Original / Odaily Planet Daily (@OdailyChina)

Author / Wenser(@wenser2010)

Recently, Alliance DAO founder qw(@QwQiao) dropped a bombshell opinion: "Blockchain moats are limited," rating the moat of L1 public chains at a mere 3/10.

This statement quickly ignited the overseas crypto circle, sparking heated discussions among crypto VCs, public chain builders, and KOLs. Dragonfly partner Haseeb angrily retorted that rating the "blockchain moat at 3/10" was utterly ridiculous, noting that even Aave founder Santi, who dislikes the industry's gambling tendencies, never believed blockchain "has no moat."

Debates about the meaning, value, and business models of blockchain & cryptocurrency consistently resurface throughout market cycles. The crypto industry constantly oscillates between idealism and reality: people nostalgically yearn for the original decentralized ideals while simultaneously craving the status and recognition of the traditional financial industry, all while being deeply mired in self-doubt about whether it's "just a repackaged casino." The root of all these contradictions perhaps lies in scale—the total market capitalization of the crypto industry has hovered around $3-4 trillion, still appearing minuscule compared to traditional financial giants often worth hundreds of billions or even trillions of dollars.

As practitioners in the industry, everyone harbors a contradictory psychology of both arrogance and inferiority—arrogant about blockchain's birth embodying Satoshi Nakamoto's ideal of de-monetization and decentralized spirit, and about the crypto industry indeed becoming an emerging financial sector that is gradually gaining attention, acceptance, and participation from mainstream forces; the point of inferiority, however, is probably like a poor kid always feeling that what they are doing isn't quite honorable, filled with blood, tears, bitterness, and pain from a zero-sum game where people prey on each other. In short, the limitations of the industry's scale have bred this cyclical identity anxiety, self-doubt, and self-denial.

Today, let's use the topic of "moat business ratings" raised by qw to discuss the existing chronic problems and core advantages of the crypto industry.

Origin of the Debate: Is Liquidity the Moat of the Crypto Industry?

This major industry discussion about "whether the crypto industry has a moat" originally stemmed from a statement by Paradigm team researcher frankie—"The greatest trick the devil ever pulled was convincing crypto people that liquidity is a moat."(Odaily Planet Daily Note: Original quote: the greatest trick the devil ever pulled was convincing crypto people that liquidity is a moat.)

It's clear that frankie, a "purebred" VC, somewhat scoffs at the current industry trend of highly推崇 "liquidity is everything." After all, for an investment manager or research expert who holds advantages in capital and information, they often hope their managed funds are spent on projects and businesses with real operational support, capable of generating genuine cash flow and continuously providing financial returns.

This view also gained agreement from many in the comments:

- Multicoin partner Kyle Samani directly said "+1";

- Ethereum Foundation member binji believed that "trust is the real moat; even if trust might flow opportunistically in the short term, liquidity will always reside where trust is placed."

- Chris Reis from Circle's Arc blockchain team also pointed out: "TVL always seems to be the wrong North Star metric (business guiding goal)."

- Justin Alick from the Aura foundation remarked somewhat jokingly: "Liquidity is like a fickle woman; she might leave you at any time."

- DeFi researcher Defi peniel stated bluntly: "Relying solely on liquidity is not a moat; hype can disappear overnight."

Of course, many also refuted this—

- DFDV COO & CIO Parker commented: "What are you talking about? USDT is the worst stablecoin but holds absolute dominance. Bitcoin is the (performance/experience) worst blockchain but holds dominant地位 absolutely."

- Former Sequoia investor, now Folius Ventures investor KD, simply asked: "Isn't it?"

- Fabric VC investor Thomas Crow pointed out: "In exchanges, liquidity *is* a moat—the deeper the liquidity, the better the user experience; this is the most important characteristic in this vertical industry, without exception. This is why major innovations in crypto asset trading focus on solving insufficient liquidity (which leads to worse user experience). Examples include Uniswap acquiring liquidity for long-tail assets through LPs, and Pump.Fun attracting pre-token launch liquidity through standardized contracts and bonding curves."

- Pantera investor Mason Nystrom retweeted and commented: "Liquidity is absolutely a moat." He then provided various examples: Among public chains, Ethereum leads today because of DeFi liquidity (and developers); among CEXs, Binance, Coinbase, etc.; among lending platforms, Aave, MakerDAO; among stablecoins, USDT; among DEXs, Uniswap, Pancakeswap.

