Author: Ba Xiaoling, Wu Xiaobo Channel

"Over the long term, capital markets will eventually become 'desensitized' to regional conflicts and internalize the long-term impacts of war as part of macroeconomic data."

On April 12th in Islamabad, the U.S. and Iran returned home, and subsequently, news of the "failed talks" swept the globe and continues to ferment.

The good news is that the market has 24 hours to digest this shock; the bad news is that no one knows if 24 hours will be enough.

News of Iran and the U.S. failing to reach an agreement makes the headlines

Over 90% of geopolitical conflicts fade from market view within two weeks, but the remaining 10% are enough to change the world.

Since the outbreak of the U.S.-Iran war, the market has been tormented for a full six weeks by the "frenzied operations, rises and falls all depending on Trump."

In the past March, from A-shares to Hong Kong stocks and U.S. stocks, major indices generally corrected by over 4%. Individual stocks fared even worse, with over 85% of A-share stocks falling, with a median decline of 11.5%, equivalent to the average retail investor suffering a limit-down drop.

However, the market has recently begun to show signs of gradually becoming "desensitized" to the war.

Based on this change, we synthesized the views of 11 financial experts and economists to produce the "April 2026 Wealth Growth Report," attempting to find investment clues amidst the turbulent war situation and provide reference for asset allocation in the coming month.

This report, approximately 18,000 words long, mainly revolves around three core questions:

◎ Is April a good time to "pick up bargains"?

◎ When will the U.S.-Iran war end? How big is its impact on the market?

◎ Under a "wartime economy," how should investors allocate assets?

Is April a Good Time to 'Pick Up Bargains'?

On the investment calendar, every April is a typical "moment of decision."

Unlike February-March when the market is in a data vacuum, after entering April, Q1 macroeconomic data gradually becomes clear, listed companies' annual reports and Q1 reports are集中 disclosed, and the market shifts from "expectation-driven" to "reality-priced."

In other words, the April market believes more in "what you see is what you get."

More importantly, despite the big drop, the current market is not short of ammunition.

According to Dongwu Securities estimates, in early April, the turnover of the two markets remained above 1.6 trillion, higher than most of last year;

The同期 margin balance was 2.58 trillion, only slightly down from the early March high, showing that leveraged funds have not withdrawn on a large scale;

The total share of equity ETFs, representing long-term market funds, remained at 2.10 trillion shares, down only 11.9 billion shares from the early March high, overall stable;

In addition, A-share new account openings in March were about 4.6 million, still at a historical high, indicating undiminished enthusiasm among residents to enter the market.

This means that even under the impact of geopolitical conflicts, potential buying power in the market is still sufficient. Once a market reversal occurs, these funds are likely to quickly transform into new incremental entries.

So where will the funds flow first?

Most institutions believe that when market trends tend to ease, those companies that simultaneously possess "valuation repair space, oversold rebound potential, and performance support" will更容易 attract funds back.

The reason is that some quality assets often fall to a "good price" amidst the general decline.

In the report, we also invited 9 experts to make predictions on the rise and fall of eight assets: the Hang Seng Index, CSI 300, Japanese and South Korean stocks, U.S. stocks, the U.S. dollar index, gold, first-tier city real estate, and crude oil. At the same time, they provided allocation suggestions for eight investment targets: STAR 50 ETF, stocks with performance reversal or valuation repair concepts, Hang Seng Tech ETF, Consumer ETF, gold, U.S. bonds, HALO concept stocks, and货币 funds.

Among them, the most favored market is the Hang Seng Index, with 7 people bullish and no one bearish. The most favored investment targets are the STAR 50 ETF and stocks with performance reversal or valuation repair concepts, followed by the Hang Seng Tech ETF and gold.

Experts believe that Hong Kong stocks have already fully priced in liquidity tightening and the impact of the war. Therefore, after extreme overselling, Hong Kong stocks are expected to usher in a "valuation correction," becoming one of the markets with the greatest rebound elasticity in April.

At the same time, 4 experts bullish on the CSI 300 index also基于 similar reasons, pointing out that against the backdrop of strong domestic fundamental data in March, the market has shown obvious signs of overselling.

When Will the U.S.-Iran War End?

