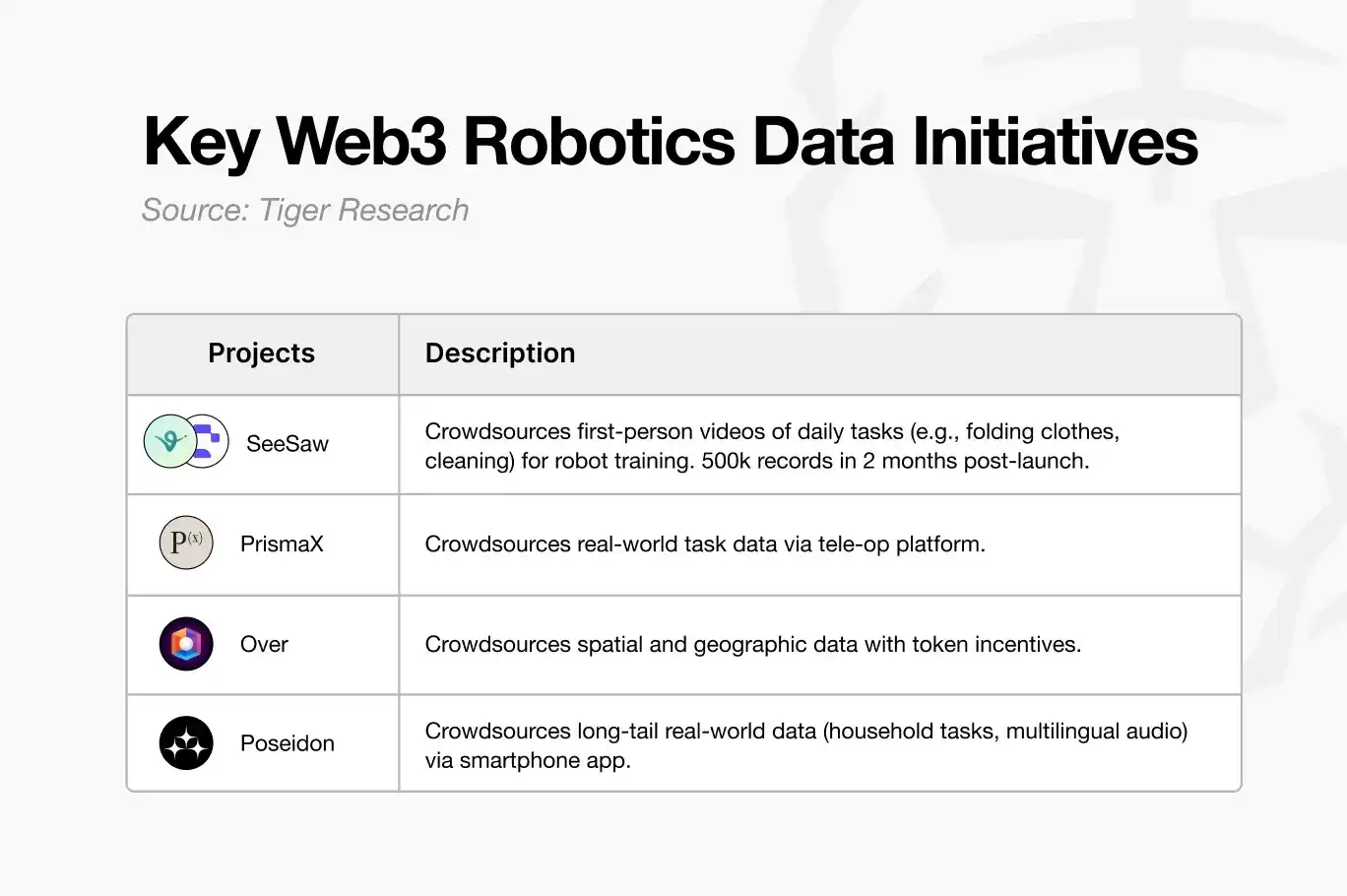

5. Robotics and Cryptocurrency Will Usher in a New Era of the Gig Economy

Source: figure.ai

The robotics industry is growing. Real-world data for robot training has become crucial. Traditional centralized methods cannot efficiently collect massive amounts of data. Blockchain-based decentralized crowdsourcing solves this problem. It collects vast amounts of data from individuals globally and provides transparent, instant rewards. A new gig economy centered around robotics will emerge.

