Author: José Maria Macedo, Delphi Labs Cofounder

Compiled by: Deep Tide TechFlow

Deep Tide Guide: The founder of Delphi Labs spent two weeks intensively visiting China's AI ecosystem, meeting a large number of founders, investors, and CEOs of listed companies.

His conclusion was unexpected: more optimistic about hardware than expected, more pessimistic about software than expected, and his views on Chinese founders overturned his previous perceptions.

The article also covers hot topics such as valuation bubbles, the humanoid robotics sector, and information asymmetry between China and the West.

Full text as follows:

I spent two weeks in China, meeting a large number of founders, VCs, and CEOs of listed companies within the AI ecosystem. Before going, I was bullish on this ecosystem, expecting to see world-class AI talent working at valuations far lower than in the West.

My perspective changed when I left—it became more specific: hardware is stronger than I imagined, software is weaker than I imagined, and some observations about Chinese founders also surprised me.

The Founder Problem

The exceptional founders I've invested in share a common trait: independent thinking, rebelliousness, extreme focus, and obsession. They don't follow the rules. They constantly ask "why" and refuse to accept second-hand wisdom. The decisions they make seem inexplicable to outsiders but feel obvious to them. They possess an intrinsic, unstoppable intensity, often manifested as a long-term obsession and excellence. As a VC who meets many smart people daily, this type of person stands out instantly in a crowd because their life trajectory has a distinct "sharpness."

Many founders I met in China were of another type, which surprised me.

They are extremely outstanding—top university degrees, resumes from ByteDance or DJI, Nature papers, multiple patents. In the West, these achievements are only for the top technical talents; in China, they are the entry ticket. They also work harder than almost anyone I've met. We had meetings at all hours, non-stop even on weekends, rushing between cities. One founder met with us on the day his wife gave birth.

But independent thinking, rebellious spirit, and a vision from 0 to 1—these were harder to find. The founders' backgrounds are highly similar, pitches are more conservative, and many ideas are upgrades of existing products (impressive V2) rather than truly original bets. Given the massive scale of technical talent China produces, I expected to encounter more people "showing up with ideas I've never heard of."

My interpretation: China's education system cultivates excellence but doesn't leave enough room for deviation. It produces top executors skilled at solving known problems, not the type who "show up with a problem nobody knew existed."

VCs Are Reinforcing This Model

More interestingly, local investors are exacerbating this trend.

The investment logic of most Chinese funds is based on one premise: invest in the best people coming out of ByteDance or DJI. They look at resumes, not edge; background, not conviction. The VCs' own profiles are similar—coming from big companies, consulting, or investment banking, much like European VCs a decade ago.

Ironically, historically, the Chinese founders who truly built great companies mostly never worked in big companies. Jack Ma was an English teacher who took the college entrance exam twice. Ren Zhengfei founded Huawei at 43, previously being in the military. Liu Qiangdong started by selling goods at a market stall. Wang Xing dropped out of his PhD to start a business. More recently, Liang Wenfeng, who created DeepSeek, never worked anywhere outside his own company. These people are outliers, those without "standard resumes"—precisely the ones the current investment system would miss.

Finding these people offers real alpha, but currently, few seem to be looking there.

Shenzhen and the Hardware Ecosystem

The most shocking thing I saw in China wasn't some startup's pitch.

It was Shenzhen's hardware underground workshops—engineers systematically obtaining high-end Western products, disassembling them part by part, and reverse-engineering everything in an extremely rigorous way. Walking out, I was genuinely unsure if most Western hardware founders understand what they're competing against. The network effects here aren't theoretical; they are physical, dense, and built up over decades.

The entrepreneurs we met confirmed this with data: over 70% of hardware investment comes from the Greater Bay Area, close to 100% from within China—this means iteration cycles are something Western hardware companies simply cannot match.

Most founders I met are using DJI's playbook: make consumer hardware in a niche—electric wheelchairs, lawn mowing robots, new-generation fitness equipment—grow revenue to 8 or 9 figures (USD), then leverage the customer base or underlying technology to move into adjacent categories. Some companies are already much larger than you think. The strongest company I saw on this trip was Bambu Lab, a 3D printing company most Westerners haven't heard of, reportedly with annual profits of $500 million, doubling every year.

Bearish on Chinese Software

I left more skeptical about Chinese software opportunities than when I arrived.

At the model level, China's open source is indeed strong, but closed-source models still have a noticeable gap compared to the best in the West, and the gap might be widening. The capital expenditure gap is huge. GPU access is still restricted. Western labs are increasingly cracking down on distillation. The revenue numbers say it all: Anthropic reportedly did $6 billion ARR in February alone. The best Chinese model companies have ARR in the tens of millions of dollars.

On the software startup side, the mainstream profile is PMs and researchers from ByteDance, making agentic or ambient consumer software for Western markets. The talent is indeed strong, but many of these products fall right within the feature set that big labs will natively release—one update could render them obsolete. Another thing that surprised me: China lacks large, fast-growing private software companies. In the West, besides model companies, there is a batch of startups already doing 9-figure or even 10-figure ARR with astonishing growth—Cursor, Loveable, ElevenLabs, Harvey, Glean. This tier of breakthrough private software companies basically doesn't exist in China—exceptions like HeyGen, Manus, GenSpark, who left after succeeding.