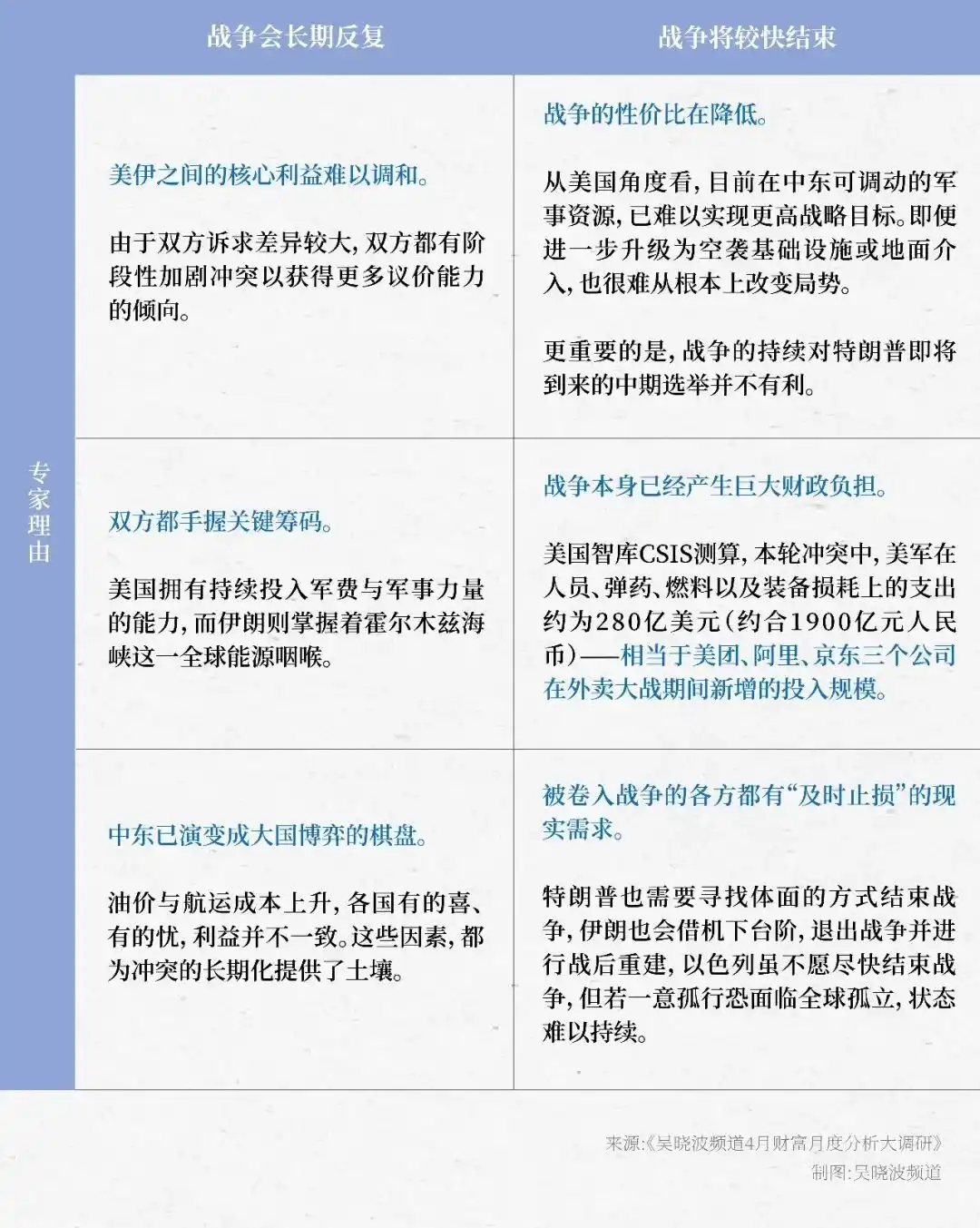

Although the experts gave their respective judgments, most still emphasized that the repetitiveness and long-term impact of the war will continue to disturb the market. They普遍建议 investors remain restrained—"the later the布局, the stronger the certainty."

So, in the experts' view, when will the conflict end? And how big is the impact on the market?

The survey results show significant divergence among the 11 experts: 4 believe the war will be difficult to end in the short term, 3 believe it will end relatively quickly, and 4 say it is difficult to judge.

Experts who believe the conflict will be long-term and repetitive mainly base their view on both sides' dissatisfaction with the "gains" from the war, while those who believe the war will end quickly理由更多 from a cost perspective (see table below).

