Source: Wall Street Journal

If you set the clock back two years, few South Koreans would have believed that the fastest way to create wealth would shift from apartment buildings in Gangnam District to the trading halls on Seoul's Yeouido.

For the past two decades, the wealth code for Korean households was almost singular: buying property.

Whether it was school district housing in Gangnam, Seoul, or new residential complexes in Gyeonggi Province, getting on the property ladder almost guaranteed wealth appreciation. Data from the Bank of Korea shows that real estate long accounted for over 60% of Korean household assets, while stocks' share in total household assets remained in the single digits for years. For the vast majority of Koreans, the stock market was more akin to a casino, while real estate was the true store of wealth.

But entering 2026, a fundamental shift suddenly occurred.

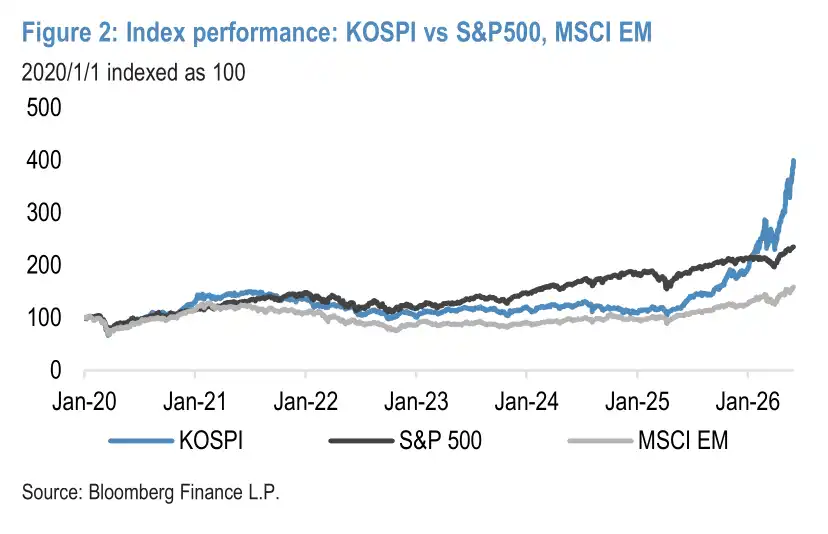

J.P. Morgan's latest report presented a staggering figure: in this super bull market driven jointly by AI and policy reforms, the South Korean KOSPI index has year-to-date crushed global markets with a terrifying 109% surge (compared to the S&P 500's mere +11%). This has led to a paper gain in the domestic stock and fund assets of Korean households that has soared past 1000 trillion won (approximately $730 billion).

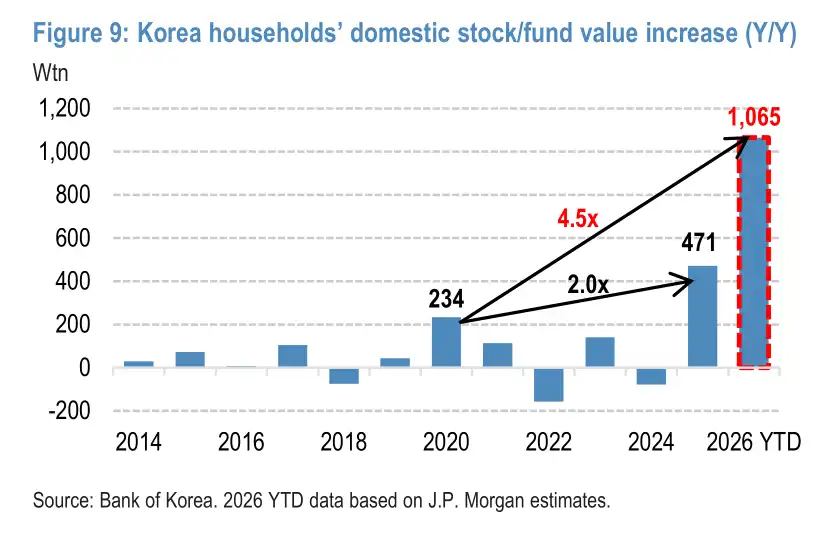

What does 1000 trillion won represent? It's 4.5 times the peak of the retail frenzy during the 2020 pandemic (234 trillion won), close to 40% of South Korea's annual GDP. This is a speed of wealth creation never seen before in the history of the Korean capital market. For a country with a total population of only 51 million, it almost means an average paper wealth increase of nearly 20 million won per person.

However, this feast of wealth creation is far more complex than the numbers suggest. Behind it intertwine three narratives: the AI-driven semiconductor supercycle, the capital market institutional reforms led by the South Korean government, and a series of real estate control policies designed to lock capital within the stock market. The combination of these three factors has jointly catalyzed this unprecedented wealth effect.

But simultaneously, highly concentrated structural risks, rapidly accumulating leverage, and the deeply ingrained speculative impulses of retail investors are testing how long this feast can last.

Every Previous Bull Market Was a Story of Heartbreak for Retail Investors

The Korean stock market is not short of bull markets. The problem is, every bull market has ultimately become a story of heartbreak for retail investors.

