Author: Dave

"The Advancing MM 1: Market Maker Inventory Quoting System"

"The Advancing MM 2: Market Maker Order Book and Order Flow"

The first two parts discussed order flow and inventory quoting, making it sound like market makers can only adjust passively. But do they have proactive methods? The answer is yes. Today, we introduce statistical edge and signal design, which are the "micro alpha" pursued by market makers.

1. Market Maker's Alpha?

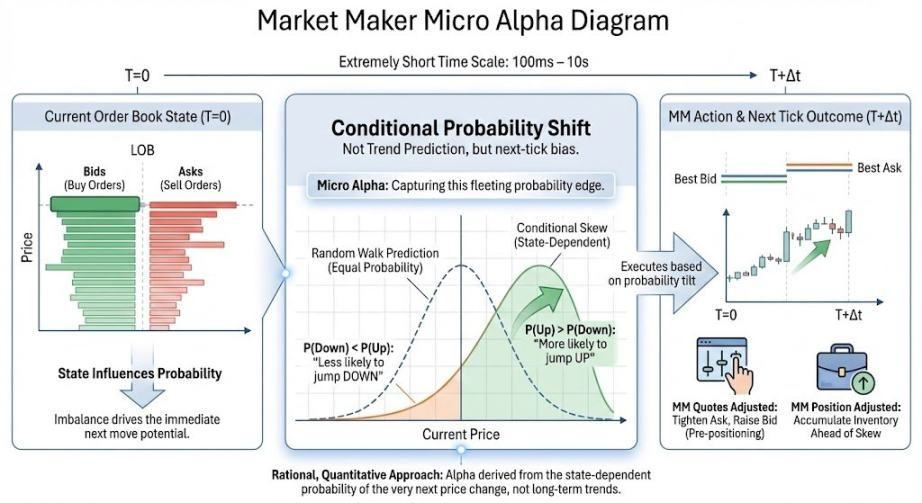

Micro alpha refers to the "conditional probability shift" in the direction of the next price movement / mid-price drift / trade asymmetry on an extremely short time scale (~100ms to ~10s). It's important to note that the alpha in the eyes of market makers is not about trend prediction or guessing price changes; it only requires a probability shift, which is different from the alpha we commonly talk about. Let me explain in simpler terms:

A market maker's statistical edge can be understood as whether, within an extremely short time window, the order book state is "inclined" to move the price in a certain direction first. If a market maker successfully calculates the probability of the next millisecond's price movement using some indicators, they can: 1. Be more willing to buy before a likely price increase. 2. Withdraw buy orders faster before a likely price drop. 3. Reduce exposure during risky moments.

The financial basis for predicting the next price direction is: Due to factors like order flow, order volume, and order book cancellation ratio (which we'll discuss later), the market is not a "random walk" Brownian motion in a short instant but has a direction. The above statement is the financial translation of the mathematical concept of "conditional probability."

With this alpha, market makers can directionally operate on prices. The "market makers" finally earn money from price movements, not just service fees like spreads.

2. Classic Signals Introduction

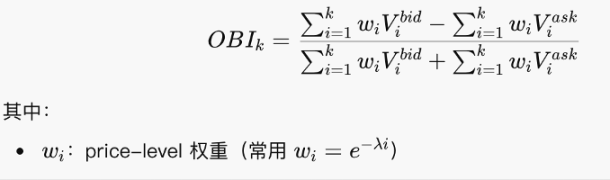

2.1 Order Book Imbalance: OBI

OBI measures which side has "more people standing" near the current price level. It is a standardized volume differential statistic.

The formula is actually not difficult; it's just a proportional logic of summation. It checks whether there are more buy or sell orders. An OBI approaching 1 indicates almost all are buy orders, with a thick bottom. Approaching -1 indicates a thick top. Approaching 0 suggests a relatively symmetric buy-sell balance.

Note that OBI is a "static snapshot." It's a classic indicator but not very effective alone; it must be used with cancellation ratios, order book slope, etc.

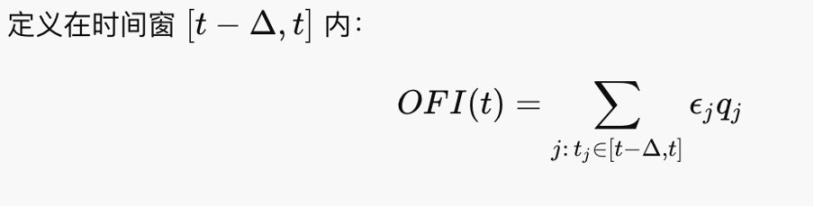

2.2 Order Flow Imbalance (OFI)

OFI measures who has been actively attacking in a recent short period. OFI is the first-order driving factor of price changes because prices are pushed by taker orders, not by placed orders.

It feels like net buying/selling volume. In the Kyle (1985) framework, ΔP ≈ λ ⋅ OFI, where λ is tick depth. Thus, OFI is the factor driving price changes.

2.3 Queue Dynamics (Queue)

Most exchanges now use continuous auction rules based on best price and first-come-first-served (FCFS) principles, so submitted orders queue up to be filled. The queue represents the order placement situation, which determines the order book state. Abnormal order book states (including order replenishment and cancellation)暗示 directional price changes, i.e., micro alpha.

