Author: Dong Jing

Source: Wall Street News

An IPO feast comparable to the peak of the dot-com bubble is taking shape. AI giants OpenAI, Anthropic, and SpaceX are racing towards the public markets, each targeting a trillion-dollar valuation. Their combined scale is enough to reshape the landscape of the U.S. stock market. This unprecedented wave of listings is both the ultimate stress test for AI investment logic and the biggest variable for the direction of risky assets this year.

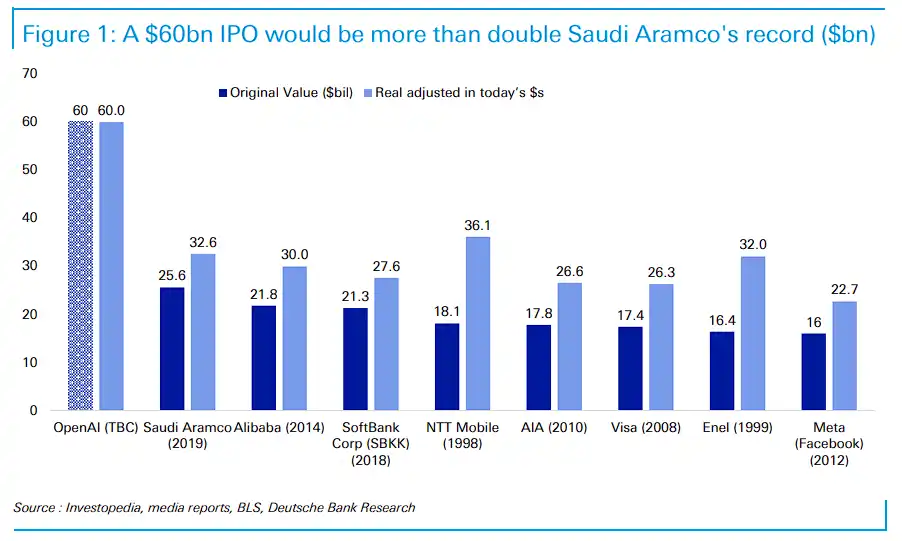

On May 22, according to a Wall Street News article, OpenAI has prepared to confidentially file its IPO application with regulators. The listing could happen as early as September this year, targeting a valuation exceeding $1 trillion and aiming to raise approximately $60 billion. This would more than double the $25.6 billion IPO record set by Saudi Aramco in 2019.

Meanwhile, rival Anthropic is also advancing its own listing plans and disclosed that its Q2 revenue is expected to double sequentially to $10.9 billion, potentially achieving quarterly operating profitability for the first time. Deutsche Bank noted in a research report that the landing of these two IPOs "is likely to become a major swing factor for the direction of risky assets this year," and is a macro theme that must be closely watched.

However, beneath the glossy valuations, the two companies' financial fundamentals are starkly different. OpenAI's Q1 revenue was $5.7 billion, but its adjusted operating profit margin was -122%, meaning it lost $1.22 for every dollar of revenue generated. It is not expected to achieve positive cash flow until 2029 or 2030 at the earliest. Anthropic's revenue was $4.8 billion in the same quarter and is projected to jump to $10.9 billion in Q2, with an expected operating profit of about $559 million, having already touched the threshold of profitability.

Analysis points out that these two companies are competing on the same stage but present vastly different business logics, presenting public market investors with a rare dilemma.

The Largest IPO in History: How Shocking Are the Numbers?

Deutsche Bank noted in a research report that the scale of either OpenAI's or Anthropic's single IPO would exceed twice the fundraising amount of Saudi Aramco's 2019 IPO. Even after inflation adjustment, it would easily become the largest IPO in history.

