The development of every disruptive fintech inevitably goes through growing pains, and Decentralized Finance (DeFi) is no exception. The early lending markets launched rapidly and expanded aggressively. The industry faced successive security attacks in the public market, then gradually improved code security, collateral asset risk control, oracle mechanisms, liquidation logic, and governance systems.

Past risk cases have reference value but can no longer represent today's mature DeFi ecosystem. After all, those who only look backward often miss current opportunities.

Excluding cross-chain bridge-related security incidents, the current estimated annualized loss rate of funds from theft and malicious attacks for DeFi lending businesses on Ethereum Virtual Machine (EVM) and Solana chains is about 0.03% of the Total Value Locked (TVL). The data for this analysis is aggregated from hack and exploit events flagged on the DeFi Llama platform.

The core criterion for judging security risk is: How large is the actual loss from exploits relative to the amount of capital in the market?

A loss rate of 0.03% roughly equates to the probability of accidental slip-and-fall deaths among the American public. This shows that, setting aside the market's prevalent panic, the actual security risk of DeFi lending businesses is relatively low.

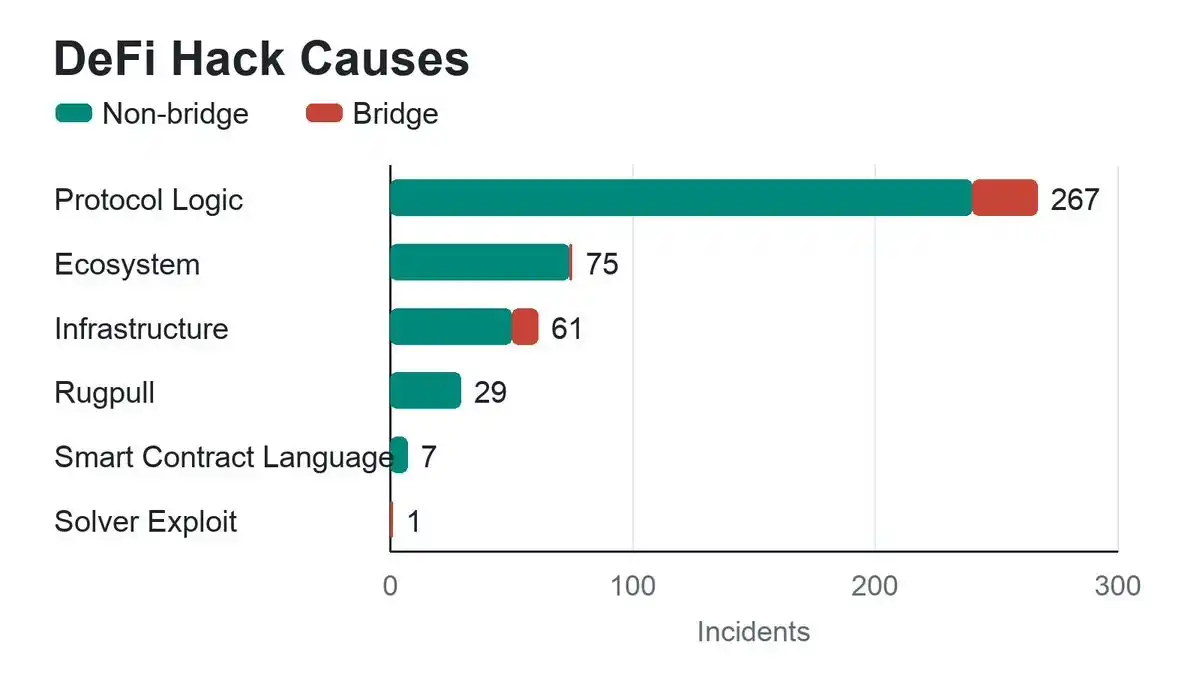

Breakdown of DeFi Security Incidents

As of May 16, 2026, the total amount stolen from all categories of DeFi protocols, according to DeFi Llama statistics, reached $7.751 billion. This statistic has a very broad coverage, encompassing cross-chain bridges, decentralized exchanges (DEX), derivatives protocols, blockchain gaming projects, digital wallets, underlying infrastructure failures, and non-lending DeFi businesses.