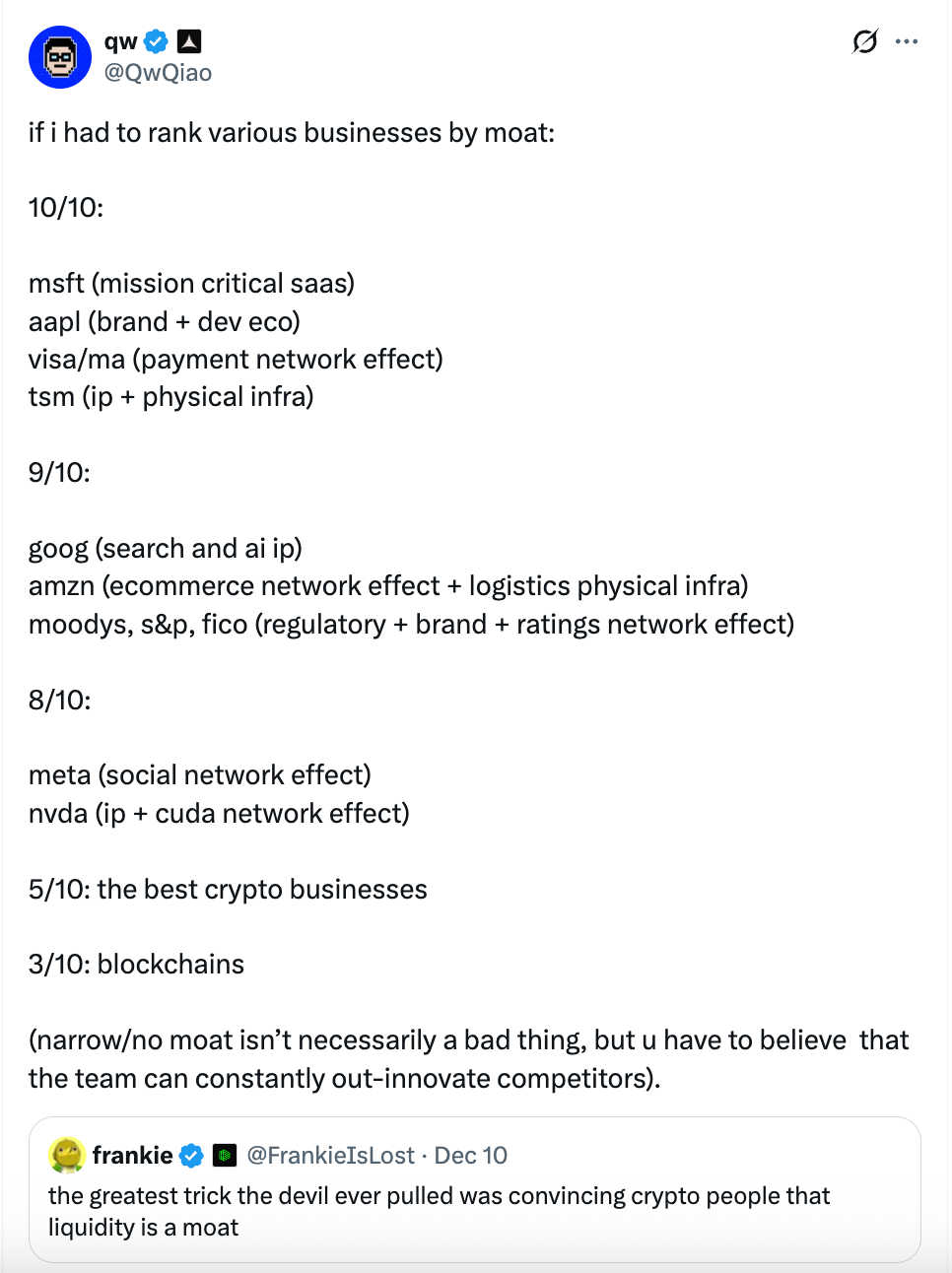

Then came the "moat rating" tweet from Alliance DAO founder qw:

In his view, the moat of the blockchain (public chain) itself is very limited, rated only 3/10.