From the dot-com bubble to the new energy frenzy and the retail frenzy during the pandemic, whenever a rally emerged, retail investors rushed in, keen on high-frequency trading and chasing hot themes, with small-cap and concept stocks often being bid up to ridiculous valuations. Once the party ended, wealth evaporated just as quickly.

This is also why the famous "Korea Discount" has persisted long-term. Companies with similar profitability are often valued lower in Korea compared to their US and Japanese peers. Investors' reluctance to grant higher valuations isn't because Korean companies aren't profitable, but because they don't believe those profits will genuinely return to shareholders.

Opaque governance, controlling shareholder interests overriding those of minority shareholders—this has been an unresolved deadlock in the Korean capital market for decades. This is also why money made in the stock market didn't flow back to consumption or stay in the market—it merely served as "ammunition" for buying property.

Understanding this vicious cycle is key to grasping what's truly different about this bull market: for the first time, two forces are working in tandem to dismantle this cycle.

AI Is the Spark, Institutional Reform Is the Foundation

One force comes from the demand side: AI.

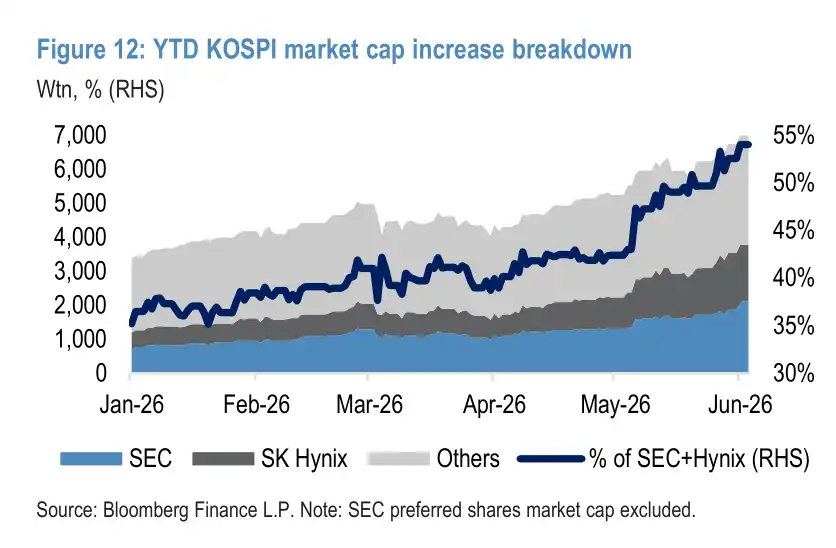

In terms of index contribution, Samsung Electronics and SK Hynix are the core driving forces of this rally. With HBM (High Bandwidth Memory) becoming the most critical infrastructure in the AI era, these two memory giants have exploded—Samsung Electronics is up 201% year-to-date, SK Hynix has soared 256%. Together, the two companies contributed roughly 72% of the KOSPI's year-to-date gains, with their combined market cap rising to 54% of the total index weight.

The semiconductor supercycle has injected unprecedented fundamental support into the Korean stock market.

The other force comes from supply-side institutional reforms.

Under the "Value-Up" capital market reform framework pushed by the South Korean government, systemic issues plaguing the market for over two decades are being addressed: amendments to the Commercial Code establishing directors' fiduciary duty to all shareholders, strengthened protection for minority shareholders, and forceful promotion of listed companies to increase dividends and share buybacks.

These reforms have, for the first time, laid an institutional foundation for seriously tackling the "Korea Discount," and have also started to shift the perception of stocks in Korean households from "speculative tools" towards "long-term assets."

It is the superposition of these two forces that opened the floodgates for Koreans to pour into the stock market.

The total number of active stock trading accounts has soared to a historic high of 107 million. The share of stocks and funds in Korean households' financial assets has risen to 23%, surpassing the previous peak of 21% during the 2020 pandemic.

The Government's Third Move: Blocking Money at the Door of the Property Market

But for the wealth effect to truly translate into consumption momentum, having a rally and reforms alone isn't enough.

The South Korean government did a third thing, arguably the most crucial one: it proactively blocked the channel for money flowing back into the property market.

This is the core mechanism for understanding this "super cycle." In the past, stock market gains were meaningless because the money made would ultimately flood into the property market as down payments—the stock market was merely a reservoir for real estate.

This time, the government used a series of extremely stringent property market controls to lock this channel shut: a mortgage cap of 600 million won in the Seoul metropolitan area, a complete ban on mortgage applications for multi-property holders, an announcement to drastically increase housing supply by 1.35 million units by 2030, and in May 2026, the temporary extension of heavy capital gains tax benefits for multi-property holders formally expired.

Expectations for continued property price increases began to cool. The 1000 trillion won of wealth created in the stock market, for the first time, had no exit flowing into real estate and was forced to circulate within the financial system—and began to transmit to real consumption.

