* Key Change in 2025: Pricing Framework 'Externalization'. No longer primarily driven by a single public chain cycle/narrative self-loop, but instead dominated by policy and compliance + macro liquidity/risk appetite + leverage and risk control; price elasticity depends on which entry points funds come from, what assets they buy, and how they exit under pressure.

* Fund entry points shift from a 'single on-chain leverage channel' to multiple parallel channels: ETF (standardized allocation) + stablecoin dollar base (on-chain settlement/circulation) + DAT (public company financing capacity → spot demand function) + listing path (IPO) (mapping capabilities like licensing/custody/clearing/institutional services into buyable stock cash flows).

* Industry internal evolution: Shifting from 'narrative-driven' to 'product line-driven'—stablecoin layering (cash layer vs. yield-efficient tools, the latter more cyclical), on-chain perpetuals becoming infrastructural and moving towards market share battles, prediction markets expanding from crypto-native to event contract markets; industry rhythm becomes more coupled with macro/political variables.

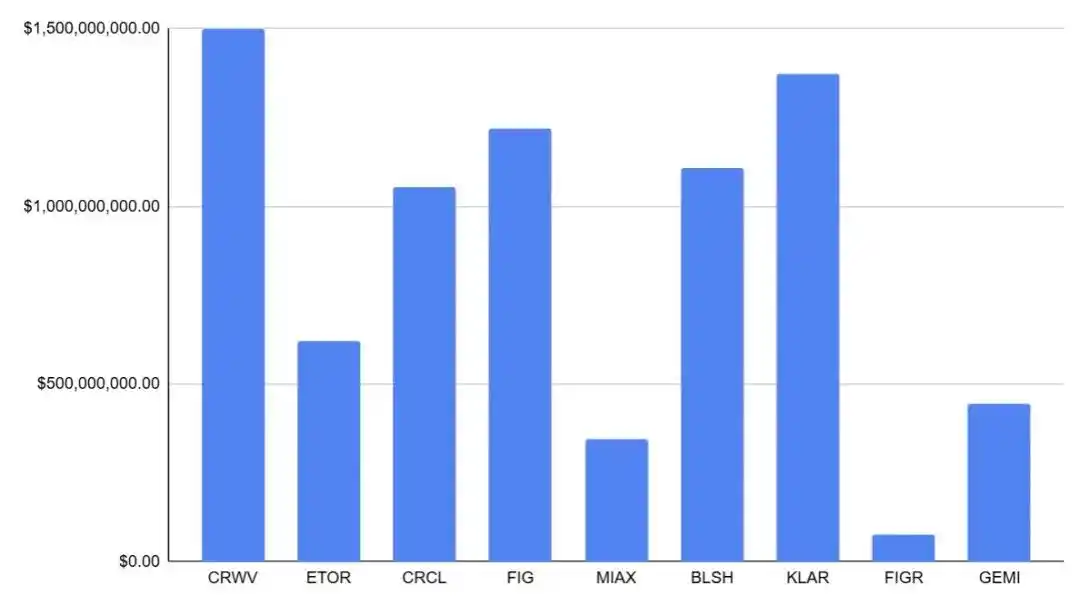

* Listing path/IPO: 9 crypto/related companies completed IPOs in 2025, raising a total of ~$7.74 billion; valuations ranging from ~$1.8 billion to $23 billion; initial float ~7.6%–26.5%.

* Potential 2026 IPO candidates: Anchorage Digital, Upbit, OKX, Securitize, Kraken, Ledger, BitGo, Tether, Polymarket, Consensus (approx. 10 companies).

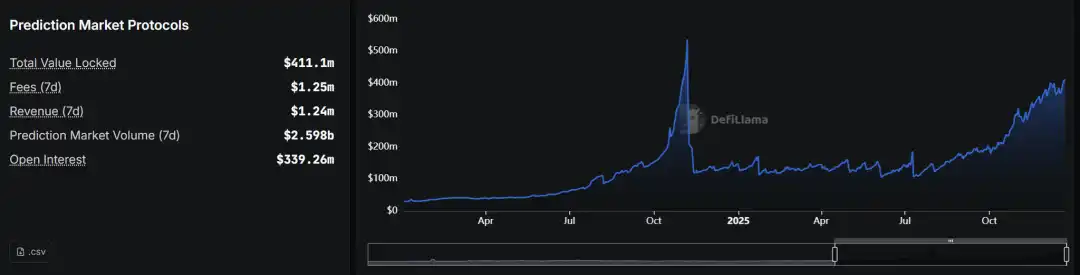

* Observable fund entry points: Total stablecoin supply ~$205B → ~$300B+ (structure: USDT ~$186.7B, USDC ~$77B); IBIT net inflows YTD ~$25.4B; DAT adoption by hundreds of companies, combined holdings in the hundreds of billions USD; on-chain perpetuals 30-day volume ~$1.081T, OI ~$15.4B; prediction market 2025 full-year volume ~$44B; USDe ~$15B → ~$8.5B → ~$6–7B.

