DeFi regulation is back in the headlines as the crypto industry and Wall Street disagree on the proposed ‘innovation exemption’ for tokenized assets.

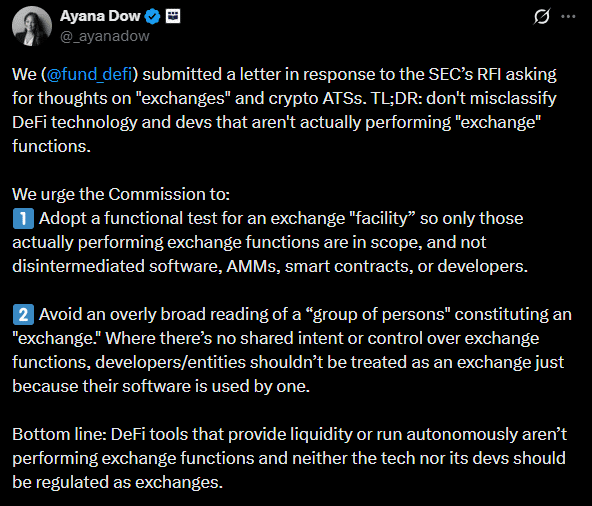

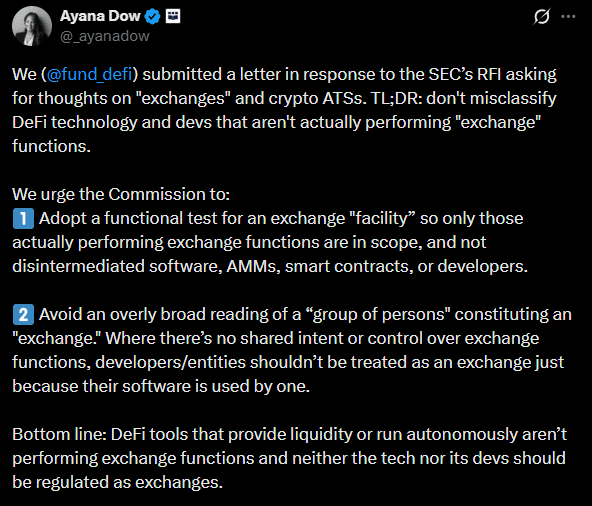

On the 1st of April, a DeFi advocacy group, the DeFi Education Fund (DEF), wrote to the SEC arguing that decentralized protocols should not be ‘misclassified as intermediaries’ like centralized traditional exchanges.

Ayan Dow, legal officer at DEF, added,

DeFi tools that provide liquidity or run autonomously aren’t performing exchange functions, and neither the tech nor its devs should be regulated as exchanges.

According to the advocacy group, any non-custodial application does not fall within the legal definition of an intermediary or exchange. Additionally, classifying developers as intermediaries, yet they don’t control the ‘non-custodial platforms’ they’ve built, would place an overwhelming regulatory burden on them.

As such, the advocacy group pressed that any suggested DeFi regulation scope should exclude disintermediated software, automated market makers (AMMs), smart contracts, and non-controlling developers.