Cross-chain bridges are the high-risk area: after removing cross-chain bridge-related security incidents, the total stolen loss in the DeFi sector shrinks to $4.518 billion.

Code executes only the instructions it was written to follow, not the developer's ideal expectations, which is the root cause of various vulnerabilities. Proper risk classification is significant: DeFi is not a single, uniformly risky sector. Cross-chain bridge hacks, DEX oracle manipulations, wallet phishing scams, and lending market collateral asset vulnerabilities are all completely different risk types.

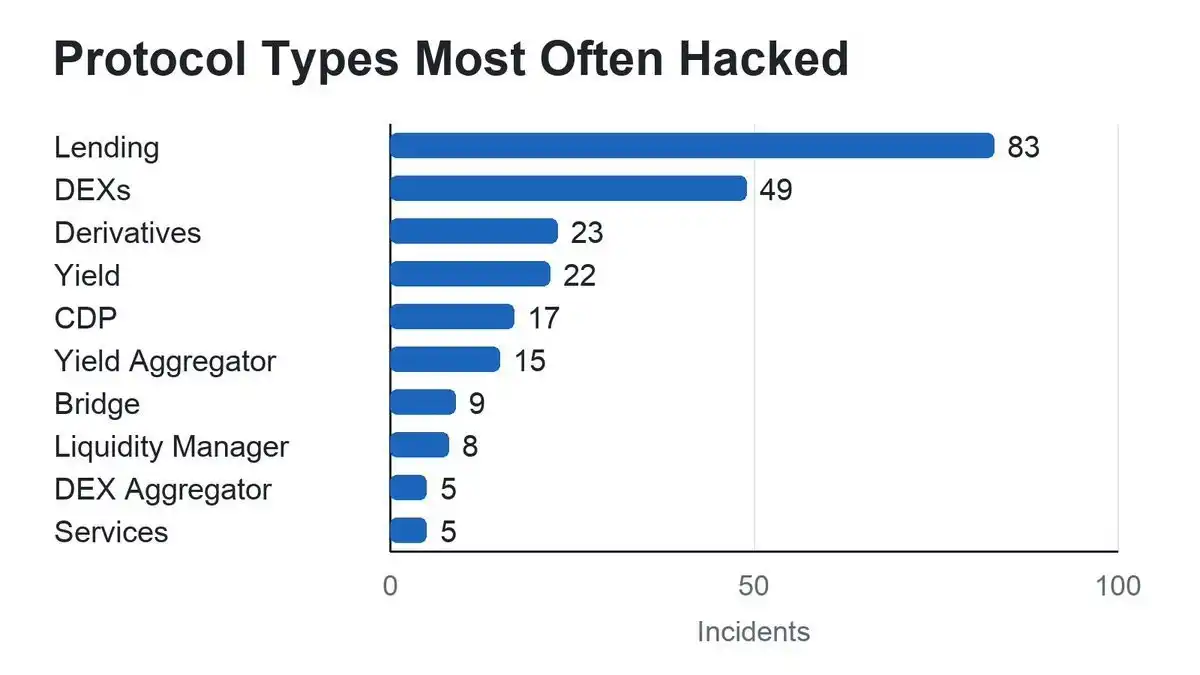

Among all DeFi protocols, lending markets are attacked most frequently, for a very simple reason: large amounts of assets are locked long-term in smart contracts, making them prime targets for hackers.

Lending protocols and Automated Market Makers (AMMs) are high-incidence sectors for security incidents, with the core commonality being the need to pool large amounts of assets into smart contracts. Apart from cross-chain bridges, the vast majority of security incidents are concentrated in these two types of protocols. This article will focus on the lending and money market sector for analysis.