The main theme of the crypto market in 2025 no longer revolves around the technological cycle of a single public chain or the self-loop of on-chain narratives, but enters a deeper stage dominated by 'external variable pricing and financial entry competition'. Policy and compliance frameworks determine the access boundaries for long-term capital, macro liquidity and risk appetite determine whether trends can continue, and derivative leverage and platform risk control mechanisms reshape volatility patterns and drawdown speeds at key junctures. More importantly, a main theme repeatedly validated by the market starting in 2025 is: what determines price elasticity is no longer just the 'strength of on-chain narratives', but rather which entry points funds use to enter, what investable assets they land on, and how they exit under pressure. External variables and internal evolution jointly drove the transformation of the crypto industry in 2025, further solidifying two clear paths for the future development of the crypto industry.

Institutionalization Acceleration and Securitization Breakthrough: The Period of External Variable Dominance in the 2025 Crypto Market

'Financialization' underwent a structural shift in 2025. The ways funds enter are no longer limited to native on-chain leverage but have differentiated into multiple parallel, clearly layered channels. Crypto allocation expanded from a single 'asset exposure (spot/ETF)' to a dual-line structure of 'asset exposure + industrial equity'. Market pricing also shifted from a single-axis drive of 'narrative - positioning - leverage' to a comprehensive framework of 'institution - fund flows - financing capacity - risk transmission'.

On one hand, standardized products (like ETFs) incorporate crypto assets into the risk budget and passive allocation framework of investment portfolios; stablecoin supply expansion solidifies the on-chain dollar settlement base, enhancing the market's endogenous settlement and circulation capacity; corporate treasury (DAT) strategies directly map the financing capacity and balance sheet expansion of public companies into a spot demand function. On the other hand, crypto companies use IPOs to 'securitize' capabilities like licensing, custody, trading clearance, and institutional services into public company stocks, allowing institutional funds for the first time to use familiar methods to buy into the cash flows and compliance moats of crypto financial infrastructure, and introducing a more comparable benchmarking system and exit mechanism.

IPOs play the role of 'buying the industry, buying cash flows, buying compliance capabilities' in the fund structure. This path was rapidly established in 2025, becoming one of the preferred choices for leading crypto companies and an external variable for the crypto industry.

In the 5 years prior, this path was not clear, not because public markets formally closed to crypto companies, but because IPOs were practically in a state of 'high threshold, difficult pricing, difficult underwriting' for a long time:

On one hand, unclear regulatory stance combined with high-intensity enforcement meant core businesses like trading, brokerage, custody, and issuance had to endure higher density legal uncertainty disclosures and risk discounts in prospectuses (e.g., the SEC sued Coinbase in 2023, accusing it of operating as an unregistered exchange/broker/clearing agency, reinforcing the uncertainty that 'the nature of the business might be determined retroactively').

On the other hand, stricter accounting and audit standards for custody businesses regarding capital and liability presentation also increased compliance costs and institutional cooperation barriers (e.g., SAB 121 imposed stricter asset/liability presentation requirements for 'custodying crypto assets for clients', widely seen by the market as significantly increasing the asset burden and audit friction for financial institutions engaging in crypto custody).

Simultaneously, industry credit shocks combined with macro tightening led to a contraction in the overall US IPO window, causing many projects that might have leveraged public markets to postpone or change course (e.g., Circle terminated its SPAC merger in 2022, Bullish called off its SPAC listing plan in 2022). More critically, from a primary market perspective, these uncertainties were amplified into real 'underwriting friction': underwriters needed to pass internal compliance and risk committees during the project initiation phase, conducting stress tests on whether business boundaries might be retroactively defined, whether key revenues might be reclassified, whether custody and client asset segregation introduced additional balance sheet burdens, and whether potential enforcement/litigation triggered major disclosure and indemnification risks; once these issues were difficult to explain standardly, it led to significantly higher due diligence and legal costs, longer prospectus risk factors, unstable order quality, ultimately reflected in more conservative valuation ranges and higher risk discounts. For issuing companies, this directly changed strategic choices: rather than pushing forward reluctantly in an environment with 'high explanation costs, suppressed pricing, uncontrollable post-listing volatility', it was better to delay issuance, turn to private financing, or seek M&A/other paths. The above collectively determined: at that stage, IPO was more like a 'choice question' for a few companies, not a sustainable financing and pricing mechanism.

The key change in 2025 was that the above resistance saw clearer 'removal/easing', making the listing path regain continuous expectations. One of the most representative signals was the SEC issuing SAB 122 and rescinding SAB 121 in January 2025 (effective that month), directly removing the most controversial, most 'asset-heavy' accounting obstacle for institutions participating in custody and related businesses, improving the scalability of the bank/custody chain, and reducing the structural burden and uncertainty discount for related companies at the prospectus level. Around the same time, the SEC established a crypto asset working group and signaled progress towards a clearer regulatory framework, reducing the premium for uncertainty about 'whether rules will change, will they be retroactive' at the expectation level; mid-year legislative progress in the stablecoin area further provided 'framework-level' certainty, making key links like stablecoins, clearing, and institutional services easier for traditional capital to incorporate into valuation systems in an auditable, comparable way.