- He believes Microsoft (key SaaS), Apple (brand + developer ecosystem), Visa/Mastercard (payment network effects), TSMC (IP + physical infrastructure) can score 10/10 (strongest moat);

- Google (search and AI IP), Amazon (e-commerce network effects + logistics infrastructure), rating agencies like Moody's, S&P, FICO (regulation-driven + brand + rating network effects), large-scale cloud computing (AWS/Azure/GCP etc.) can score 9/10;

- Meta (social network effects), NVIDIA (IP + CUDA network effects) score 8/10;

- The best crypto businesses in the crypto industry score 5/10;

- Public chains (blockchains) score only 3/10 (narrow moat).

qw further stated that a low moat score isn't necessarily bad, but it means teams must continuously lead innovation, otherwise they will be quickly replaced. Later, perhaps feeling the initial rating was too hasty, he added some supplementary ratings in the comments:

- The 3 major cloud service infrastructure providers score 9/10;

- BTC's moat scores 9/10 (Odaily Planet Daily Note: qw pointed out that no one can replicate BTC's founding story and the "Lindy Effect," but deducted 1 point because it's unclear if it can handle security budget and quantum threats);

- Tesla 7/10 (Odaily Planet Daily Note: qw believes automated IP like self-driving is insane, but the car industry is commoditized, and humanoid robots might be similar)

- Lithography machine manufacturer ASML 10/10.

- AAVE's moat score might be higher than 5/10, qw's reason: "As a user, you must trust their smart contract security testing is thorough enough not to lose your funds".

Of course, seeing qw so grandly play the "sharp critic," besides debates about the "moat system," some in the comments made unrelated sarcastic remarks, even mentioning: "What about those terrible launch platforms you invested in?" (Odaily Planet Daily Note: After investing in pump.fun, Alliance DAO's subsequent investments in one-click token issuance platforms (like Believe) performed poorly, even he himself didn't want to rate them)

With such a火药味十足 (fireworks-filled) focal topic, Dragonfly partner Haseeb's subsequent angry retort followed.

Dragonfly Partner's Inner OS: Nonsense, I've Never Seen Someone So Shameless

Responding to qw's "moat rating system," Dragonfly partner Haseeb posted angrily: "What? 'Blockchain moat: 3/10'? That's kinda absurd. Even Santi doesn't think public chains 'have no moat'.

Ethereum has held a dominant position for *10 consecutive years*, hundreds of challengers have raised over $10 billion trying to grab market share. After a decade of competitors trying to defeat it, Ethereum has successfully defended its throne every time. If that doesn't indicate Ethereum has a moat, I don't know what a moat is!"

In the comments of this tweet, qw gave his perspective: "You're talking about looking back ('the past ten years') and it's factually incorrect (on multiple metrics Ethereum no longer holds the throne)."

Subsequently, the two exchanged several rounds on "what exactly is a moat?" and "does Ethereum really have a moat", with qw even pulling out a post he made in November, pointing out that the "moat" in his mind is actually revenue/profit. But Haseeb immediately counterargued with examples—once-popular crypto projects like OpenSea, Axie, BitMEX, although they had high revenues, actually had no moat; the real moat should focus on—"can it be replaced by competitors".

Abra Global management director Marissa also joined the discussion: "Agree (with Haseeb). qw's statement is a bit strange—switching costs and network effects can be strong moats—Solana and Ethereum both have these, I think they will be stronger than other public chains over time. They both have strong brands and developer ecosystems, clearly also part of the moat. Maybe he's referring to other public chains that don't have the above advantages."

Haseeb continued, full of sarcasm: "qw is just splitting hairs, asking for trouble."

Based on the above discussion, perhaps we should break down the "real moat" of public chains in the cryptocurrency industry and what aspects it comprises.

The 7 Components of a Public Chain Moat: From People to Business, From Origin to Network

In my opinion, the main reasons why qw's "moat rating system" seems somewhat unable to justify itself are:

First, its rating标准 only looks at current industry status and revenue while ignoring multi-dimensional evaluation. Whether it's infrastructure like Microsoft, Apple, Amazon Web Services, or payment giants like Visa, Mastercard, the main reason qw gives high scores is their strong revenue models, which obviously oversimplifies and superficializes the business moat of a giant company. Moreover, Apple's global market share is not dominant, and payment giants like Visa also face challenges like market shrinkage and regional business decline.

Second, it overlooks the complexity and uniqueness of public chains and crypto projects区别于 (differentiating them from) traditional internet businesses. As challengers to the fiat system, cryptocurrency, blockchain technology, and subsequent public chains and crypto projects立足点 (base themselves) on the inherent "anonymity," "nodality" of decentralized networks, which is often something traditional revenue-driven businesses cannot achieve.