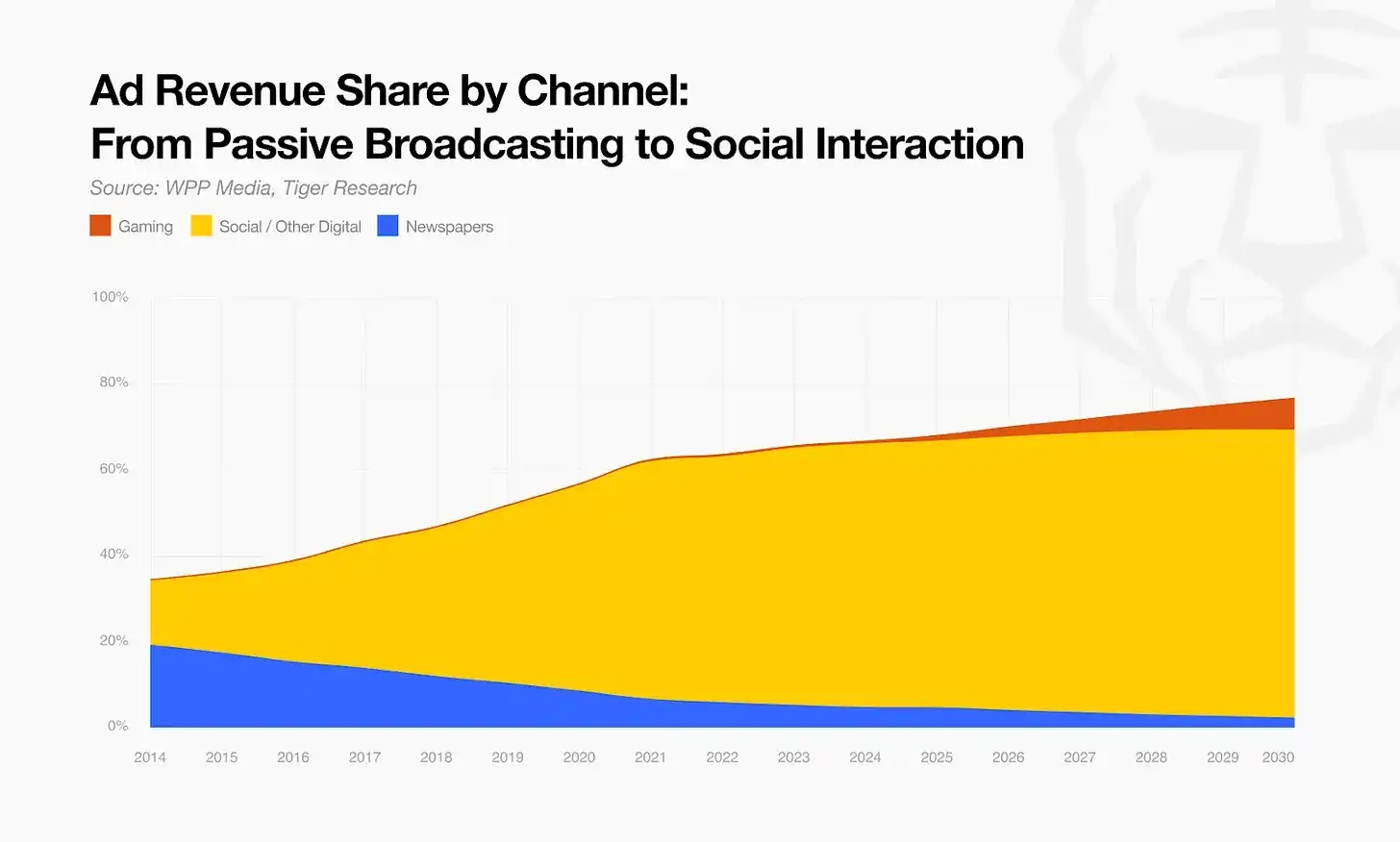

6. Media Companies Adopt Prediction Markets

As traditional revenue models reach their limits, media companies will adopt prediction markets as a survival strategy. Readers will shift from passive consumption to active participation, placing capital bets on news outcomes. This shift will optimize revenue structures while driving deeper audience engagement.