These changes quickly transmitted along the primary market execution chain: for underwriters, it became easier to transition from 'unexplainable, unpricable' to 'disclosable, measurable, comparable' compliance conditions—able to be written into the prospectus, able to be benchmarked horizontally by buyers, making underwriting teams more likely to give valuation ranges, control issuance pace, and invest in research coverage and distribution resources. For issuing companies, this meant IPO was no longer just a 'financing action', but a process of engineering revenue quality, client asset protection, internal controls, and governance structure into 'investable assets'. Furthermore, although the US market doesn't have a formal 'cornerstone investor' system like Hong Kong, anchor orders and long-term accounts (large mutual funds, sovereign wealth, some crossover funds) during bookbuilding functionally play a similar role: when regulatory and accounting friction ease and industry credit risks are cleared, high-quality demand is more likely to return to the order book, helping pricing become more stable, issuance more continuous, thus making IPO more likely to return from an 'occasional window' to a 'sustainable financing and pricing mechanism'.

Ultimately, marginal improvements in policy and accounting standards are specifically mapped onto the rhythm and fund flow of the annual行情 through the primary market and capital allocation chain. Looking at the annual unfolding of 2025, the above structural changes became visibly apparent in a relay fashion.

Early 2025, regulatory discount convergence drove a re-rating of institutional expectations, with core assets with clearer allocation paths benefiting first; then the market entered a period of反复 confirmation of macro hard boundaries, where interest rate paths and fiscal policy embedded crypto assets deeper into the volatility model of global risk assets (especially US growth stocks). By mid-year, the reflexivity of DAT became more apparent: the number of public companies adopting similar treasury strategies rose to the hundreds, combined holdings reached the hundreds of billions USD level, balance sheet expansion became an important marginal demand source; simultaneously, ETH-related treasury allocations heated up, making the 'balance sheet expansion - spot demand' transmission no longer just about BTC. In Q3 and Q4, against the backdrop of multiple parallel channels and fund rebalancing between different entry points, the valuation中枢 and issuance conditions of public markets began to more directly affect capital allocation in the crypto space: whether issuance was smooth, whether pricing was认可, gradually became a风向标 for measuring 'industrial financing capacity and compliance premium', and indirectly transmitted to spot pricing through fund reallocation between 'buying coins/buying stocks'. As Circle and others provided 'valuation anchors', and more companies advanced listing applications and preparations, IPO evolved from a 'pricing reference' to a core variable affecting the fund structure: ETFs mainly solve the problem of 'can we allocate, how to incorporate into portfolios', while IPOs further solve the problem of 'what to allocate, how to benchmark, how to exit', pushing some funds from the high-turnover on-chain leverage ecosystem towards longer-term industrial equity allocation.

More importantly, this 'entry competition' is not just a theoretical framework, but can be directly observed in fund data and market behavior. As the on-chain dollar settlement base, stablecoin supply scale rose from ~$205B to the $300B range and stabilized near year-end, providing a thicker settlement and liquidity buffer for on-chain交易 expansion and deleveraging processes; ETF fund flows沉淀 as a visible pricing factor, with IBIT achieving ~$25.4B in net inflows YTD despite macro volatility and institutional rebalancing disturbances, increasing the explanatory power of 'net flow/rebalancing rhythm' for price elasticity; the scaling of DAT meant public company balance sheets began to affect spot supply-demand structure directly, potentially strengthening trend expansion during uptrends, but也可能 triggering反向传导 due to valuation premium contraction and financing constraints during downtrends, further coupling traditional capital market volatility with crypto market volatility. Simultaneously, IPOs provided another set of quantitative evidence: 9 crypto/crypto-related companies completed IPOs in 2025, raising a total of ~$7.74B, indicating the public market financing window not only exists but has real承载 capacity.

In this context, IPO became an 'external structural variable' for the 2025 crypto market: on one hand, it expanded the range of assets compliant funds could allocate to, providing public market valuation anchors and comparable systems for stablecoins, trading/clearing, brokerage, and custody links, and changing the holding period and exit mechanism of funds through the 'stock' form; but on the other hand, its marginal increment is not linear and is still constrained by macro risk appetite, secondary market valuation中枢, and issuance windows.

Overall, 2025 can be summarized as a combination year of 'institutionalization acceleration, macro constraint strengthening, and securitization restart': institutional and compliance path advancement increased the allocatability of crypto assets, causing fund entry points to expand from a single on-chain structure to a parallel system of ETFs, stablecoin base, DAT, and IPO; simultaneously, interest rates, tariffs, and fiscal friction continuously shaped liquidity boundaries, making the行情 more like 'macro-driven volatility' of traditional risk assets. The resulting track differentiation, and the return of the 'public company vehicle', will form an important prelude to 2026.