However, whether the future is "fight and talk" or "talk and fight," the experts' consensus is clear:

"Capital markets will eventually become 'desensitized' to regional conflicts and internalize the long-term impacts of war as part of macroeconomic data."

In this regard, they suggest investment strategies can be more pragmatic: rather than guessing when the war will end, it is better to accept it as part of reality and reprice it within the framework of a "wartime economy."

Under this framework, one of the most important changes is the rise in the center of oil prices, which is unlikely to fall back to pre-war levels in the short term.

Corresponding to the Chinese market, on the one hand, rising oil prices will drive a "price increase行情," and on the other hand, the allocation status of Chinese assets may be further enhanced.

Under the Wartime Economy, the 'Price Increase行情' is Coming

As early as March, at the major brokers' spring strategy meetings, two core themes were invariably mentioned: the "AI narrative" and "PPI stabilization and recovery."

The PPI (Producer Price Index), since turning negative in October 2022, had been in negative growth territory for 41 consecutive months by February 2026.

And PPI repair will directly benefit upstream corporate profits and support the overall market. Historical experience shows that systemic bear markets usually do not occur in the early stages of PPI recovery.

According to Yuekai Securities analysis, before the geopolitical conflict occurred, the fundamental driving force for PPI recovery came from the continuous improvement in supply and demand relations: first, the rapid development of global artificial intelligence driving computing power and energy investment; second, fiscal efforts pulling infrastructure investment; third, "anti-involution" policies promoting continuous optimization of market competition秩序.

Based on this, most institutions believe that the "price increase concept" brought by PPI recovery is expected to become one of the clearest investment themes this year.

Specifically, upstream price increases will bring cost pressure to midstream and downstream. Therefore, in the initial stage of PPI recovery, the market tends to配置 those enterprises with price transmission capabilities, i.e., companies with brand, channel, or industrial chain advantages that can pass costs to the end consumer.

However, in March 2026, driven by soaring energy prices, PPI rose 0.5% year-on-year, turning positive from negative "ahead of schedule."

According to Guolian Minsheng Securities estimates, if oil price factors are excluded, the improvement in PPI is not significant, and there is a possibility of冲高回落 in the third quarter. But this price signal still helps change corporate behavior and consumer confidence under the previous low inflation.

At the same time, under the "wartime economy" framework, many institutions judge that the overall allocation value of Chinese assets is rising.

The reason is that in a global environment dominated by "supply shocks," capital tends to be allocated towards safety and efficiency. Therefore, China, with its stable energy supply, complete industrial system, highly resilient supply chain, and mature industrial配套, has significant advantages in these two aspects.

This means that Chinese assets, including A-shares and Hong Kong stocks, are expected to occupy a more important position in this round of global asset rebalancing.

Big Head Has Something to Say

Finally, attached is the experts' detailed version of April allocation and financial advice for reference.

Market irrationality often lasts longer than expected. Rather than guessing unpredictable inflection points, it is better to prepare asset allocation and risk isolation in advance.

At the market level, I am optimistic about tech stocks. Although valuations are indeed not low, high valuations themselves do not mean that a bubble "must burst." Unlike the 2000 internet bubble, the tech giants dominating the market today have strong free cash flow, real huge profits, and deep industry barriers, with risk resistance far greater than back then. In fact, the premise for tech companies to maintain high valuations currently is that profit growth or liquidity support has not reversed.

In terms of time and space, this round of slow bull and long bull market is still in the first half.

It is recommended that investors maintain confidence and patience, actively关注错杀优质 stocks or funds to grasp the next round of market rally opportunities. In the bottom area of market adjustment, do not easily lose quality筹码.

At the same time, it must be seen that structural differentiation will continue. This year, the "new barbell strategy" can continue to be adopted: one end of the "barbell" is technology龙头 stocks representing technological innovation, such as those重点 mentioned in the "15th Five-Year Plan" like robots, chips and semiconductors, computing power algorithms, commercial aerospace, solid-state batteries, controllable nuclear fusion, etc.; the other end is traditional blue-chip stocks with heavy assets and low volatility, such as "HALO assets" like power grid equipment, non-ferrous metals, coal, oil and gas.

Overall bullish on the后市. The next month coincides with the Q1 report disclosure period. It is recommended to focus on the performance主线,重点关注 export-oriented advanced manufacturing, i.e.,布局 in the two major directions of technology + cycle.