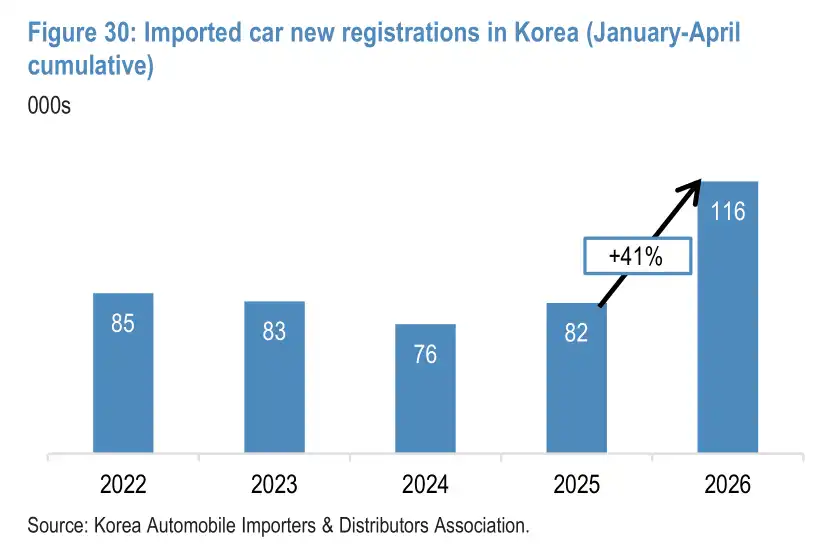

In Q1 2026, department store sales growth in Korea reached 17%; in the first four months of the year, new registrations of imported luxury cars surged 41% year-on-year; high-end luxury goods and credit card personal spending showed significant recovery. The wealth effect is transforming from paper numbers into higher table turnover rates at restaurants around Yeouido, into longer queues outside Shinsegae Department Store.

J.P. Morgan's report estimates that even using the Bank of Korea's historically most conservative wealth conversion rate of 1.3%, this 1065 trillion won asset appreciation would generate approximately 14 trillion won in incremental consumption; if calculated using the higher-end Western market conversion rate of 4%, the wealth effect could even reach 43 trillion won, equivalent to 1.6% of GDP. They characterize this round as a "super cycle" of the wealth effect.

But Not Everyone Is at the Main Table

However, not everyone is seated at the main table for this feast.

Wealth distribution is extremely uneven. This rally is dominated by two mega-cap stocks, yet retail investors hold only about 15%-20% of Samsung and SK Hynix, far below their average holding level of around 35% across the entire KOSPI market—they systematically missed the main surge.

J.P. Morgan data shows that the average return of the top 20 stocks most favored by net retail buying in 2025 is only 44% year-to-date in 2026, underperforming the broader market by a full 65 percentage points.

The stratification in consumption is equally stark. The wealth effect first and most significantly benefited high-end consumption: luxury goods, imported luxury cars, and high-end department stores became the biggest winners.

Representatives of mass daily needs like large supermarkets, online FMCG e-commerce (e.g., Coupang, down 29% year-to-date), and the food delivery industry have hardly enjoyed this wave of benefits. Food delivery even faces headwinds as people return to upscale dine-in experiences.

This super cycle is, in essence, a highly concentrated redistribution of wealth, not a widespread, inclusive prosperity.

How Much Farther Can This Leverage-Laden Train Go?

Advertisements for index ETFs are ubiquitous on Seoul's buses and subway stations.

This should be a reassuring signal—the proliferation of ETFs typically indicates retail investors are moving from betting on single stocks towards diversified allocation, a sign of market maturation.

But in Korea, this signal is quickly distorted by another set of data: leveraged ETFs account for only 3.7% of total ETF assets but contribute nearly 20% of the entire ETF market's trading volume. The government even approved "double-leveraged single-stock ETFs" specifically tracking Samsung and SK Hynix, adding more fuel to the fire at the market's most feverish moment.

Korean retail investors are buying ETFs, but they're turning a tool meant for risk diversification into a chip for doubling down.

More unsettling is the FOMO (Fear Of Missing Out) sentiment permeating the entire market.

During NVIDIA CEO Jensen Huang's visit to Korea, the stocks of any company rumored to be meeting with him invariably soared. When rumors spread that he might wear a Doosan Bears jersey to a baseball game, Doosan-affiliated stocks all hit limit-up—only to fall back just as sharply the day the official confirmation came. The market is operating on an extremely simplistic logic: just having a meeting with Jensen Huang can bring several limit-up gains.

The risks are not just emotional.

Margin balance has surged to historically rare highs, over half the index's market cap is concentrated in just two stocks, and the fate of the entire market is now deeply tied to the health of the global AI industry.

For the past two decades, the most popular saying among Korean youth was: "If you can't afford a place in Gangnam, you'll never catch up with wealth growth."

Today, amidst the flickering numbers in the Yeouido trading halls, more and more Koreans are beginning to experience another possibility: the appreciation of household wealth doesn't have to rely solely on steel and concrete; it can also be tied to the train of global technological innovation.

But just how far this train, loaded with leverage and fervor, can travel—the real test is only just beginning.