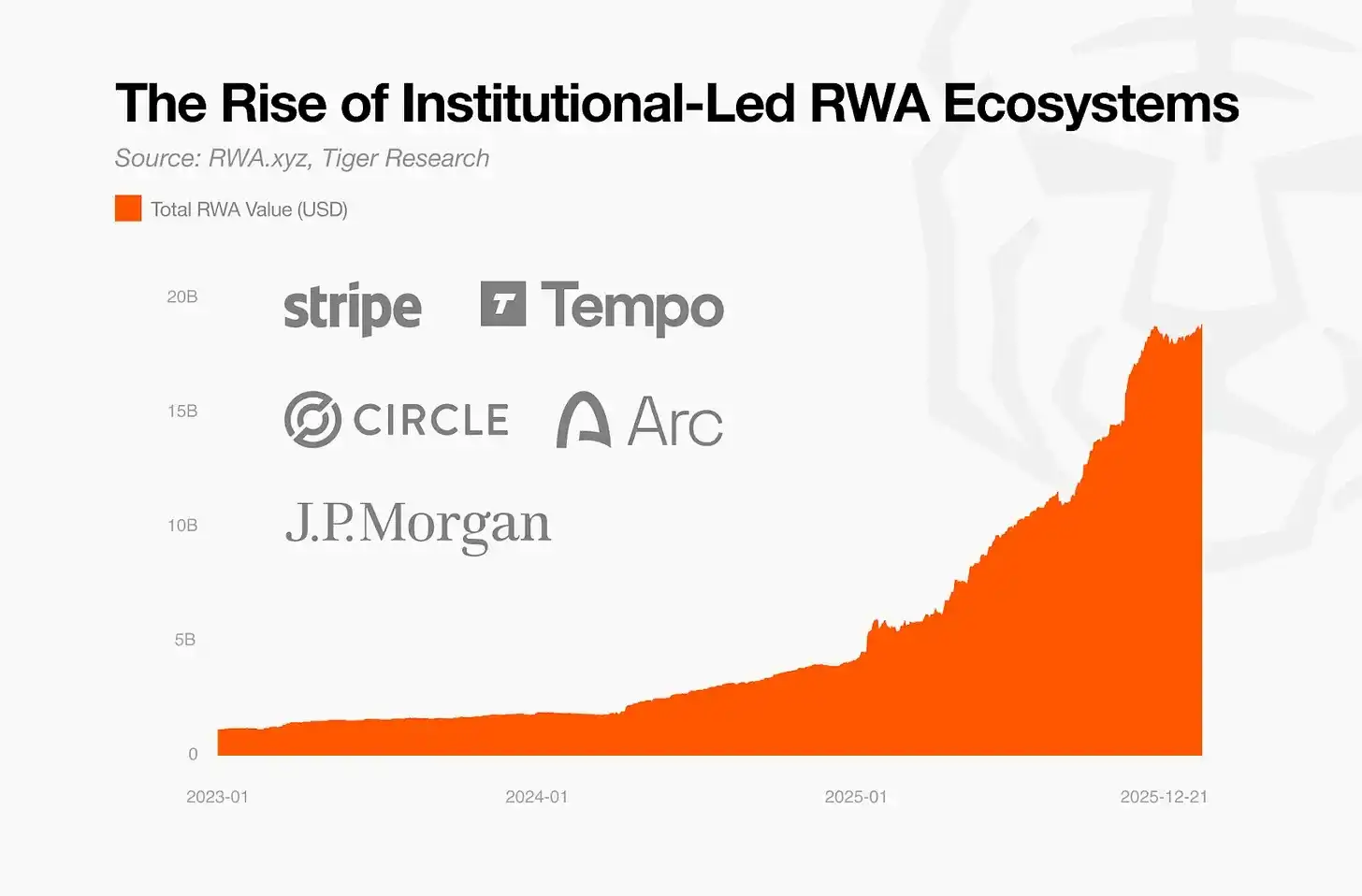

7. Traditional Finance Dominates RWA Through Self-Built Chains

Source: Tiger Research

Traditional financial institutions are the main suppliers in the RWA market. Given the need for asset control and security, the benefits of using third-party platforms are minimal. These companies are likely to build their own chains to maintain market leadership. RWA projects lacking independent asset