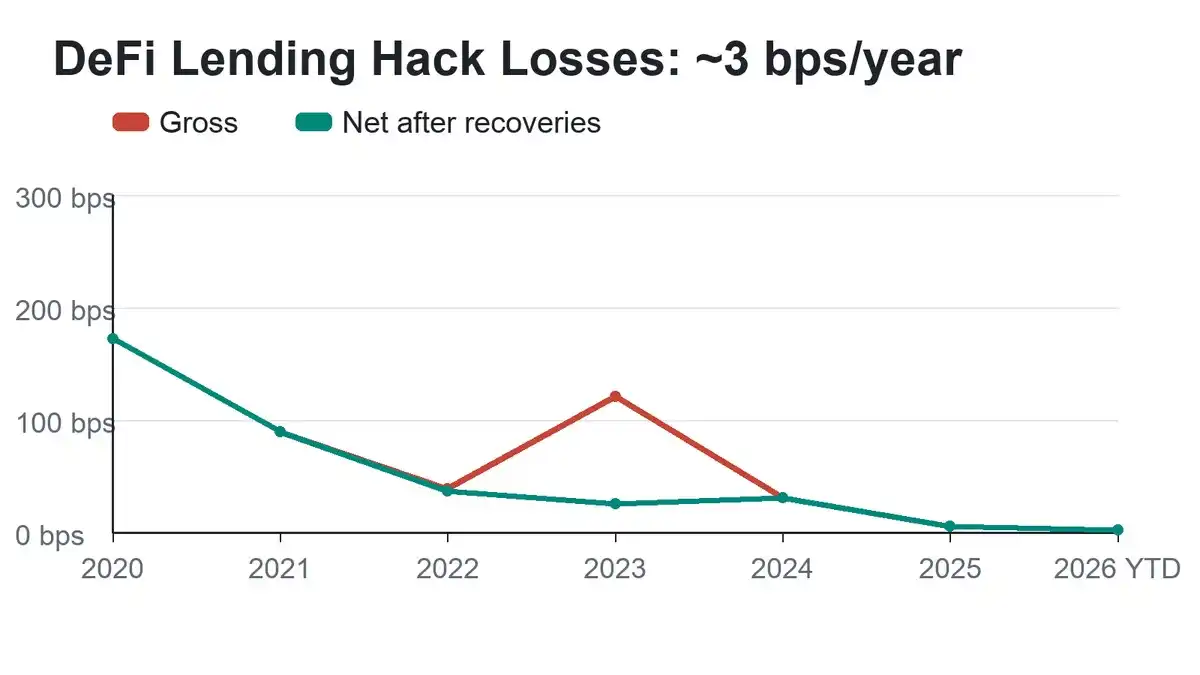

Fund Loss Rate Has Greatly Improved

Today's overall DeFi locked volume is far higher than during the early days of frequent vulnerabilities, especially in the lending sector, where project risk control systems are more mature, code audits are more comprehensive, and real-time global risk monitoring is increasingly robust. Excluding cross-chain bridge incidents, the annualized actual stolen loss ratio for lending businesses in the EVM and Solana ecosystems has significantly declined.

Euler even set a classic risk management case by successfully recovering all stolen assets. The $197 million hack of Euler in 2023 not only saw full recovery but also resulted in a $240 million repatriation due to asset price fluctuations, achieving a positive surplus. This opened the gap between industry book losses and actual recovered amounts.

Taking May 16, 2026, as the cut-off date, statistics from the past year show:

· Total book loss from theft in non-cross-chain lending businesses on EVM and Solana: $30.9 million

· Actual net loss after deducting asset recoveries: $30.1 million

· Average daily locked capital in the lending sector: $99.6 billion

· Book fund loss rate: 3.1 basis points

· Actual net loss rate: 3 basis points

Converted, the annual fund loss remains stable at around 0.03% of the total lending TVL.