IPO Window Warming: From Narrative Premium to Financial Primitive

In 2025, the US IPO window for crypto-related companies明显 warmed up, evolving from a 'theoretically open window' to a set of public market samples that can be quantitatively tested: a total of 9 crypto/crypto-related companies completed IPOs for the year based on sample口径, raising a combined ~$7.74B, indicating the public market's financing承 capacity for 'compliantly accessible digital financial assets' has recovered to a considerable scale, not just symbolic small orders. Valuation-wise, these IPOs covered a range from ~$1.8B to $23B, basically covering stablecoins and digital financial infrastructure, compliant trading platforms and trading/clearing infrastructure, regulated brokerage channels, and on-chain credit/RWA and other key links, giving the industry a trackable, comparable equity asset sample pool; this not only provided valuation anchor points for the 'stablecoin - trading - brokerage - institutional services - on-chain credit/RWA' chain, but also made the market's pricing language for crypto companies migrate more systematically towards a financial institution framework (emphasizing compliance and licensing, risk control and operational resilience, revenue quality and sustainable profits more). In terms of market performance, the 2025 samples普遍 showed the common characteristic of 'strong initial issuance stage, followed by rapid differentiation': the issuance structure of many companies had a relatively tight initial float (approx. 7.6%–26.5% range), making short-term price discovery more elastic when the risk appetite window opened; the secondary market was generally strong on the first day, with some标的 seeing double-digit or even higher re-pricing, and the rest mostly having double-digit positive returns, with many companies continuing their strength in the first week and first month, reflecting that buyers had 'sustained承' for such assets during the window period, not just one-time pricing; but after 1-6 months, differentiation increased significantly, and became more aligned with the traditional risk asset logic of 'macro + quality'—companies more偏向 retail and trading-oriented businesses were more sensitive to risk appetite shifts and retreated faster, while assets more偏向 upstream infrastructure and institutional承 capacity were more likely to obtain sustained re-ratings.

More crucially, the reason why the 'return' of US crypto company IPOs was so热捧 is essentially that it simultaneously satisfied the three things the public market cared about most in a window period: buyable, comparable, exitable.

First, it turned the previously hard-to-access 'cash flows of crypto financial infrastructure' into stock assets that traditional accounts could directly hold, naturally adapting to the compliance and risk control frameworks of long-term funds like mutual funds, pensions, and sovereign wealth;

Second, IPOs gave the industry its first batch of horizontally comparable equity samples for the first time. Buyers no longer had to rely on 'narrative strength/trading volume extrapolation' to guess valuations, but could use the familiar language of financial institutions for stratification—compliance costs and licensing barriers, risk provisions and internal controls governance, customer structure and retention, revenue quality and capital efficiency—when pricing methods became more standardized, buyers were more willing to give higher certainty premiums during the window period;

Third, IPOs partially migrated the exit mechanism from 'on-chain liquidity and sentiment cycles' to 'public market liquidity + market making/research coverage + index and institutional rebalancing', which made funds dare to give stronger order quality during the issuance stage (including more stable long-term demand and anchor orders), thereby in turn strengthening the re-pricing momentum in the initial issuance stage. In other words, the热捧 wasn't solely due to risk appetite, but due to the decline in risk premium brought by 'institutional accessibility': when assets become easier to audit, easier to compare, easier to incorporate into risk budgets, the public market is more willing to pay a premium for them.

Among these, Circle is the most representative case of a 'stablecoin track equity valuation anchor': its IPO was priced at $31, raising ~$1.054B, corresponding to an IPO valuation of ~$6.45B, and the secondary market underwent intense re-pricing during the window—approx. +168.5% on the first day, +243.7% in the first week, +501.9% in the first month, reaching a peak of $298.99 mid-way对应 a maximum gain of ~+864.5%, and even at the half-year sample point it was still approx. +182.1%. The significance of Circle lies not in the 'gain itself', but in it being the first time 'stablecoin' was priced by the market as an auditable, comparable, risk-budget-includable 'financial infrastructure cash flow' in a public equity manner, moving away from its past reliance on on-chain growth narratives: the compliance moat and settlement network effects were no longer just concepts, but were directly reflected in the elevation of the valuation中枢 through issuance pricing and secondary market持续承.同时, Circle also verified the typical 'buying method' of the US market for such assets—when the window opens, small float combined with high-quality buyer demand amplifies price elasticity; but when the window contracts, valuations regress faster to differentiation based on fundamental delivery, cycle sensitivity, and profit quality. This also forms the core reason for our optimism regarding US crypto company IPOs: the public market will not raise valuations indiscriminately, but it will complete stratification faster and more clearly, and once quality assets establish a comparable valuation anchor in the public market, their cost of capital will decrease, their refinancing and M&A currency will be stronger, and the positive cycle of growth and compliance investment will be easier to achieve—this is more important than short-term gains and losses.