Wall Street opposes DeFi legal exemption

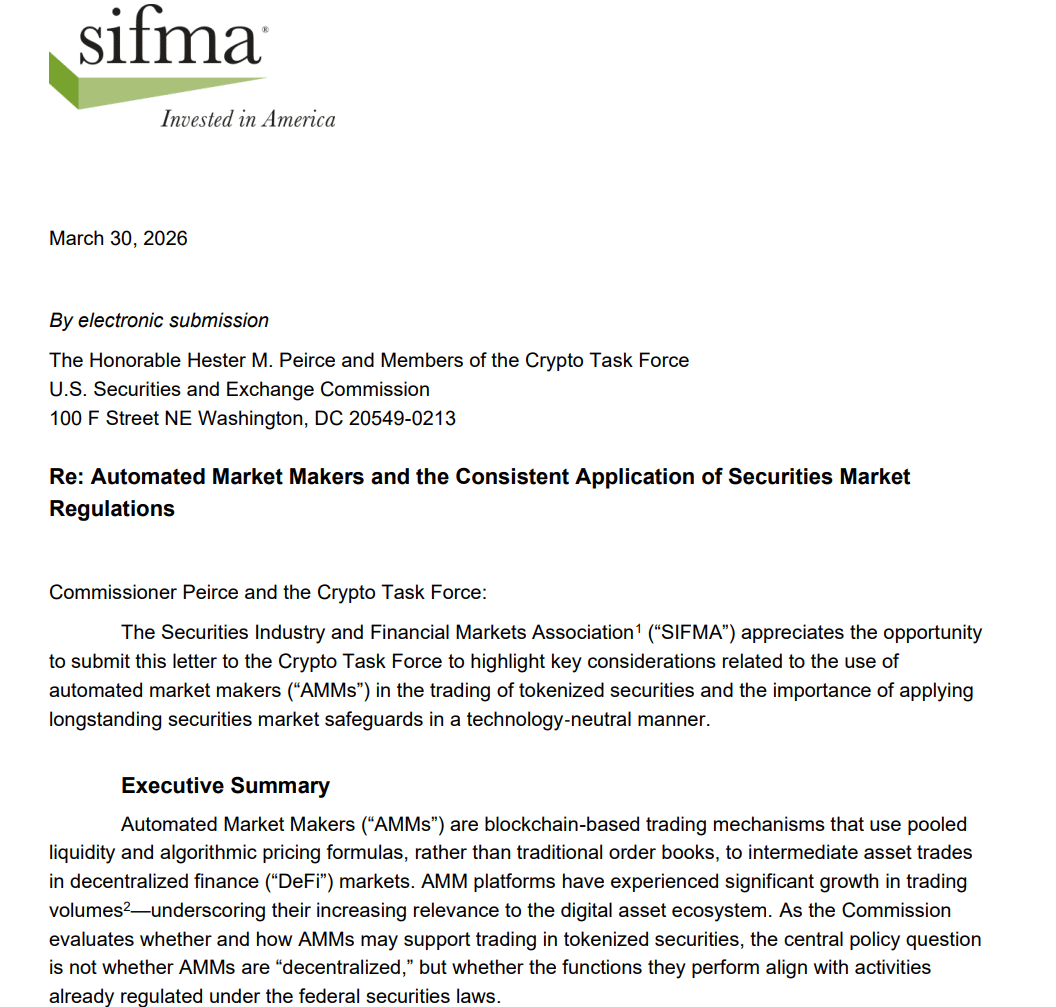

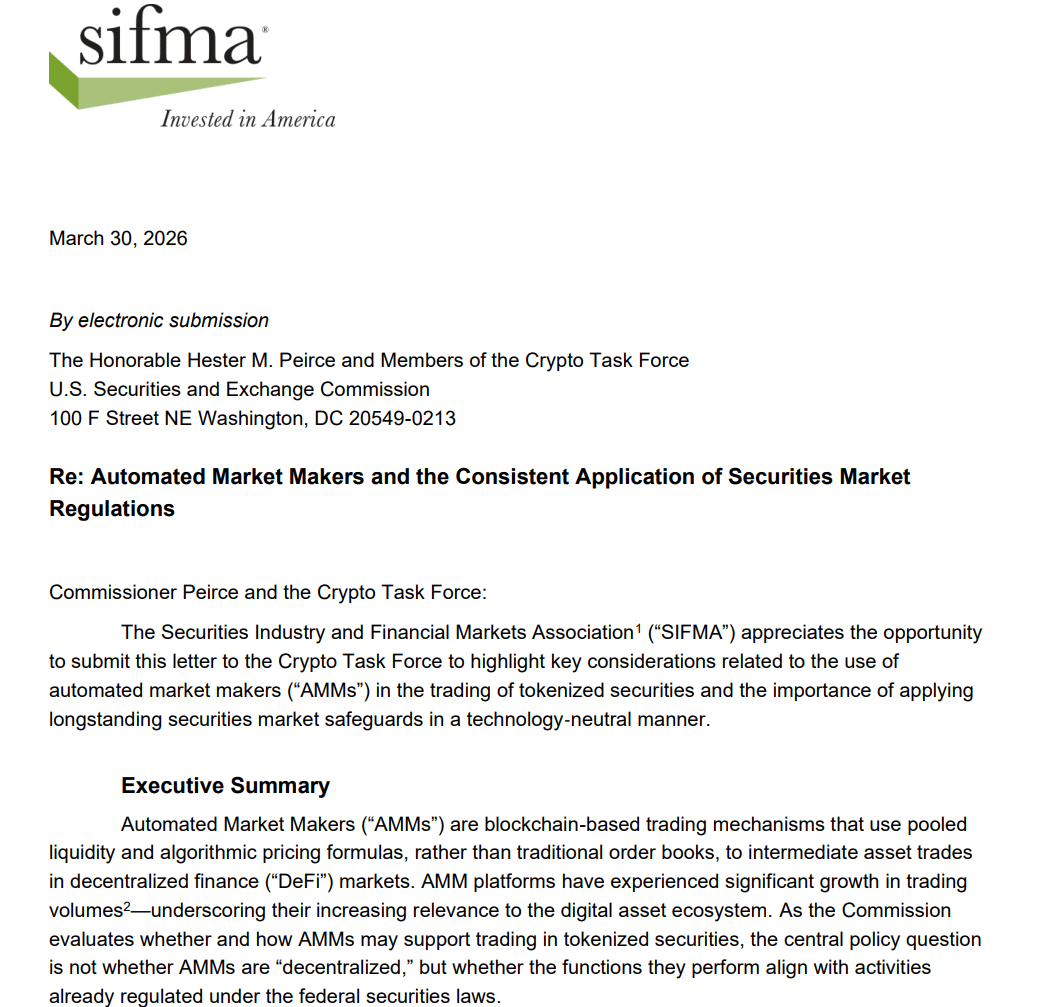

The DEF letter was also a response to SIFMA (Securities Industry and Financial Markets Association). The TradFi umbrella group recently argued that the SEC should regulate AMMs, citing risk to investor protections.

According to SIFMA, the SEC should regulate AMMs and DeFi platforms based on their functions in supporting tokenized securities trading. And not based on whether they’re decentralized, as DeFi supporters propose.

SIFMA believes the Commission should maintain technology neutrality by regulating AMMs based on their market function rather than protocol architecture.

SIFMA’s stance echoed Citadel Securities’ position. Last year, Citadel called for a strict regulation of DeFi platforms that handle tokenized securities.

SIFMA and Citadel’s opposition to unregulated DeFi could be genuine concerns, given the scams and blowouts seen in the past across the sector. For Wall Street, compliance should apply to everyone handling tokenized securities.

However, Citadel gets most of its revenue from being a centralized intermediary, especially for retail platforms like Robinhood. As a result, DEF views the Wall Street opposition as motivated by the potential disruption of DeFi tech (removing intermediaries) to its business interests.

It remains to be seen how the SEC will address these competing interests while still supporting innovation in the upcoming ‘exemption’ framework for tokenized securities.

Final Summary

- Advocacy group DeFi Education Fund (DEF) has opposed SIFMA’s push to regulate AMMs and other non-custodial DeFi platforms

- However, SIFMA claims most ‘decentralized’ platforms pose investor protection risks.