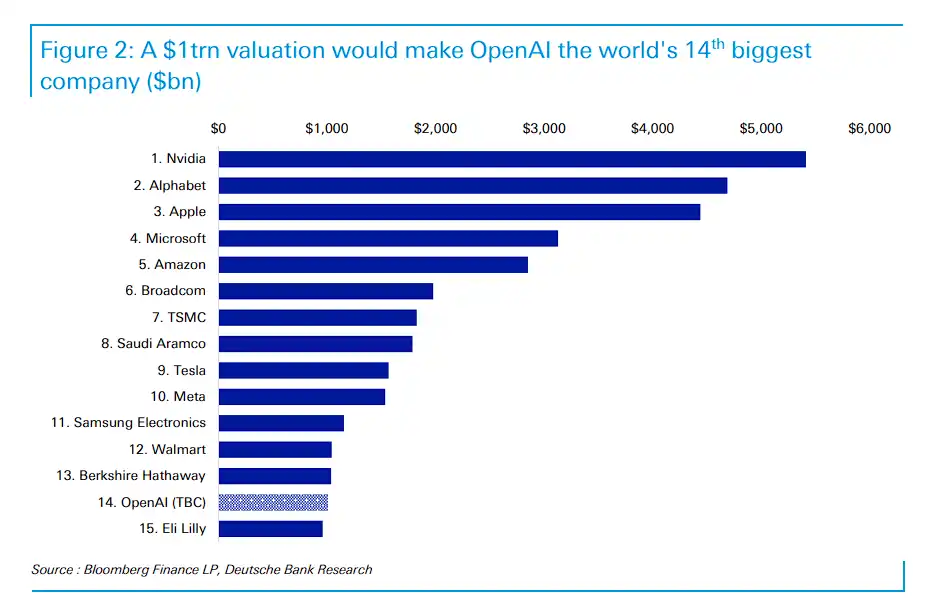

Deutsche Bank stated in another report that if OpenAI achieves its target valuation of over $1 trillion, it would become the world's 14th largest company by market capitalization, trailing only Berkshire Hathaway and surpassing Eli Lilly.

For comparison, Berkshire's revenue last year exceeded $370 billion with a net profit of $67 billion; Eli Lilly's sales exceeded $65 billion with a profit of $21 billion. In contrast, OpenAI is not yet profitable, has an annualized revenue of about $30 billion, and only has thousands of employees.

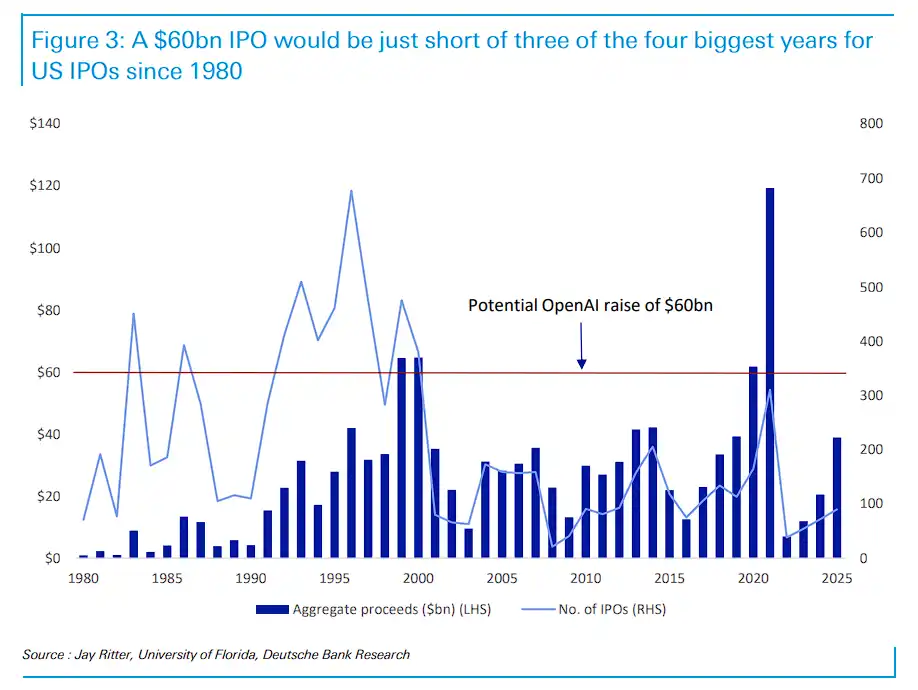

From a market capacity perspective, Deutsche Bank believes the current total U.S. stock market capitalization is about $70 trillion, five times that of the peak of the dot-com bubble. The market's digestion capacity is far stronger than in the late 1990s.

Back then, there were nearly 500 IPOs annually on average, whereas this decade averages only about 120, and today's listed companies are generally more mature.

Furthermore, a single $60 billion IPO is slightly less than the total fundraising for all U.S. IPOs in both 1999 and 2000 (each around $65 billion), equivalent to half of the record $119 billion set in 2021.

The 'Siphoning Effect' of the Behemoths and the Massive Passive Fund Reallocation

As these giants move towards public markets, their potential liquidity drainage effect on the U.S. stock market has already raised high alert on Wall Street.

The clustering of SpaceX, OpenAI, and Anthropic listings, combined with Nasdaq's newly introduced "fast inclusion" mechanism, is brewing an unprecedented massive reallocation of passive funds—the siphoning effect of the AI behemoths.

As mentioned in a Wall Street News article, JPMorgan Chase estimates that if SpaceX targets a $2 trillion valuation and ultimately achieves a 50% free float, passive funds would have to sell approximately $95 billion of their holdings in the current eight major Wall Street tech stocks (Nvidia, Apple, Microsoft, Amazon, Google, Broadcom, Meta, Tesla) to make room for the new entries.