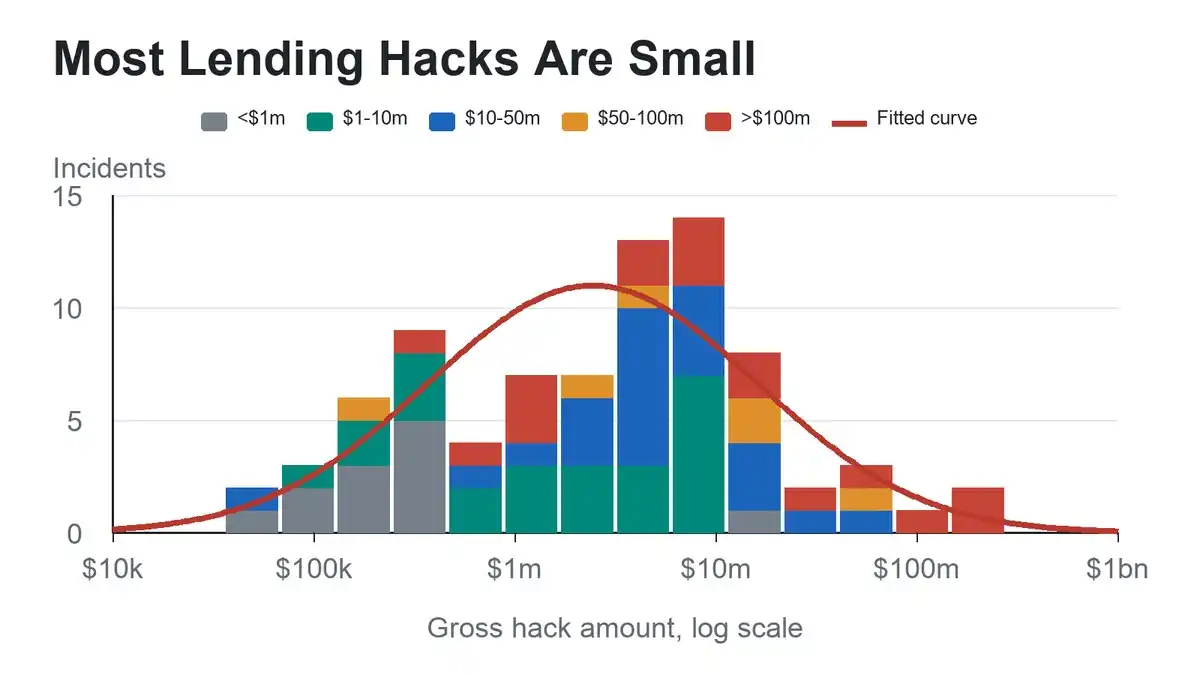

The Advantage of Asset Diversification

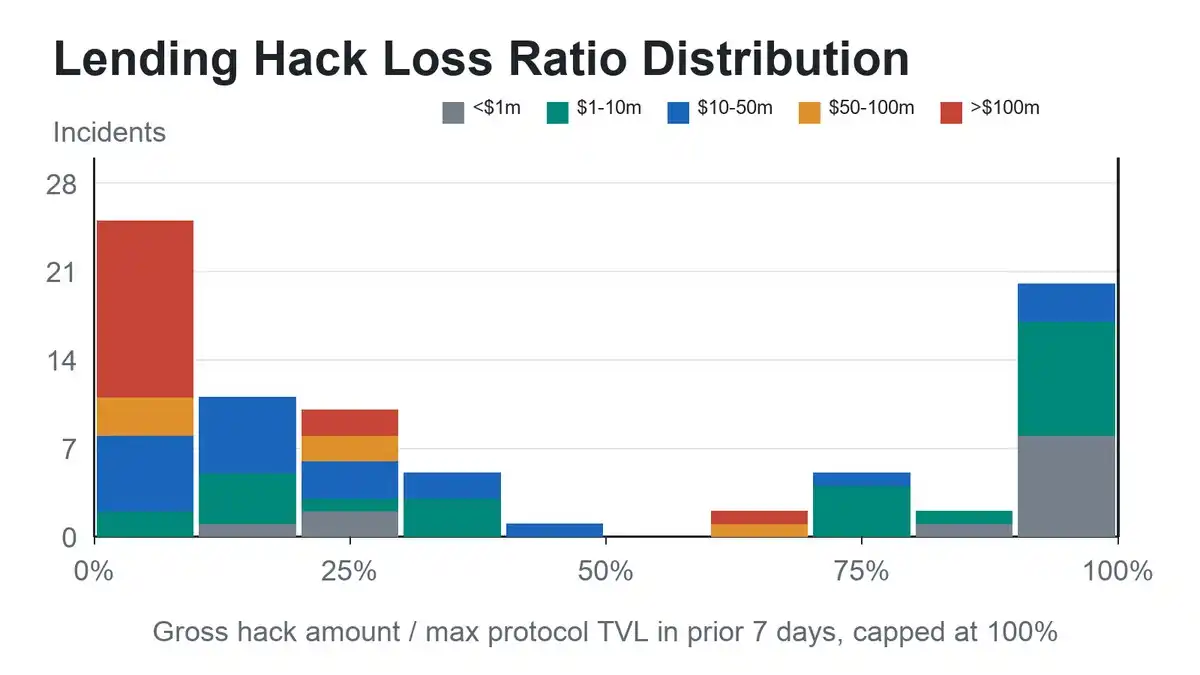

DeFi security incidents show a clear polarization characteristic: a very small number of extremely large thefts account for the vast majority of the industry's publicly reported total losses. Plotting incident size on a logarithmic scale reveals that the scale of various theft events roughly follows a log-normal distribution. Intuitively, the losses caused by the vast majority of security incidents are relatively small, with high-value mega-thefts concentrated in only a few extreme cases.

Although ChatGPT has raised differing views, I believe this data strongly demonstrates that portfolio diversification is an excellent method for crime prevention.

From the perspective of risk transfer and commercial insurance, this data model also provides reasonable support for the industry's security insurance business. Insurance institutions can set single-claim payout limits for different protocols to carry out underwriting business in an orderly manner.

Furthermore, the vast majority of theft incidents have limited impact, far from enough to shake the entire capital base of the lending sector. And the larger the overall sector volume, the smaller the impact of a single security event on the whole.

Note: In some theft incidents, the loss amount appears to exceed the project's own TVL. Such cases are uniformly counted as 100% loss.

There are two main reasons for this data discrepancy: first, a time lag exists between the TVL snapshot and the security incident, during which asset volume changed; second, DeFi Llama's TVL statistical scope is inconsistent with the actual assets at risk.

