Sentiment around cryptocurrency memecoin launch platform Pump.fun [PUMP] has turned positive again following renewed interest in memecoins over the past day.

The platform’s native token moved alongside that momentum, with PUMP surging 12% over the past day.

Even so, the rally remained tied to the platform’s underlying health, leaving investors exposed if protocol activity failed to recover.

Why are investors buying PUMP?

PUMP’s recent rally has coincided with growing investor participation. The token’s holder count reached a record 122,440, while retail investors accounted for roughly 38% of holders.

That increase also appeared in on-chain data, suggesting fresh capital supported the recent move.

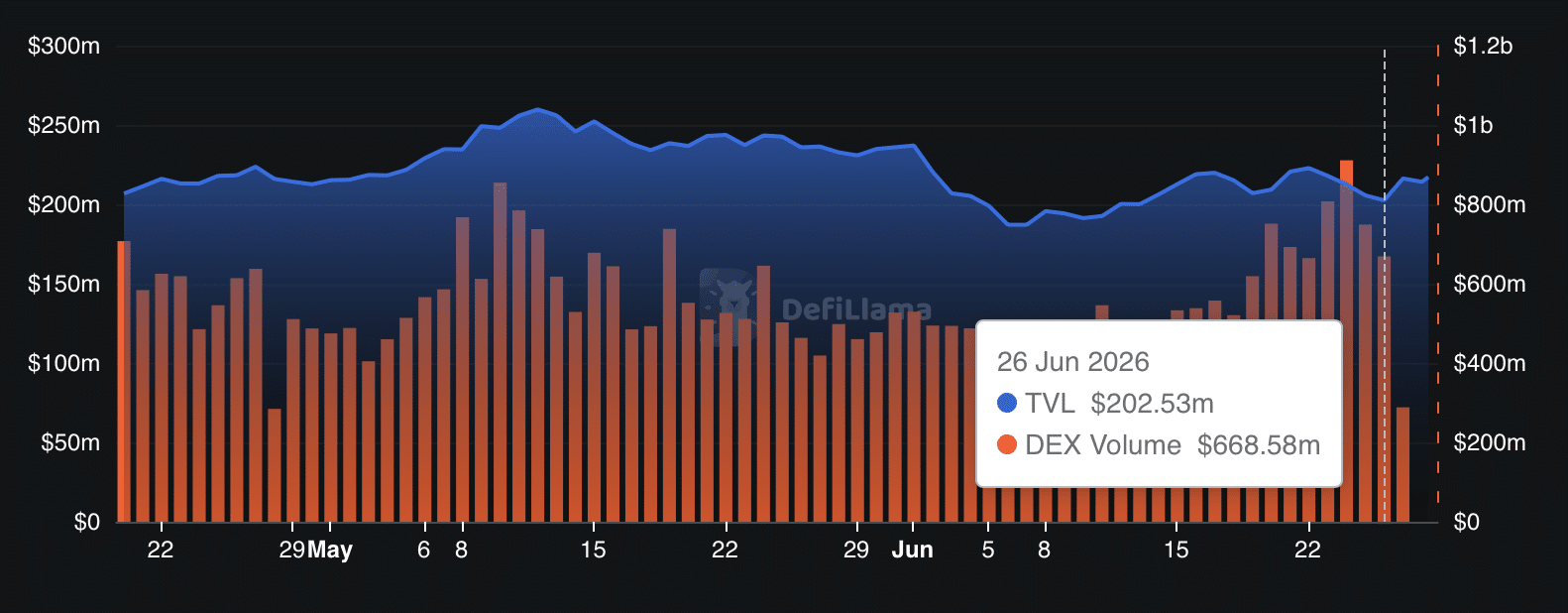

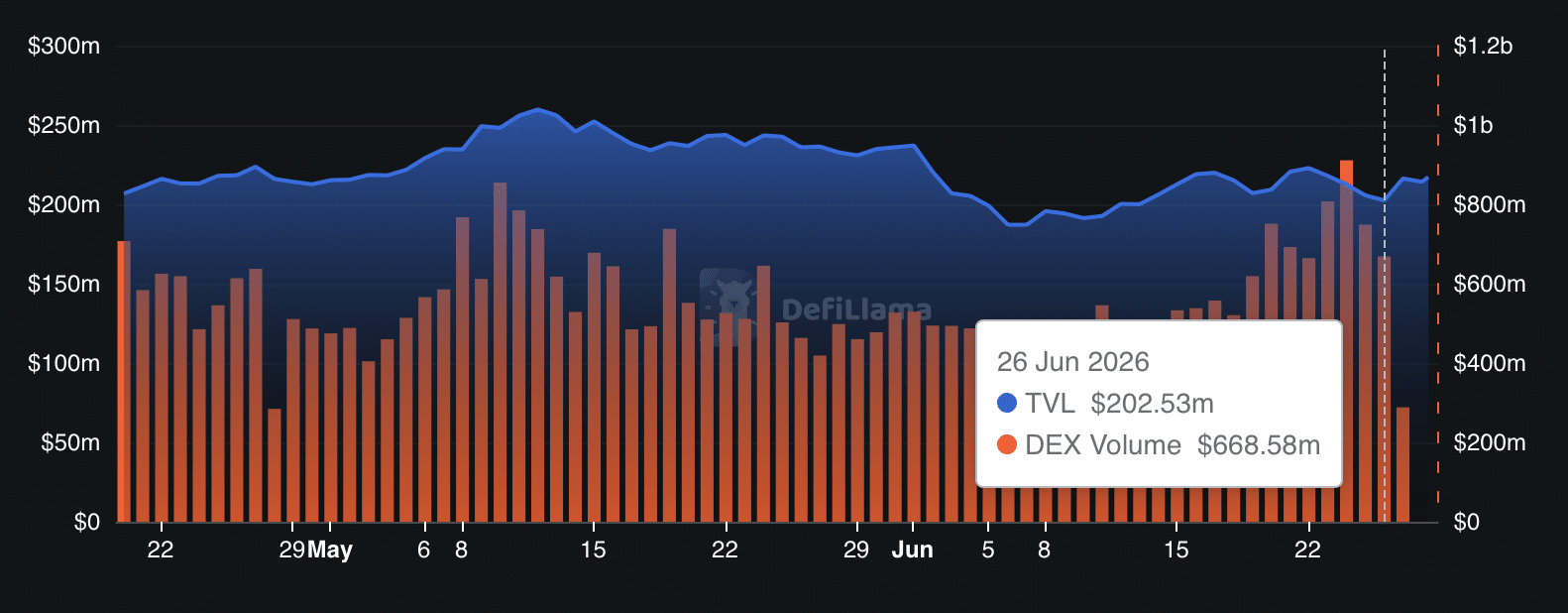

Between the 26th of June and now, investors added roughly $15.7 million to Total Value Locked (TVL), lifting it to $217.7 million. Those inflows suggested investors committed more capital despite recent volatility.

Total Value Locked measures assets deposited into DeFi protocols. Rising TVL often reflects stronger long-term conviction while investors earn yield.

Is the protocol keeping up?

However, rising TVL did not match the protocol’s underlying performance.

