Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: The Semiconductor ETF (SOXX) has surged 78.5% year-to-date, while the Software ETF (IGV) has fallen 12.5% over the same period, creating a performance gap of over 90 percentage points, a historically extreme level.

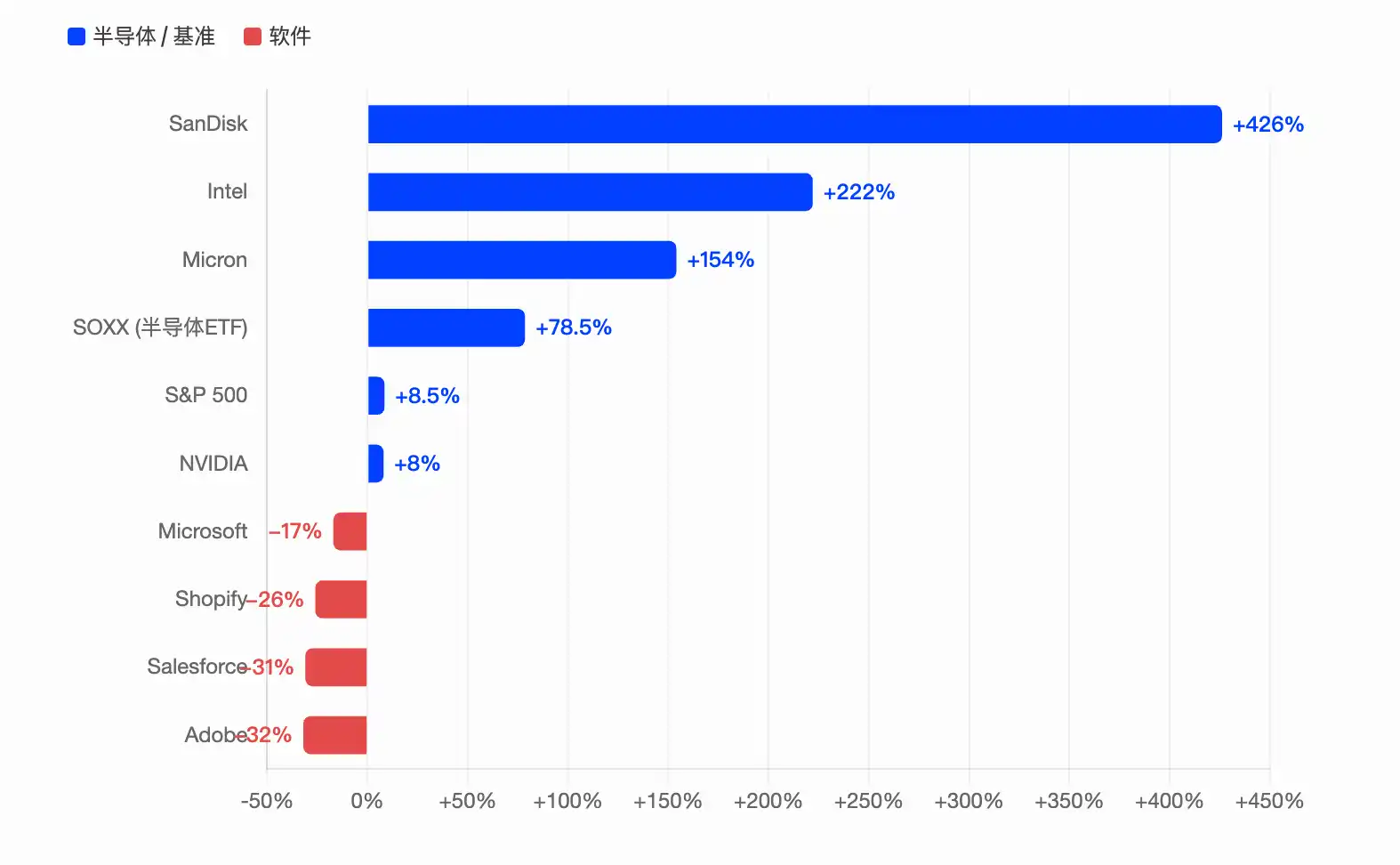

SanDisk leads the S&P 500 with a 426% annual gain, Intel has tripled, Micron is up 154%, while Microsoft, Adobe, and Salesforce have all dropped more than 17% year-to-date. The four hyperscale compute companies' combined capital expenditures for 2026 are nearing $700 billion. Capital is pouring into the chip supply chain like a black hole, while the software sector faces a double squeeze from AI displacement narratives and fund outflows.

Recently, a hot post on the Reddit investment forum overseas stated that semiconductor stocks are "basically a black hole sucking everything else in," which resonated widely.

Data confirms this intuition. As of the May 22nd close, the iShares Semiconductor ETF (SOXX) has returned 78.5% year-to-date, while the iShares Expanded Tech-Software ETF (IGV) has returned -12.5%. Two ETFs belonging to the same broad technology category show a year-to-date performance gap exceeding 90 percentage points.

According to Tickeron statistics, all software stocks in the S&P 500 are currently trading below their 200-day moving averages, while about 89% of semiconductor stocks remain above their 200-day moving averages. Both sectors fell in sync to the zero line during the 2022 bear market, after which their trajectories completely diverged. This split was not gradual but explosive.

SanDisk up 426% leads S&P 500, Intel's triple gain crushes AMD

The numbers are even more dramatic at the individual stock level.

According to Benzinga Pro data, SanDisk (SNDK) has risen about 426% year-to-date, making it the best-performing stock in the S&P 500 in 2026, following a 559% surge in 2025. This storage chip company, spun off from Western Digital, has seen NAND flash prices rise over 200% year-over-year driven by AI, with March quarter revenue growing 250% to $5.95 billion and non-GAAP gross margins reaching a high 78.4%.

