Written by: Liam 'Akiba' Wright

Compiled by: Saoirse, Foresight News

Key Takeaways

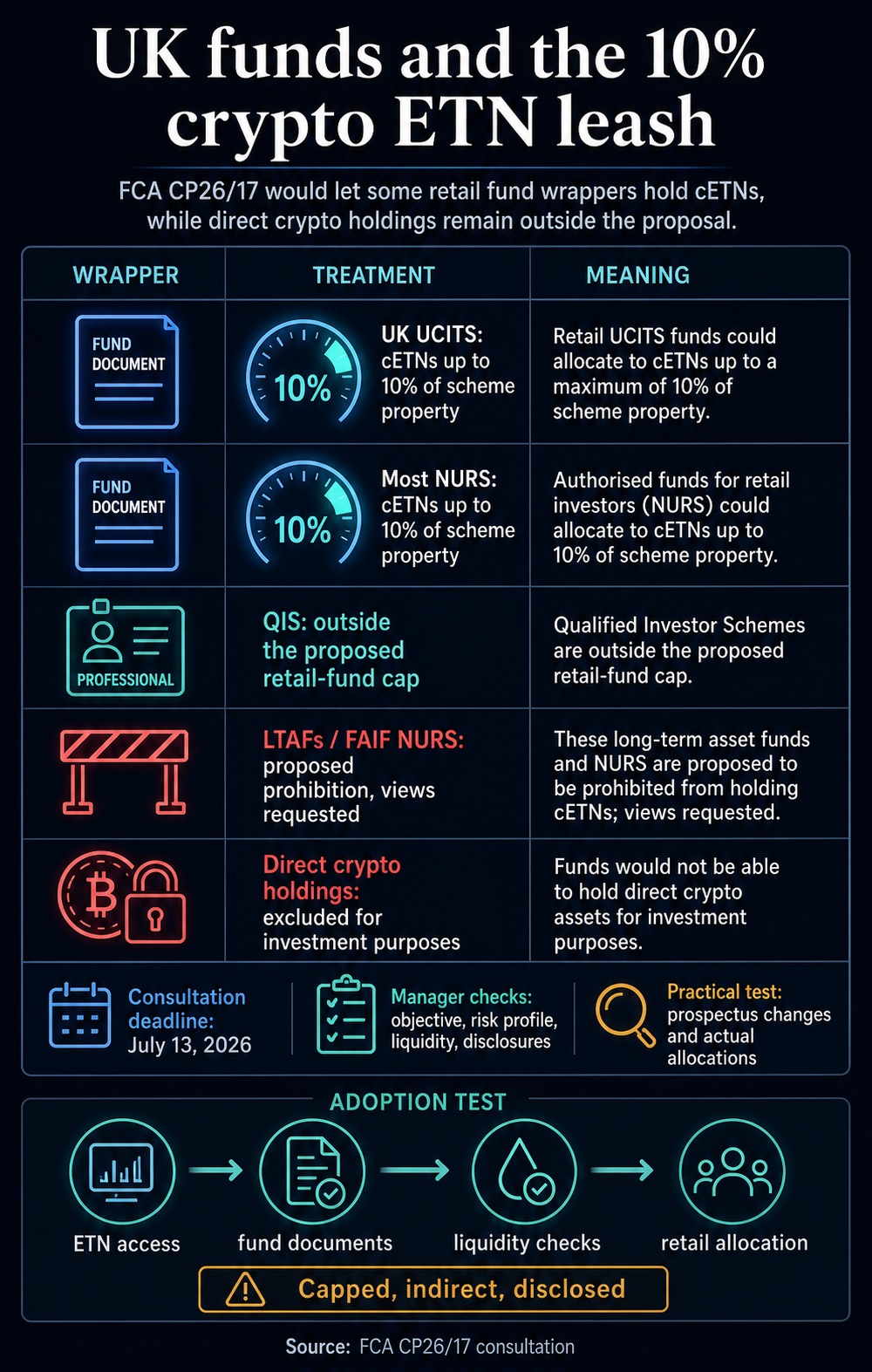

- The UK Financial Conduct Authority (FCA) is soliciting public feedback on a proposal to allow UK UCITS funds and most non-UCITS retail schemes (NURS) to allocate up to 10% of their assets to crypto asset exchange-traded notes (ETNs).