supplies will lose their competitive advantage and face elimination.

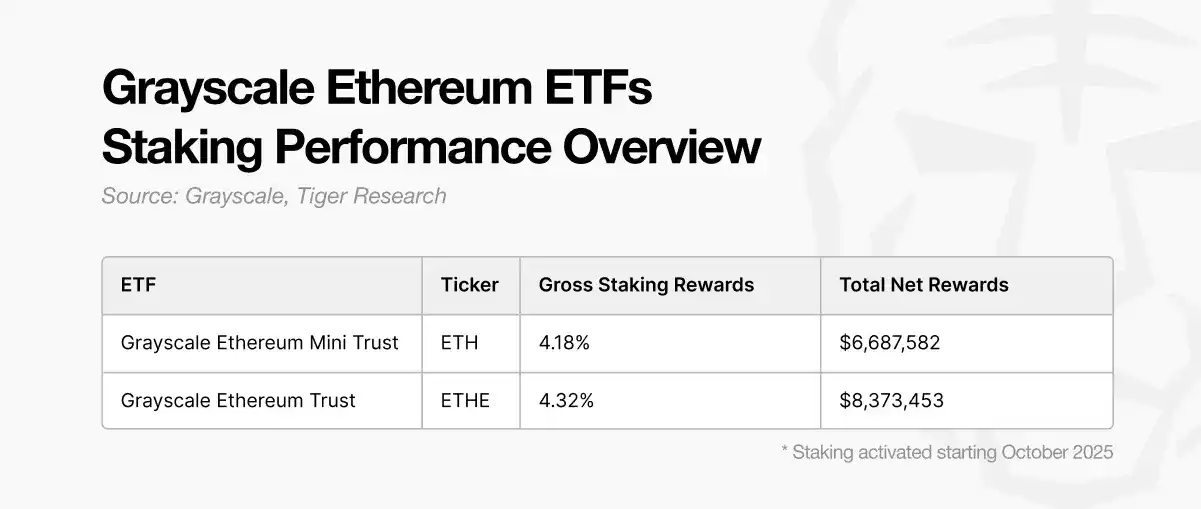

8. ETH Staking ETFs Will Drive BTCFi Growth

Source: Tiger Research

The launch of Ethereum staking ETFs will prompt Bitcoin ETF holders to seek yield. BTCFi fills this gap. As large amounts of capital enter Bitcoin, the demand for asset utility will rise. This pursuit of yield will drive the next wave of BTCFi growth.