Based on this, I believe the moat of public chain businesses mainly lies in the following 7 aspects, including:

1. Technical Philosophy. This is also the biggest advantage and differentiating feature of the Bitcoin network, Ethereum network, Solana network, and countless public chain projects. As long as humanity remains wary of centralized systems, authoritarian governments, and the fiat system, and accepts the concepts of sovereign individuals and related viewpoints, the real demand for decentralized networks will always exist;

2. Founder Charisma. Satoshi Nakamoto disappeared after inventing Bitcoin and ensuring the Bitcoin network ran smoothly, sitting on tens of billions of dollars in assets but unmoved; from a World of Warcraft enthusiast abused by the game company to Ethereum co-founder, Vitalik resolutely embarked on his decentralized spiritual journey; Solana founder Toly and others were originally elite engineers at US big tech companies but were unwilling to stop there, thus starting their own "capital internet" construction journey, not to mention the various public chains built inheriting the ambition of Meta's Libra network with the Move language. The personal charm and appeal of founders are particularly important in the crypto industry. This is also why countless crypto projects receive VC favor, community追捧 (praise), and capital influx because of their founders, but also fade into obscurity due to founder resignation or accidents. A good founder is the true soul of a public chain乃至 (and even) a crypto project;

3. Developer and User Network. On this point,正如 (just as) the Metcalfe effect and Lindy effect emphasize, the stronger the network effect of something and the longer it exists, the more likely it is to persist. The developer and user network is the cornerstone of public chains and many crypto projects, because developers can be said to be the first and most enduring users of a crypto public chain or project;

4. Application Ecosystem. A tree with roots but no branches and leaves can hardly survive, and the same goes for crypto projects. Therefore, a rich application ecosystem capable of self-closure and synergistic effects is crucial. The reason why public chains like Ethereum and Solana can survive the winter and still exist is inseparable from the various application projects that are always building. Furthermore, the richer the application ecosystem, the more it can continuously generate造血 (blood-making), feeding back to the public chain;

5. Token Market Cap. If the aforementioned are the inner part and foundation of a "moat," then the token market cap is the external form and brand image of a public chain and a crypto project. Only when you "look expensive" will more people believe you "have a lot of money," that you are a "gold mining ground." This is true for individuals, and likewise for projects;

6. Openness to the Outside. Besides building their own internal循环 (circulation) ecosystems, public chains and other crypto projects also need to maintain openness and operability and exchange value with the external environment. Therefore, openness to the outside is also crucial. Taking public chains like Ethereum and Solana as examples, this refers to the convenience and scale of their bridging with traditional finance, user fund inflows/outflows, and various industries through windows like payments and lending;

7. Long-Term Roadmap. A truly solid moat must not only provide support in the short term but also constantly update, iterate, and innovate, maintaining its own vitality and longevity in the long term. For public chains, the long-term roadmap is both a North Star metric and a powerful抓手 (lever) to激励 (incentivize) continuous development and innovation inside and outside the ecosystem. Ethereum's success is closely related to the planning of its long-term roadmap.

Based on the above elements, a public chain can grow from zero to one, from nothing to something, gradually moving through the野蛮生长 (wild growth) period into the mature iteration period. Corresponding liquidity and user stickiness will naturally follow.

Conclusion: The Crypto Industry Has Not Yet Reached the Stage of "Competing on Talent"

Recently, Moore Threads, known as the "Chinese version of NVIDIA," successfully listed on the Hong Kong stock market, achieving a milestone of 300 billion CNY on its first day of trading; then, within just a few days, its stock price soared all the way, reaching another astonishing breakthrough with a market cap exceeding 400 billion CNY today.

Compared to Ethereum, which took 10 years of operation to finally reach a $300 billion market cap, Moore Threads covered 1/7 of that journey in just a few days. And compared to US stock giants often worth trillions, the crypto industry is even more insignificant.

This makes us sigh again that today, with the scale of capital and user involvement far smaller than the financial and internet industries, we are far from the stage of "competing on talent." The only pain point of the crypto industry today is that we don't have enough people, we don't attract enough capital, and the industries involved are not broad enough. Rather than worrying about those grand, all-encompassing "moats," perhaps what we should think about is how cryptocurrency can更快 (faster), lower cost, and more conveniently meet the real needs of more market users.