In terms of timing, before the impact of the U.S.-Iran conflict completely钝化, the market may still experience large fluctuations. Therefore, the later the布局 time, the stronger the certainty.

◎ First, the core strategy is "adaptation." In the current environment, responding to changes is more important than prediction. Do not大幅度 cut positions due to panic, as it is easy to fall before dawn.

◎ Second, the practical advice is to maintain positions and shift the focus towards defensive sectors. Hang Seng Tech has already fallen thoroughly, many good companies are in an oversold state, and you can go in batches to "pick up bargains," but it is not recommended to heavily weight at this stage because tech stocks are now too volatile and too affected by sentiment.

◎ Third,关注 the following opportunities: keep an eye on short-term U.S. bonds, the current yield is very cost-effective; gold is an unshakable hedging asset under geopolitical risks.

Big fluctuations are actually a "touchstone" for good companies. Taking advantage of market chaos, you can instead pick out those quality companies that have been错杀 for long-term布局.

Wars are always about fighting and talking, talking and fighting. However, the market will go from initially being affected by Trump's "line drawing" to later becoming desensitized. For investors, the key is to invest, not speculate.

Against the背景 of unclear geopolitics, appropriately配置 some broad-based indices like the CSI 300 or CSI A500 is a good choice, offering both offensive and defensive capabilities. Increase the proportion of sector ETFs appropriately when the situation becomes clearer. For individual stocks, it is better to maintain low allocation.

In addition, short-term market fluctuations are difficult to predict, but the following can be expected:

First, the 2026 Q1 report has guiding significance for the full year's performance. Therefore, sectors that perform well or exceed expectations are expected to be favored by the market.

Second, you can关注 the two logics of price increase and going global. The former is more concentrated in upstream non-ferrous metals and chemicals, the latter more in equipment and machinery companies. However, considering that non-ferrous metals and chemicals have偏高 valuations, focusing on the machinery sector might have a higher probability of rising.

Currently, U.S. stocks, A-shares, and gold are all at relatively high valuations overall.

For individual investors, it is currently recommended to be guided by absolute returns,优先配置 low-risk assets such as bonds and货币 funds, while moderately搭配 consumption sector ETFs and gold with relatively reasonable valuations; for the stock portion, you can关注 dividend assets, large-cap indices, and avoid themes and small and micro-cap styles that have risen too much previously. Avoid following the crowd and thematic investing, wait quietly for opportunities.

Short-term看好 A-share oversold rebound opportunities, medium-term看好 consumption and real estate industry chain.

At the global market level, the valuations of U.S. tech stocks and Hong Kong tech stocks have currently fallen to the bottom of the valuation range of the past two years. Among them, the average valuation of large U.S. tech companies has fallen below 25 times, moving towards 20 times. The普遍 valuation of large Hong Kong tech companies is below 20 times.

And the profit growth of these tech companies is still strong, accompanied by large buyback support. If the adjustment continues and valuations fall another step, it would反而 be a good抄底 opportunity for medium- and long-term funds.

Facing uncertain geopolitics, it is recommended that investors recently operate with half positions, at most two-thirds positions.

In terms of sectors, I am personally quite optimistic about domestic substitution in semiconductors and commercial aerospace, especially low-market-cap,单项冠军 in a certain field. The U.S. is currently酝酿 a new round of unprecedented semiconductor control bills, which will benefit NVIDIA in the short term and benefit Chinese semiconductor domestic substitution in the medium to long term. It is estimated that the market will追捧 the semiconductor domestic substitution sector in April, creating opportunities for the STAR 50 ETF.

The war has a certain impact on the后市, but it is a阶段性 factor, not a决定性 factor. The main part of the war is expected to end很快, but there is a long tail effect. The impact on the Strait and the global supply chain is expected to last for a relatively long time. Investors can dynamically grasp two opportunities: increasing allocation of错杀 assets and阶段性 profit realization of受益 assets like crude oil.

The charm of capital markets lies in the fact that even in extreme environments like war, there are布局 opportunities for超预期 returns.

It is recommended to relatively overweight the STAR 50 ETF and货币 funds, firmly standing on the main track of the national capital market narrative logic. In addition, April is the annual report season for the A-share market. It is recommended to be in空仓 or selectively建仓 a small amount in错杀绩优 stocks.