So far, the 2026 cycle has been a bear market.

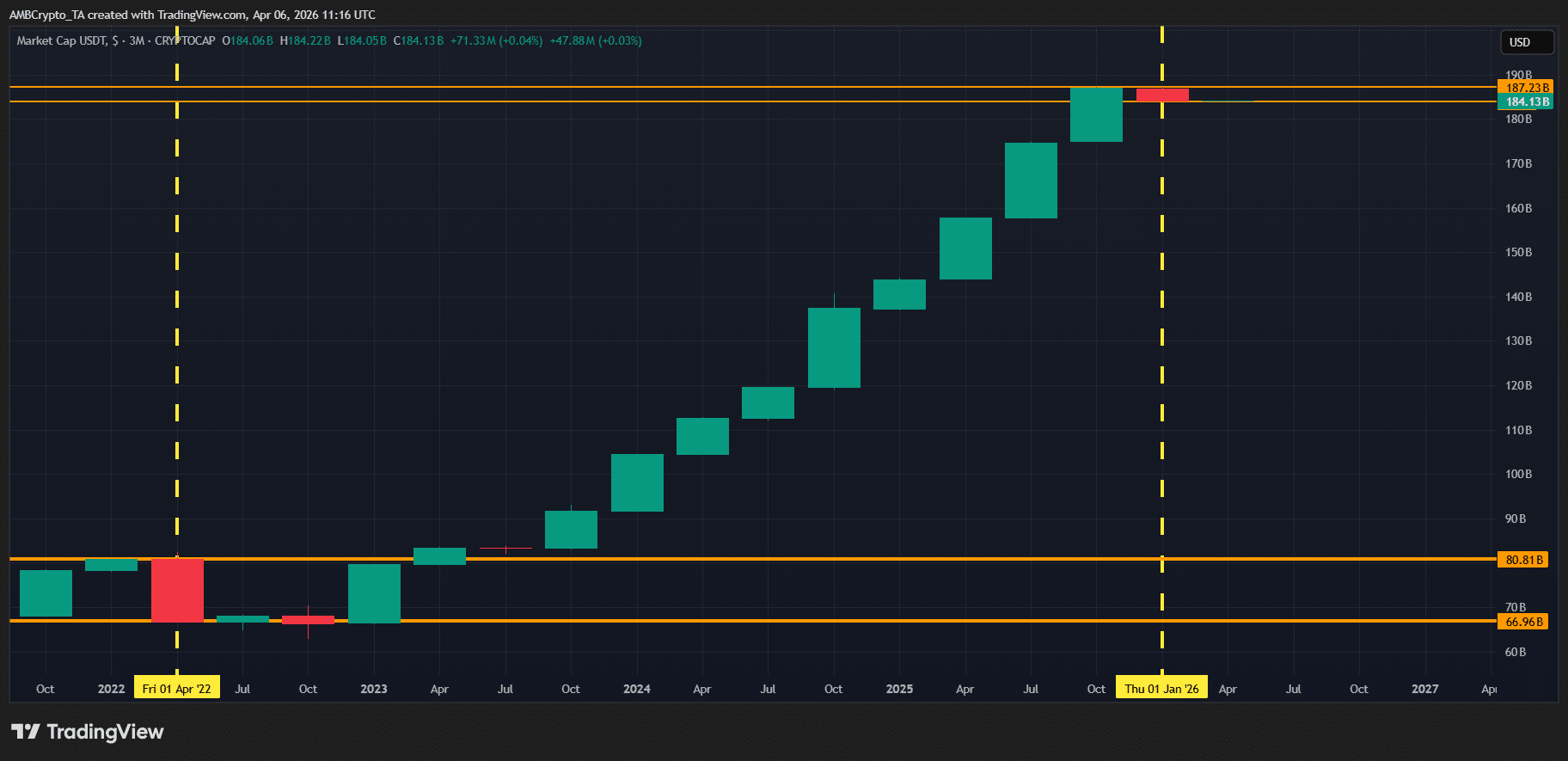

Notably, one clear signal is when stablecoin market caps drop alongside crypto prices. In Q1, USDT fell 1.6%, showing that money was leaving crypto instead of sitting on the sidelines like it would in a bull market, where investors hold dry powder for the next risk-on move.

The result? The total crypto market dropped 20.8% over the same period, confirming the bearish trend.

Investors weren’t chasing dips. Instead, they were exiting. TOTAL2 (market cap ex-BTC) fell 19.17%, meaning capital didn’t rotate into altcoins either, which only adds to the bearish picture.