According to 24/7 Wall Street, Intel (INTC) has risen about 222% year-to-date to $225, doubling AMD's gain. Intel's rebound comes from an extremely low base, coupled with progress on its 18A process node, rumors of Apple foundry orders, and yield improvement data disclosed by CEO Patrick Gelsinger in a CNBC interview. Short sellers have been severely squeezed; according to S3 Partners data, since the March 30th low point, Intel's market cap has increased over $440 billion, resulting in paper losses exceeding $12 billion for short sellers.

Micron (MU) has risen about 154% year-to-date, with a cumulative gain of 661% over the past 12 months. Earnings support this move; for the fiscal 2026 second quarter, revenue was $23.9 billion, up 196% year-over-year, with adjusted earnings per share of $12.20, far exceeding market expectations of $9.21. DRAM accounted for 79% of total revenue, with High Bandwidth Memory (HBM) being a key driver. SK Hynix Chairman Chey Tae-won even predicted that the memory chip shortage could last until 2030.

In contrast, NVIDIA (NVDA), the true "money printer" of AI compute, has risen about 8% to $15 year-to-date, performing far worse than the aforementioned second-tier semiconductor companies. According to The Motley Fool, NVIDIA's current forward P/E ratio is about 21.5x, almost on par with the S&P 500's 20.3x. This means the market is no longer paying a growth premium for NVIDIA; capital is instead flowing towards chip companies with lower valuations and greater potential upside.

$700 Billion in Capex: The Hyperscale Compute Companies' 'Arms Race'

Behind the semiconductor surge is real money.

According to data compiled by the Financial Times and multiple institutions, the combined capital expenditures for 2026 by the four hyperscale compute companies—Microsoft, Alphabet (Google's parent), Amazon, and Meta—are projected to be between $650 billion and $725 billion, nearly doubling from about $410 billion in 2025. This represents the largest concentrated infrastructure investment cycle in tech history.