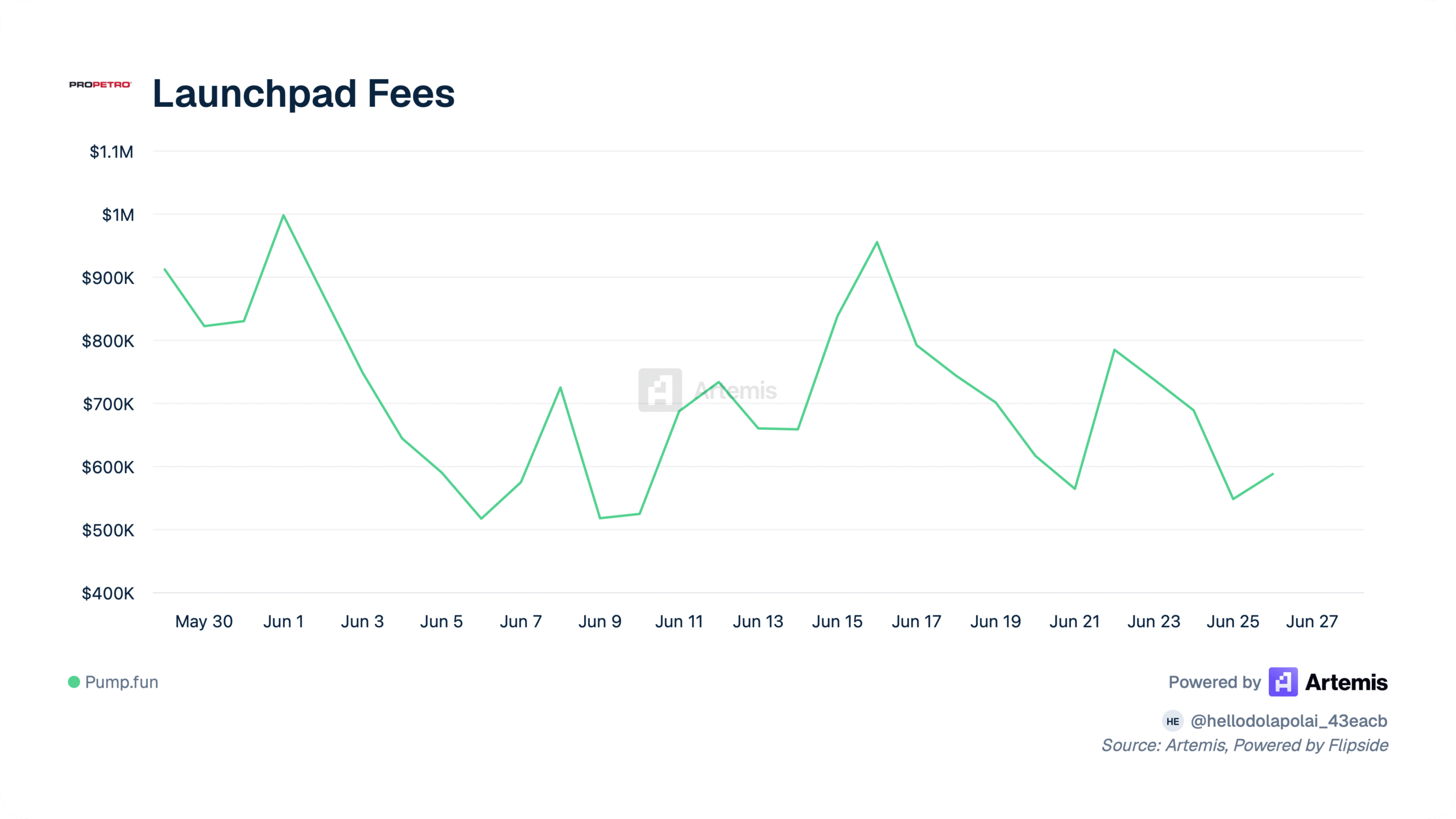

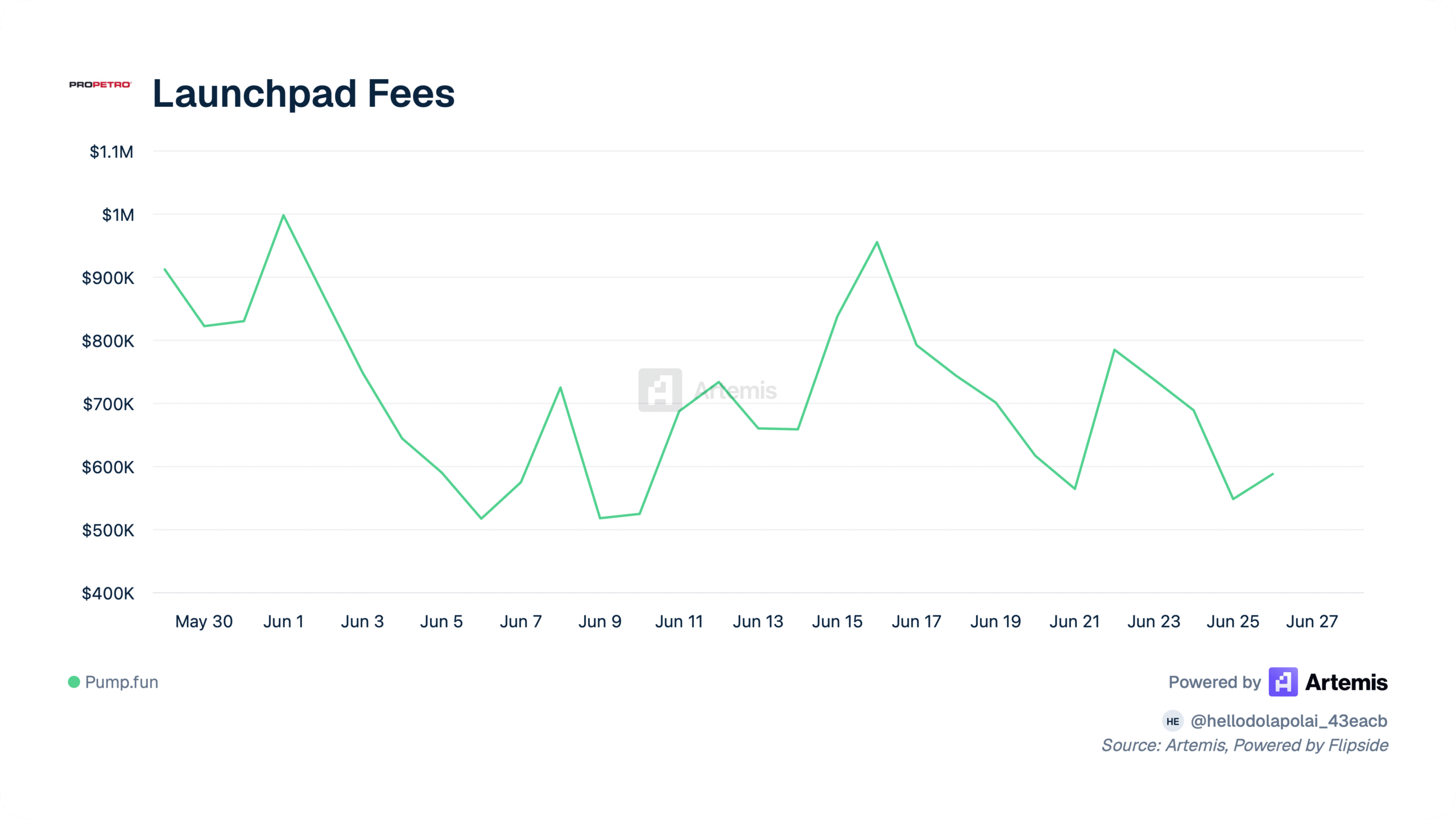

Pump.fun continued underperforming across key metrics, including revenue, fees, and launchpad volume.

Data from Artemis showed launchpad volume and fees generated by memecoins on the platform fell 86.7% and 35.6% to $5.8 million and $587,200, respectively.

Those declines suggested user activity remained weak despite improving investor sentiment.

Lower activity reduced fee generation and limited protocol utility, making it harder for the recent price recovery to gain stronger fundamental support.

Revenue reflected the same trend.

Protocol revenue fell 23% to $147.8 million, reinforcing signs of slowing activity.

Historically, sustained token rallies have been easier to support when protocol usage improves alongside price. Until those metrics recover, PUMP’s recent optimism could remain vulnerable.

Final Summary

- PUMP gained 12%, holder count hit a record, and TVL increased sharply, signaling renewed market interest.

- If protocol metrics fail to recover, investor optimism may prove difficult to sustain.