- The new rules would enable ordinary retail funds to gain indirect exposure to crypto assets but still prohibit funds from directly holding native cryptocurrencies like Bitcoin and Ethereum.

- Whether this policy will be widely adopted in practice rests with fund managers; the stringent disclosure, liquidity assessment, and product suitability requirements may deter many asset management firms.

The UK Financial Conduct Authority is considering a new rule that would allow UCITS fund products and most non-UCITS retail schemes to hold crypto asset exchange-traded notes, with the position size capped at 10% of the fund's total assets.

This proposal, included in the FCA consultation paper 'CP26/17', seeks to further integrate crypto asset exposure into the regulated public fund system. While ordinary retail investors have already been able to purchase crypto ETNs individually on exchanges, this new rule addresses the core question: what proportion of a diversified portfolio managed by a licensed fund management firm can be allocated to such notes.

The regulator's answer is strict limitation. Funds may only allocate to such crypto ETNs when they are aligned with the fund's stated investment objective and risk profile, with an overall hard cap on the position size.

The proposal clearly states that directly holding Bitcoin, Ethereum, or other native cryptocurrencies for investment purposes remains prohibited. Public consultation on the fund-related rules closes on July 13, 2026.

Specific Scope of the Position Limit

This draft rule creates a crypto asset investment channel with a position cap for UK UCITS funds and for non-UCITS retail schemes, with specific exceptions. The limit is calculated based on the fund's total assets, allowing a fund to invest up to 10% in transferable securities such as crypto asset exchange-traded notes (crypto ETNs).

This percentage allows funds to moderately gain crypto exposure while restricting it to a secondary allocation. A balanced multi-asset fund could use crypto ETNs as a small satellite position. (Note: A satellite position refers to a small, flexible allocation, typically 5%–20%, used to pair with niche, high-volatility assets seeking alpha; it carries higher risk and is more offensive, without altering the overall portfolio style. Crypto ETNs are a typical satellite holding.)

Funds focused on traditional retail investment portfolios remain fully within the licensed retail fund regulatory framework, with crypto exposure only permissible via ETN products and still subject to the 10% constraint.

The FCA outlines differentiated regulatory rules for different fund types: Qualified Investor Schemes (QIS) targeting professional clients and sophisticated investors are not subject to the 10% cap applicable to retail funds.

For Long-Term Asset Funds (LTAF) and non-UCITS retail schemes operating as funds of alternative investment funds (FAIFs), the proposal seeks to completely prohibit allocation to crypto ETNs, and the regulator is also soliciting feedback on this restriction.

This chart is a policy diagram from the UK FCA consultation paper CP26/17: The UK proposes to allow UCITS and most NURS funds for ordinary investors to allocate up to 10% to crypto ETNs, with no cap for professional investor QIS, a ban for long-term asset funds, and all funds still prohibited from directly holding cryptocurrencies. The policy consultation closes on July 13, 2026.

This differentiated regulatory framework forms the core of the proposal: the regulator is cautiously opening an investment channel for crypto assets through securities and fund rules, while isolating the custody of native cryptocurrencies from fund portfolios.

Funds can purchase listed securities on compliant trading venues, thereby gaining exposure to crypto asset price returns, while the underlying native crypto assets themselves are not included in the licensed fund's investment holdings.

This proposal continues the direction of previous FCA policy—in 2025, the regulator already permitted retail investors to trade crypto ETNs on UK-recognized exchanges.

That policy took effect on October 8, 2025, allowing ordinary consumers to trade crypto ETNs on FCA-recognized UK investment exchanges, with relevant financial promotion rules and consumer protection regulations applying concurrently.

The regulator consistently classifies crypto ETNs as high-risk: retail crypto ETNs are not covered by the Financial Services Compensation Scheme, and the ban on crypto derivatives for ordinary retail investors remains unchanged.

The regulator believes that current crypto market infrastructure and maturity provide a foundation for controlled opening, but the high-risk nature of underlying crypto assets still requires clear labeling. The fund-related proposal follows the same regulatory logic.