Looking ahead to 2026, the market's focus will升级 from 'does the window exist' to 'can subsequent listing projects continue to advance, forming a more continuous issuance rhythm'. Based on current market expectations, potential candidates include Anchorage Digital, Upbit, OKX, Securitize, Kraken, Ledger, BitGo, Tether, Polymarket, Consensus, etc., totaling about 10 companies, covering a more complete industry chain from custody and institutional compliance entry, trading platforms and brokerage channels, stablecoins and settlement base, asset tokenization and compliant issuance infrastructure, to hardware security and new information markets. If these projects can land continuously in the public market and receive relatively stable fund承, its significance will not just be 'a few more financings', but will further standardize the logic of investors buying into crypto companies: more willing to pay a premium for compliance moats, risk control and governance, revenue quality and capital efficiency, while also completing筛选 faster through valuation中枢 and secondary performance during macro headwinds or weakened issuance conditions. Overall, we are optimistic about the directional trend of US crypto company IPOs: 2025 has already verified the public market's承 capacity with quantity, financing scale, and market re-pricing; and if 2026 can continue this trend of 'continuous issuance + stable承', IPOs will resemble a sustainable capital cycle more—further pushing the industry from 'narrative-driven periodic行情' towards 'sustainable public market pricing', and allowing companies truly possessing compliance and cash flow quality to continuously expand their leading advantage under lower capital costs.

Industry Structure and Product Line Formation: Internal Evolution of the Crypto Industry

To judge whether this public market path can continue, and which companies are more likely to be 'bought' by the market, the key is not to repeat 'whether the window exists', but to return to the structural evolution that has already occurred within the industry in 2025: growth drivers are switching from single-point narratives to multiple sustainable product lines, and under macro and regulatory constraints, forming a volatility and differentiation mechanism closer to traditional risk assets—it is precisely within this mechanism that the capital market will decide which business models deserve a more stable valuation中枢 and lower cost of capital.

In 2025, the structural changes within the crypto industry became clearer than ever: market growth is no longer primarily dependent on narrative-driven risk appetite spillovers, but is jointly pulled by several more sustainable 'product lines'—trading infrastructure becomes more professional, application forms closer to mainstream finance, fund entry points more compliant, and gradually forming closed loops across on-chain and off-chain. At the same time, fund behavior and pricing rhythm are also more deeply incorporated into the global risk asset framework: volatility resembles 'risk budget rebalancing under macro windows' more, rather than the relatively independent行情 primarily driven by on-chain narratives and internal liquidity cycles like before. For practitioners, this means the focus of discussion shifts from 'which narrative will explode' to 'which products can stably generate transactions, retain liquidity, and withstand stress tests of macro volatility and regulatory constraints'.

Under this framework, the traditional 'crypto four-year cycle' further weakened in 2025. The cycle logic did not disappear, but its explanatory power was significantly diluted: channels like ETFs, stablecoins, corporate treasuries incorporated larger volumes of funds into an observable, rebalancable asset allocation system; simultaneously, interest rate and dollar liquidity boundaries became harder constraints, making risk budgets, leverage pricing, and deleveraging paths closer to traditional markets. The result is that uptrends rely more on 'macro risk appetite + net inflows' resonance, while downtrends are more easily amplified during 'liquidity tightening + leverage unwinding'. The performance of various tracks throughout the year resembled a coordinated evolution: what truly pushed structural upgrade wasn't single-point narrative explosions, but underlying financialization products like stablecoin expansion, derivative deepening, event contracts continuously thickening fund entry points and trading scenarios, while simultaneously strengthening risk transmission.

Stablecoins presented two simultaneously advancing, but rhythmically unsynchronized, main lines in 2025: one was 'rising compliance certainty', the other was 'cyclical volatility of yield-generating models'. The key to the former is that, as compliance frameworks and more comparable market samples emerged, stablecoin business models became easier for mainstream funds to price based on cash flow and risk attributes; the latter manifested as yield/synthetic dollars being highly sensitive to basis, hedging costs, and risk budgets, showing significant contraction after expansion. Taking Ethena's USDe as an example, its supply approached a high of ~$15B in early October, fell to ~$8.5B附近 in November, and experienced brief de-pegging during the mid-October deleveraging window. The industry-level revelation is: yield stablecoins are closer to 'amplifiers of macro and basis'—contributing liquidity during顺风期, amplifying volatility and risk re-pricing during逆风期.

Trading infrastructure upgrade accelerated in 2025 with on-chain derivatives at the core. Platforms represented by Hyperliquid continued to approach centralized exchanges in terms of depth, matching, capital efficiency, and risk control experience, and reached a monthly trading口径 of ~$300B量级 around mid-year, indicating on-chain derivatives already have the foundation for规模化承. At the same time, new entrants like Aster, Lighter切入 from product structure, fee, and incentive systems, pushing the track from 'single platform红利' towards 'market share competition'. The essence of competition is not short-term trading volume, but whether可用 depth,清算秩序, and stable risk framework can be maintained during extreme行情; and derivative expansion also made volatility more 'macro'—when interest rates and risk appetite switch, on-chain and off-chain deleveraging often becomes more synchronized and faster.