Valuation Bubble

Despite the weak software side, the bubble is real—both early and late stage.

Early on, the very top talent from ByteDance, DeepSeek, and Moonshot AI is indeed significantly cheaper than equivalent US talent, but median valuations have converged. Pre-product consumer startups valued at $100-200 million are common. Pre-seed rounds over $30 million are not unheard of.

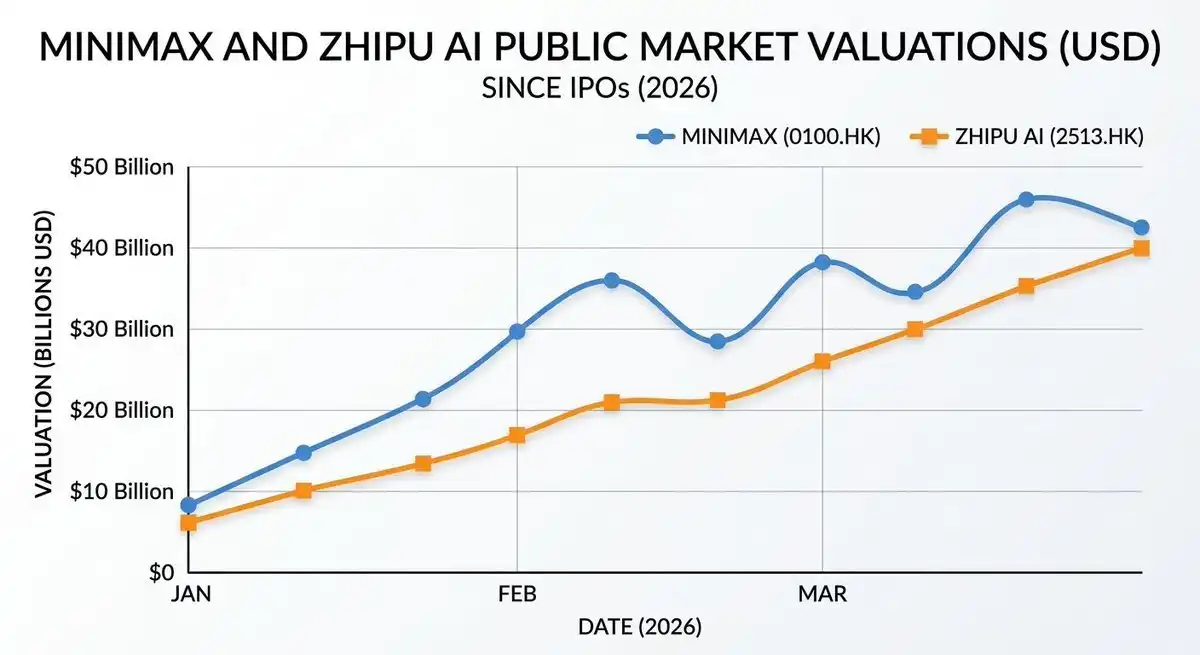

The late-stage numbers are harder to justify. MiniMax is valued at around $40 billion on the public market, with ARR under $100 million—roughly 400x revenue. Zhipu is around $25 billion for $50 million revenue. For comparison: OpenAI's highest valuation round was roughly 66x ARR, Anthropic around 61x.

Private model companies like Moonshot AI use these public market comps to fundraise—jumping from $6 billion to $10 billion to $18 billion within months. Friends in crypto will be familiar with this playbook: investors compare private valuations to a public market price "pre-unlock." Furthermore, Zhipu and MiniMax can maintain these levels partly because they are currently the only way to get exposure to the "China AI narrative," which itself carries a premium. But as more companies list, this premium will dilute. Finally, IPO windows have a characteristic—they slam shut without warning. No one can guarantee you'll close this arbitrage before the comps move.

The humanoid robotics sector is in a similar situation. China has about 200 humanoid robotics companies, around 20 have raised over $100 million, several are valued in the billions—almost all with no revenue, most planning HK IPOs in 2026 or 2027. If this market is real, China's hardware advantage makes the long-term landscape relatively clear. But commercialization might be much slower than the current funding pace suggests, and I doubt the HK market can support the dozens of multi-billion dollar humanoid robotics companies currently queuing for IPO. I'm staying away for now.

Notable Information Asymmetry

One thing took me by surprise: almost every founder I met is targeting the global market first, then China. They use Claude Code, listen to Dwarkesh's podcasts, and know the San Francisco startup ecosystem inside out—often more than Western investors who haven't been keeping up.

Western hostility towards China is noticeably greater than Chinese hostility towards the West. Chinese founders see no contradiction in combining China's engineering execution and hardware depth with Western go-to-market and product thinking. When this combination comes together in the right founding team, it can birth some truly remarkable companies.

Finding these founders—those who don't fit the "standard resume template" optimized by the local VC system—is what we are doing now.

Special thanks to @woutergort for opening up his excellent Chinese network, @PonderingDurian for organizing the trip, and Claude for patiently editing my ramblings on the plane.