Crypto ETNs have now become a regular listed product category on UK exchanges, with the London Stock Exchange continuing to provide related trading services since their listing a year ago.

For fund products, however, gaining crypto exposure via ETNs means managers must assume an additional layer of compliance responsibility. Managers need to determine if listed crypto ETNs meet investment eligibility criteria and whether such exposure aligns with the fund's investment objectives, liquidity levels, risk limits, and retail disclosure requirements.

The FCA requires fund managers to: fully understand the characteristics of the assets their fund invests in, conduct complete due diligence on investment targets, and continuously monitor whether products comply with investment objectives, operational strategies, risk ceilings, and liquidity standards; concurrently, they must assess whether crypto assets and crypto ETNs can maintain sufficient liquidity under stressed market conditions.

The 10% position cap is a direct risk control measure, but supporting compliance work such as disclosure and liquidity assessment is key to determining the practical usability of this investment permission.

The FCA states that licensed funds holding crypto ETNs will follow existing disclosure rules, requiring managers to strictly adhere to regulations concerning fund investment objectives, strategies, marketing, consumer duty, and crypto asset risk summaries.

It also stipulates that if a fund exhibits high net asset value volatility or is expected to experience significantly amplified volatility, UCITS fund managers must prominently label volatility risk warnings in product materials.

Managers planning to allocate to crypto ETNs need to clearly explain the nature of the crypto asset exposure in fund documents and consumer-facing promotional materials, ensuring product positioning is unambiguous.

Even a small allocation to crypto ETNs, as long as it exceeds a negligible minimal proportion, will become a core component of the investment strategy—the risk characteristics of crypto ETNs differ significantly from most traditional transferable securities.

The FCA also requires managers to assess crypto ETN holdings in the context of the overall investment portfolio, considering other high-risk assets within the portfolio, indirect crypto exposure held through other funds, and assets with price correlations to crypto assets (e.g., bonds issued by crypto companies).

Therefore, the 10% crypto ETN limit does not cover other various risk exposures linked to crypto assets within the fund portfolio.

For retail investors, the practical effect after the new rule takes effect is that crypto assets can be more routinely included in mainstream investment portfolios, but all related risk exposures will be clearly disclosed, continuously monitored, and assessed in conjunction with other assets in the portfolio.

The Real Test of Policy Implementation

The proposal merely opens the investment channel; whether it becomes widespread ultimately depends on whether fund managers, distribution platforms, asset custodians, and distribution channels are willing to bear the associated costs of revising documents, internal governance, and investor suitability reviews.

There are two possible market development scenarios: The first is moderate adoption and spread. Asset management firms use crypto ETNs as a minor allocation tool within diversified funds. If this scenario materializes, the FCA's new rule would mark a substantive shift for the industry: crypto asset exposure is no longer limited to individual purchases by investors or products solely for professional investors; mainstream public funds can incorporate crypto allocations under robust risk controls.

The second scenario is that the policy remains largely symbolic. Managers may decide that the 10% limit, burdensome disclosure obligations, liquidity concerns, and brand reputation risks outweigh the benefits of allocating to crypto ETNs. Ultimately, only a handful of products utilize this investment permission, and the actual capital allocated post-implementation remains very limited.

Thus, this proposal is essentially a step in the progressive formalization of the crypto market system, not a full liberalization of crypto investment for public funds.

The FCA acknowledges that the crypto ETN market has matured enough to open investment channels to some licensed funds, while simultaneously taking strict measures to prevent crypto asset exposure from becoming a primary risk source for retail investment portfolios.

Subsequent market implementation signals will be reflected in asset allocation actions by asset managers, updates to fund filing documents, revisions to product descriptions on sales platforms, and other such behaviors.

After this consultation concludes, UK asset managers have two choices: revise fund prospectuses, key investor information documents (KIIDs), and platform marketing materials to include crypto ETN allocation terms; or let this 10% position limit policy remain on paper, serving only as a symbolic opening. Until then, while crypto assets can gain indirect exposure through fund products, they remain strictly constrained.