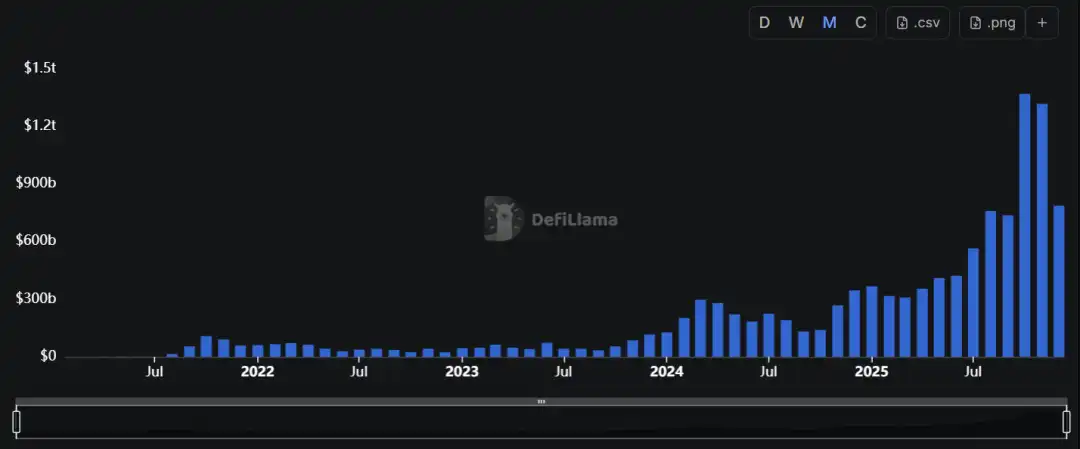

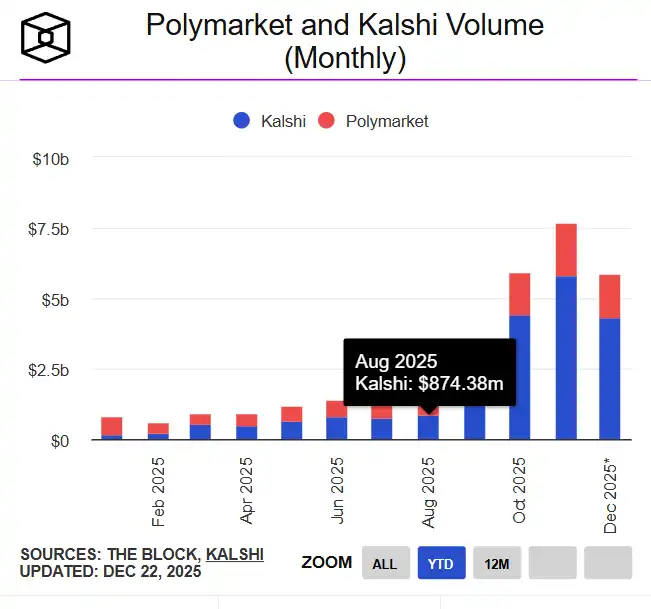

Prediction markets expanded from crypto-native applications to broader event contract markets in 2025, becoming a new incremental trading scenario. Represented by platforms like Polymarket, participation and trading scale of event contracts significantly increased; monthly trading scale grew from less than $100M in early 2024 to over $13B in November 2025, with sports and politics becoming main categories. Its deeper meaning lies in: event contracts transform macro and public issues into tradable probability curves, naturally adapt to media dissemination and information distribution,更容易 form cross-demographic user entry points, and further strengthen the coupling between crypto and macro variables (even political variables).

Overall, the structural upgrade in 2025 is pushing the industry from 'narrative-dominated price discovery' to 'product-dominated fund organization'. The layering of stablecoins, the infrastructuralization of on-chain derivatives, and the场景化 of event contracts collectively expand fund entry points and trading scenarios, also making risk transmission faster and more systematic; against the backdrop of strengthening macro and interest rate constraints, the market cycle structure further aligns with mainstream risk assets, and the explanatory power of the four-year cycle continues to weaken.