In essence, stablecoins played a central role in defining crypto’s Q1 trend.

According to AMBCrypto, this is where the recent 10x Research report becomes relevant.

It highlights that USDT issuance on Ethereum [ETH] has recently outpaced Tron [TRX], with a near 2.6% monthly jump in volume on ETH. That closes the gap with TRX, which is now just 1% higher, signaling that liquidity is starting to flow into high-cap networks, consistent with the total crypto market cap rising 1.6% so far in April.

From a technical standpoint, this combination of rising market cap and stablecoin inflows is significant.

When stablecoins move back into major networks, it suggests that investors are redeploying capital. This kind of flow often forms a base for price support, and we’re already seeing it in action.

ETH has rallied 1.87% from its $2.1k open, reinforcing that this setup is gaining traction.

Naturally, the question arises: With stablecoins back in play, could this momentum be laying the foundation for a broader Q2 rally, potentially reversing the bearish trend from Q1?

Stablecoin flows hit major networks, market eyes potential rally base

Apart from serving as a hedge or a bridge, stablecoins often act as an early signal for market activity.

A striking example is the recent activity around Solana [SOL].

Circle minted $3.25 billion USDC on Solana in just 7 days, the largest weekly issuance of 2026. This sudden influx of liquidity into the network naturally raises questions about investor intent and market positioning.

But it doesn’t stop there.

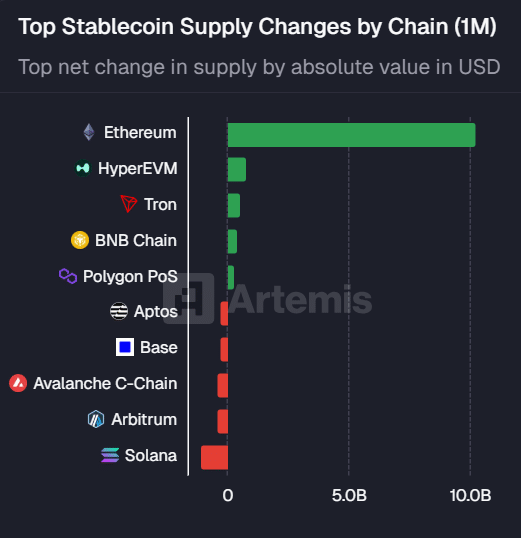

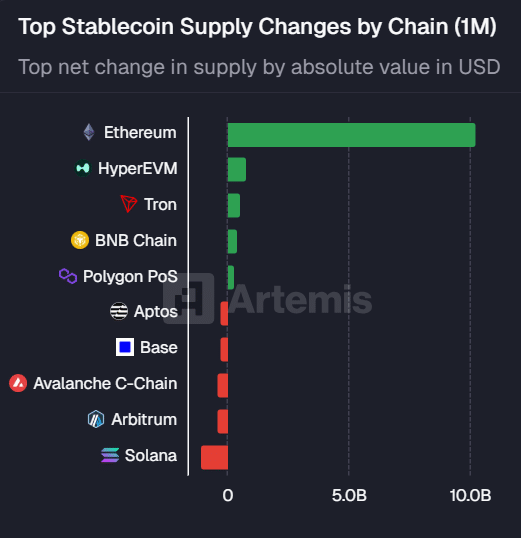

According to Artemis Terminal, monthly stablecoin supply changes on Ethereum have reached a staggering $10.3 billion, the largest among all L1 networks. This “coordinated” increase in stablecoin supply across major networks suggests that investors are actively redeploying capital.

Consequently, the critical question now becomes: Do these issuers have insight into opportunities or risks that the broader market hasn’t priced in yet?

According to the 10x Research report, Ethereum’s relative undervaluation appears to be driving much of this influx.

From a technical standpoint, Ethereum has dropped 57% from its August 2025 peak, making it look relatively cheap, especially when compared to Bitcoin, which is down roughly 42% over the same period.

This is particularly significant given that BTC dominance continues to face resistance around 60%.

Adding to this, Wall Street’s integration into DeFi is gaining momentum, bringing institutional capital to the market.

Taken together, these factors suggest that Ethereum and other high-cap L1s may be positioning for early Q2 momentum, with stablecoin flows acting as a leading indicator of where capital may move next.

Final Summary

- Rising USDT issuance on ETH and large USDC minting on SOL indicate capital is redeploying.

- With ETH down 57%, BTC dominance under pressure, and Wall Street entering DeFi, stablecoin inflows may act as a leading indicator for Q2 momentum.