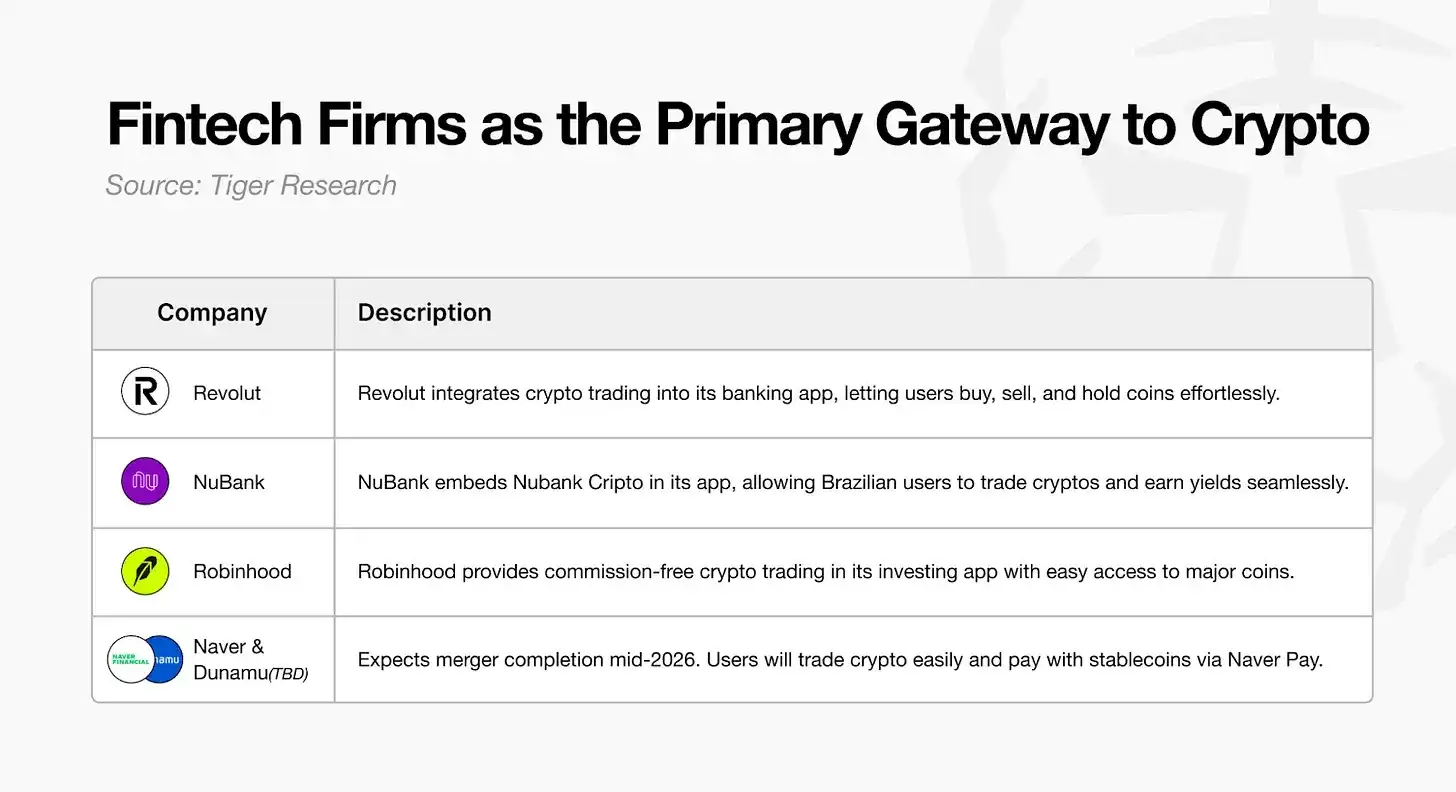

9. Fintech Will Surpass Exchanges as the Primary On-Ramp

Source: Tiger Research

As rules become clearer, fintech applications have become the preferred choice for cryptocurrency trading. New users no longer need to use cryptocurrency exchanges. They can buy and sell directly within the applications they use daily. The next wave of growth will be led by these fintech tools.

10. Privacy Technology Becomes Core Institutional Infrastructure

Source: Tiger Research

On-chain transparency exposes trading plans. This is a weakness for large institutions. High-net-worth participants must hide their movements to ensure security. Privacy technology is a key tool for these institutions to enter the market. Large-scale capital will only flow in if transaction data is secure.