Todd Sohn, Chief ETF Strategist at Strategas, points out that since the initial public float of an IPO is typically only 5%, while ETFs track trillions in assets, this extreme supply-demand imbalance will make the index inclusion process "slightly crazy." Passive investors may have no choice but to buy at high prices.

Valérie Noël, Head of Trading at Syz Group, stated that the market has already begun betting on downward pressure on existing large-cap stocks.

According to information disclosed on March 28 this year, OpenAI's public listing will be a substantial referendum on the entire AI investment logic. That information showed that OpenAI's revenue reached $13.1 billion in 2025, but its net loss in 2026 is projected to be $14 billion.

Simultaneously, OpenAI has committed to investing approximately $1.4 trillion in infrastructure construction before 2033. If S&P Global, FTSE Russell, and Nasdaq adopt fast-inclusion rules, they could force passive funds to buy around $24 billion to $48 billion immediately after the listing.

Faced with such a massive fund restructuring, ordinary investors, whether active or not, will see their portfolios passively reshaped as rules change.

Deutsche Bank noted in its report that the landing method of these IPOs will be a major swing factor for the direction of risky assets this year. PitchBook's analysis is more blunt:

There has been a "systematic quality inversion" in the private market—the companies with the highest valuations score lowest on the business quality metrics that truly matter for pricing in the public market.

For ordinary investors holding index funds or ETFs, it's hard to stay out of this game: whether active or not, their investment portfolios will be passively reshaped as index rules change.

For active investors, once the S-1 filings are public and all financial secrets are laid bare, the market will face a clear choice: to believe in a company that has already found a profitable model, or a giant asking the market for several more years and hundreds of billions of dollars to explore profitability?

The answer will determine whether this frenzy marks the start of a new cycle or the last dance before the party ends.

A Tale of Two Extremes: Anthropic Profits vs. OpenAI's Huge Losses

Despite soaring valuations, the financial conditions of the two AI leaders present starkly different pictures. Anthropic has begun to turn a profit, challenging the traditional notion that massive spending by AI companies would hinder near-term profitability.

According to a Wall Street News article, on Wednesday local time, The Wall Street Journal reported that Anthropic's Q2 revenue is expected to more than double to $10.9 billion and achieve an operating profit of approximately $559 million.

Anthropic's gross margin has jumped from 38% to over 70%. Its CEO, Dario Amodei, once joked that revenue growth had become "too difficult to handle."

The company's success is largely attributed to explosive demand from enterprise clients for its programming tools. About 85% of its revenue comes from enterprise and developer customers, a model with clear willingness to pay and relatively lower service costs.

In contrast, OpenAI is still losing money.

As mentioned in a Wall Street News article, data shows OpenAI's Q1 revenue was $5.7 billion, but its adjusted operating profit margin was -122%, meaning it loses $1.22 for every dollar earned.

Approximately 85% of OpenAI's revenue is related to ChatGPT consumer subscriptions. Despite having 55 million paying users, it supports a vast pool of over 900 million weekly active users, creating a massive cost black hole due to inference expenses for the free users.

OpenAI is not expected to achieve positive cash flow until 2029 or 2030. Its CEO Sam Altman and Head of Applied Business Fidji Simo are trying to shift focus towards commercial clients who can directly generate revenue.

At the IPO narrative level, the two companies are telling entirely different stories. Anthropic, armed with verified quarterly profitability data, tells a story comparable to Salesforce or ServiceNow—the logic of an enterprise software company.

OpenAI needs to convince the market to believe that AI agents, image generation, and even advertising businesses will eventually turn its massive consumer traffic into profit.

In Sam Altman's plan, the ChatGPT advertising business might bring in about $102 billion in revenue by 2030. But this requires time, and time is precisely the most scarce resource for OpenAI as it trades losses for growth.

AI Giants Rushing to IPO: Essentially Passing the 'Hot Potato' to Retail Investors?

According to a Wall Street News article, in the view of Joachim Klement, Managing Director at Panmure Liberum, this wave of AI giant IPOs is essentially a "risk transfer"—a large-scale offloading of early-stage investment risks onto retail investors, pension funds, and other institutions.

He believes that companies like OpenAI and Anthropic are accelerating their listings while investor sentiment is high, aiming to cash in at high valuations before the hype fades. Early institutional investors can exit entirely in the public market, while the retail investors and pension funds that take over will directly face the risk of financial logic eventually returning to reality.

He directly characterized this process as "the action of transferring investment risk on a massive scale from current holders to those willing to pay for the story."

Klement referenced Alan Greenspan's 1996 "irrational exuberance" warning as a benchmark—it was three years before the bubble burst. He judged that the AI hype in 2026 could still persist, and the likelihood of hyperscale cloud providers cutting investments is not high. However, the "impossible math" will eventually return to reality, "perhaps not in 2026, but 2027 or 2028 might see it arrive."