Dual Main Lines of Stablecoins: Compliance Certainty and Yield Model Cycles

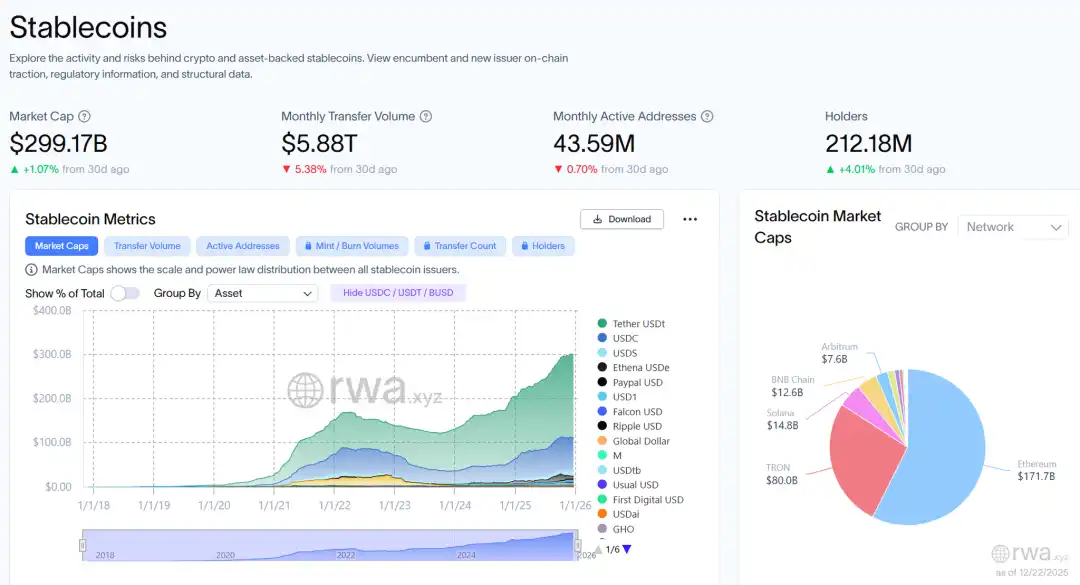

In 2025, stablecoins upgraded from on-chain trading mediums to the dollar清算 layer and fund base of the crypto system, and completed clear layering: USDT/USDC continue to form the mainstream fiat stablecoin 'cash layer', providing a liquidity network covering global trading and settlement; USDe/USDF and other yield/synthetic dollars resemble 'efficiency tools' driven by risk appetite and basis, showing significant cyclicality in expansion and contraction.

The most direct signal for the year was the substantial thickening of the on-chain dollar base: total stablecoin supply expanded from ~$205B to over $300B, and highly concentrated in the leaders (year-end附近 USDT ~$186.7B, USDC ~$77B); issuers collectively held ~$155B in US Treasury bills, making stablecoins closer to an infrastructure combination of 'tokenized cash + short-duration treasuries'. Usage side also strengthened: stablecoins accounted for ~30% of on-chain crypto trading volume, with annual on-chain activity exceeding $4T, payment-type on-chain trading volume estimated at $20–30B/day量级, real demand for cross-border settlement and fund transfer continued to rise.

On the institutional level, the GENIUS Act enacted in July incorporated payment stablecoins into requirements for permitted issuance, 1:1 reserves, redemption, and disclosure, and set access paths for foreign issuers, making 'compliance premium' begin to be priced institutionally: USDC benefits more from strengthened compliance and institutional usability, while USDT should not be simply categorized as a compliant stablecoin under the US framework, its advantage lies in the global liquidity network, but its accessibility in the US market will depend more on implementation rules and channel compliance.

The yield track completed repositioning: taking Ethena's USDe as an example, supply fell from a high of ~$14.8B in early October to ~$6–7B by year-end, verifying its structured属性 of 'expansion in顺风期, contraction in逆风期'.

Looking ahead to 2026, stablecoins remain the most certain growth轨道: competition among mainstream fiat stablecoins will shift from scale to channels and清算 networks, yield products will continue to provide顺风期 liquidity but will be more strictly priced based on stress tests and redemption resilience.

On-Chain Derivatives Platform Upgrade and Share War

In 2025, on-chain perpetual contracts crossed from 'usable products' into the infrastructure stage of 'capable of carrying mainstream trading': matching and latency, margin and清算 mechanisms, risk parameters and risk control linkage became closer to the engineering standards of centralized exchanges, and on-chain derivatives began to have the ability to分流 mainstream volume and participate in price discovery during certain periods. At the same time, fund and risk transmission became more 'macro': during windows of US stock risk appetite and interest rate expectation shifts, the volatility and deleveraging rhythm of on-chain perpetual contracts更容易 resonate in the same direction as traditional risk assets, and the market cycle's sensitivity to 'macro liquidity - risk budget' significantly increased.

The scale端 has formed a sustainably trackable 'on-chain derivatives盘子'. Based on a sample point口径 near the end of 2025, the 30-day volume of on-chain perpetual contracts was ~$1.081T, and the全市场 open interest was ~$15.4B, reflecting that this track already has the ability to常态化承 large-scale trading and risk exposure. Leading platforms still占据 the core mindshare of 'depth and risk control', but the competition logic changed substantially in 2025: market share争夺 no longer primarily relied on subsidies and listing speed, but more转向 depth, open interest沉淀, and the stability of清算秩序 during extreme行情. Taking Hyperliquid as an example, its sample point open interest was ~$6.88B, 30-day volume ~$180.4B,体现 'stronger risk exposure沉淀 + relatively steady trading scale'.

More fortunately, new entrants in the second half of 2025 were no longer just conceptual challengers, but joined the competition with quantifiable data and altered the share structure: Lighter 30-day volume ~$233.2B, cumulative volume ~$1.272T, open interest ~$1.65B; Aster 30-day volume ~$194.4B, cumulative volume ~$811.7B, open interest ~$2.45B. Based on open interest ranking口径, Hyperliquid, Aster, Lighter were already in the top three sequence (~$6.88B / $2.41B / $1.60B), indicating the track has entered the mature stage of 'multi-platform parallel competition'.