Two situations to note in the queue:

1. Iceberg: Hidden Orders

Example: Only 10 lots are shown on the surface, but every time they are filled, another 10 lots are immediately replenished. The real intention might be 1,000 lots. The method I introduced in Part 1 for annoying market makers to lower costs is essentially manually creating an iceberg. In practice, some players use iceberg orders to conceal their true volume.

2. Spoof (Fake Orders)

Placing a large order on one side to create a "false pressure illusion" and canceling it quickly before the price approaches. Spoofing pollutes OBI, slope, etc., making the queue artificially thicker and increasing movement risk. Additionally, large spoofs can intimidate the market and potentially manipulate prices. For instance, the London Stock Exchange caught someone manipulating forex in 2015 using spoofing. In crypto, we can also manually spoof to annoy market makers, but if you actually get filled, your exposure becomes significant.

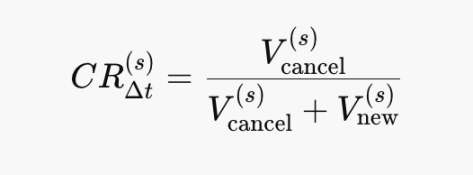

2.4 Order Book Cancellation Ratio (Cancel Ratio)

The cancellation ratio is an estimate of the "disappearance rate" of liquidity:

Cancel↑ ⇒ Slope↓ ⇒ λ↑ ⇒ ΔP more sensitive. It is an instability signal领先于 OFI. CR→1: Almost pure cancellations. CR→0: Almost pure order replenishment. The mathematical formulas in this part are very simple; you can interpret them by looking at the diagrams.

CR↑ ⟹ The passive side perceives future risk increasing. CR is also not used alone; it is used together with OFI and other indicators.

The above might just be some old-school order book games. The evolution of market making is rapid, and with stocks moving on-chain, market makers like JS might need to engage in on-chain market making. However, these indicators are still very useful and inspiring.

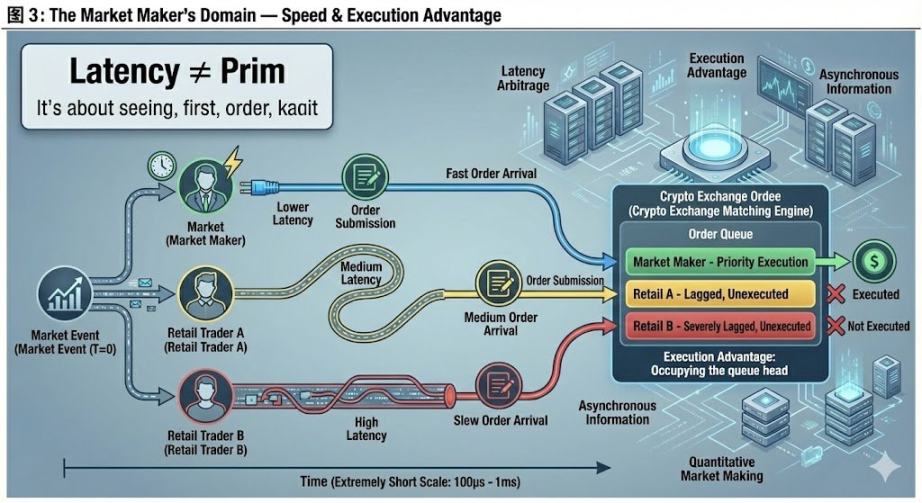

3. The Absolute Domain of Market Makers: Speed

We often hear in movies that a certain fund has faster internet speed, making it more powerful. Many market makers even move their server rooms closer to exchange servers. Why is that? Finally, let's talk about the advantages of physical equipment and the unique "trading advantages" of crypto exchanges.

Latency Arbitrage is not about predicting future prices but executing buy/sell orders at more favorable prices before others "react." In theoretical models: Prices are continuous, and information is synchronized. But in reality: The market is event-driven, and information arrives asynchronously. Why does information arrive asynchronously? Because receiving price signals from the exchange and sending order instructions to the exchange both take time—a limitation of the physical world. Even in fully compliant markets: Different exchanges, data sources, matching engines, and geographical locations cause delays. Thus, market makers with more advanced equipment have the initiative.

This tests the market maker's own capabilities and has little to do with other players, so I consider it their absolute domain.

A simple example: Suppose you want to sell a certain amount. You quote at the best selling price in the market, which should theoretically get filled. But I also want to sell. Since I see the price and quote faster than you, I get my order filled first. Your inventory cannot be sold, preventing your position from returning to neutral. Real situations are much more complex.

An interesting point: Since there are no regulatory laws yet, almost all crypto exchanges can directly grant priority filling rights to designated accounts. This means allowing certain accounts to jump the queue. This is especially common in smaller exchanges. It seems that being an "insider" in crypto is as important as in research. Whether you can execute trades safely is a crucial step from alpha theory to practice.

This part attempts to write from the perspective of a market maker. Actual operations are certainly more complex. For example, dynamic queue alone has many details to consider in practice. Welcome for comments from experts.

Postscript: There is a regret with this article. I originally wanted to use the title "Domain Expansion in Market Making" to discuss dynamic hedging and options, as I believe this is the conceptually most challenging part of market making, worthy of the big move "Domain Expansion." But after working on it for a day, I couldn't figure out how to explain it systematically, so I switched to discussing micro alpha. Teacher @agintender has an article mentioning many professional hedging concepts; I encourage everyone to take a look.