According to Tom's Hardware, Jefferies analyst Brent Thill stated bluntly: "The AI economy is healthy. The bear thesis is garbage."

Specifically: Amazon leads with a single-quarter capex of $44.2 billion, with AWS growing 28%; Alphabet's Q1 capex was $35.67 billion, doubling year-over-year, with Google Cloud backlog jumping above $460 billion; Microsoft's calendar 2026 capex is projected at $190 billion, with about $25 billion attributed to price increases in memory chips and components; Meta raised its full-year capex guidance to $125-$145 billion.

According to statistics from Om Malik's blog, three of the hyperscale compute companies recorded significant non-cash investment gains in their Q1 earnings: Alphabet recorded $36.8 billion (primarily from Anthropic equity appreciation), Amazon recorded $16.8 billion, and Microsoft recorded $5.9 billion (from OpenAI). While capital expenditures are burning cash fiercely, the AI investment targets themselves are also appreciating.

Software Stocks Slaughtered by AI Displacement Narrative, IGV Posts Worst Drop Since 2008

The other side of the coin is the brutal collapse of software stocks.

According to The Motley Fool, after Anthropic released Claude Code in early 2026, the software sector experienced a sharp decline—the market's logic was not to reward AI innovation but to punish those SaaS companies potentially displaced by AI. IGV recorded its largest drop since 2008 at one point.

As of late May, Microsoft is down about 17% year-to-date, Adobe down about 32%, Salesforce down about 31%, and Shopify down about 26%. The S&P 500 Software & Services Index is about 21% below its 200-day moving average, the largest such deviation since June 2022. According to Goldman Sachs and other institutional data, short positions in mid-to-large software companies have surged sharply over the past three months, with cybersecurity and SaaS companies being the most heavily targeted areas for shorts.

Two layers of logic underlie this divergence. The first is direct capital siphoning: market liquidity is finite. When $700 billion in capex pushes chip stocks into parabolic moves, capital must be withdrawn from somewhere. As the author of that Reddit post said: "Fundamentally decent software companies just sit there or bleed slowly, while the semiconductor index goes vertical."

The second is a revaluation of the narrative. The rapid evolution of AI agents is prompting the market to re-evaluate the moats of SaaS business models: when AI can automate programming, form-filling, and customer service, how long can subscription models based on per-seat fees last? The Motley Fool points out that software companies likely to survive will need features like real data, proprietary workflows, and deep customer integration that are difficult for AI to replicate.

Cycle Peak or Structural Shift? Two Key Questions Remain Unanswered

That Reddit user ended the post with two questions, representing investors' ultimate doubts about whether the semiconductor rally can persist.

However, these two questions remain unanswered.

First: How long can the hyperscale compute companies' capital expenditures be sustained?

According to CNBC, Pivotal Research projects Alphabet's 2026 free cash flow will plunge nearly 90% from $73.3 billion in 2025 to $8.2 billion. Of Microsoft's $190 billion annual capex, $25 billion is consumed just by price increases in memory chips and components. These companies are betting future profits on AI revenue that has not yet fully materialized.

Second: Is software the next rotation target?

According to Bank of America's Chief Investment Officer Hartnett's previous judgment in the Flow Show report, software is one of the best contrarian long positions for Q2 2026, given the extreme deviation of the sector relative to its 50-day and 200-day moving averages.

However, this does not mean the semiconductor rally is over. The Philadelphia Semiconductor Index (SOX) recorded a historic streak of 18 consecutive daily gains on April 25th, rising about 45% during that period. According to Intellectia analysis, some veteran analysts are beginning to compare the current move to the 1999-2000 internet bubble, warning of a potential 25% to 30% correction. But SOX has been up in 22 of the past 23 trading days, setting 15 intraday record highs; this momentum is itself a signal.

As that Reddit user said: "I don't want to call a top because I've been slapped in the face too many times before. But the extreme concentration of gains in a single sector is starting to smell like the late stages of a cycle."