For the industry, the competition in on-chain perpetual contracts entered the stage of 'quality and resilience pricing' in 2025—trading volume can be amplified by short-term incentives, but open interest scale, fee/revenue sustainability, and risk control performance during extreme行情 better reflect real fund retention and platform stickiness.

Looking ahead to 2026, the track is likely to evolve along two lines simultaneously:

First, on-chain derivative penetration率 continues to increase;

Second, under fee compression and rising risk control thresholds, the market further concentrates towards the few platforms that can maintain depth and清算秩序 long-term.

Whether new platforms can transition from scale sprint to steady retention depends crucially on their capital efficiency and risk framework under stress tests, not just single-phase trading volume performance.

Prediction Markets Move from Crypto-Native to Event Contract Markets

In 2025, prediction markets, building on the 'event contracts (probability pricing)' validated during the 2024 US presidential election, completed the upgrade from periodic爆点 to a more independent, sustainable trading scenario: it no longer primarily relies on short-term traffic from single political events, but through high-frequency/reusable contract categories like sports, macro, and policy nodes, sediments 'probability trading' into more stable trading demand and user habits. Because event contract标的 are naturally externalized (macro data, regulatory bills, elections, sports schedules, etc.), the activity of prediction markets became significantly more linked to US stock risk appetite and interest rate expectation switches, and the rhythm of the industry application layer further shifted from the 'internal crypto narrative cycle' to a function of 'macro uncertainty × event density × risk budget'.

Data-wise, the prediction market track saw exponential expansion in 2025: full-year total volume ~$44B, with Polymarket ~$21.5B and Kalshi ~$17.1B, the scale of leading platforms is already sufficient to support stable market making and category expansion. Growth showed明显的 event-driven peaks during the year: monthly nominal volume jumped from less than $100M in early 2024 to over $13B per month in 2025 (represented by November), showing strong elasticity during high-attention event windows. Structurally, prediction markets evolved from 'political爆点 driven' to 'sports high-frequency retention + event multi-category expansion': Kalshi's November 2025 volume was ~$5.8B, with ~91% from sports; the platform disclosed its volume had reached over $1B weekly, and claimed growth of over 1000% compared to 2024, reflecting it already has a certain常态化 trading foundation.

Combined with the aforementioned changes in capital structure and the industry changes brought by crypto company IPOs, the prediction market track rapidly upgraded from 'crypto entrepreneurship' to 'financial infrastructure/data assets': Kalshi completed a $1B financing in December, valuation ~$11B, and about two months prior completed a $300M financing at a ~$5B valuation; simultaneously, traditional market infrastructure players also began to切入 with heavy capital, with ICE (NYSE parent company) reported to be considering an investment of up to $2B in Polymarket with a ~$8B pre-money valuation. The common meaning of such transactions is: event contracts are not only seen as 'trading products', but also as integratable market data, sentiment indicators, and risk pricing interfaces.

Looking ahead to 2026, prediction markets are more likely to become one of the 'more certain' structural increments in the crypto application layer: growth drivers come from event density and information uncertainty, commercialization is closer to a combination of 'transaction fees + data products + distribution channels'. If compliance paths, distribution entry points, and dispute resolution standards become clearer, prediction markets are expected to move from periodic爆款 to more常态化 event risk trading and hedging tools; their long-term ceiling mainly depends on three hard metrics: real depth (capable of承 large amounts), reliable settlement and dispute governance, and controllable compliance boundaries.

Conclusion

Looking back at 2025, the core characteristics of the crypto market were pricing framework externalization and channel competition deepening: fund entry points shifted from an endogenous cycle driven by on-chain leverage and narratives to a multi-channel system jointly constituted by ETFs, stablecoin dollar base, corporate treasuries, and equity channels (US crypto company IPOs). Channel expansion enhanced asset allocatability, but also strengthened macro boundary conditions—行情 relies more on the配合 of net inflows and financing windows, while drawdowns are more easily集中释放 during deleveraging and清算 chains.

The structural evolution inside the industry further confirmed this migration: stablecoins completed layering between the 'cash layer' and 'efficiency tools', on-chain derivatives entered the stage of规模化承 and market share competition, prediction markets and event contracts formed more independent trading scenarios. More importantly, the return of IPOs 'securitized' crypto financial infrastructure into auditable, comparable, exitable equity assets, allowing mainstream funds to participate in a more familiar way, and pushing the valuation system to converge towards 'compliance moats, risk control governance, revenue quality, and capital efficiency'—this is the core basis for our optimism about this direction.

Looking ahead to 2026, the industry slope is more dependent on three variables: whether institutional channels can continue, whether fund沉淀 is sustainable, and the resilience of leverage and risk control under stress scenarios. Among these, if US crypto company IPOs can maintain more continuous advancement and stable承, they will continuously provide valuation anchors and financing elasticity, and strengthen the industry's migration towards sustainable public market pricing.