Although this measurement method is not absolutely perfect, it is sufficient to clearly reflect the industry's status quo: the vast majority of exploit attacks only affect a single business module within a lending protocol, with full asset compromise being extremely rare, especially for large, top-tier projects. This research data also provides a key basis for DeFi industry risk hedging and secure asset custody services.

Asset Recovery Capability is Crucial

Asset recovery has also significantly improved the actual risk profile of the DeFi lending sector.

Looking at the all-category DeFi theft data from DeFi Llama, the overall industry asset recovery amount accounts for about 8% of the total book loss; after excluding cross-chain bridge incidents, the asset recovery ratio is higher in the EVM and Solana lending sectors, reaching about 20% of the book loss.

Asset recovery success rates are generally higher for theft cases occurring in regions with well-developed legal systems and mature regulatory governance. This phenomenon also hints at industry implications related to access permissions.

Positive Industry Outlook

Today, the security risks of the DeFi lending sector have become quantifiable and classifiable, with the actual fund loss ratio continuing to decline. Data proves the industry has entered a mature development stage: the actual loss from exploit theft is extremely low relative to the sector's massive capital stock, various risks are clearly distinguishable, and risk boundaries are increasingly transparent.

In conclusion, there's no need to be swayed by external pessimistic narratives. Data and facts are enough to confirm the true risk level of the DeFi lending sector.