Author: Yukio Takanoue

The semiconductor industry, particularly the memory market, is currently undergoing an extraordinary expansion that can only be described as "explosive growth." Terms like "booming" are insufficient to capture the phenomenon. One glance at the charts is enough to be astonished by its scale.

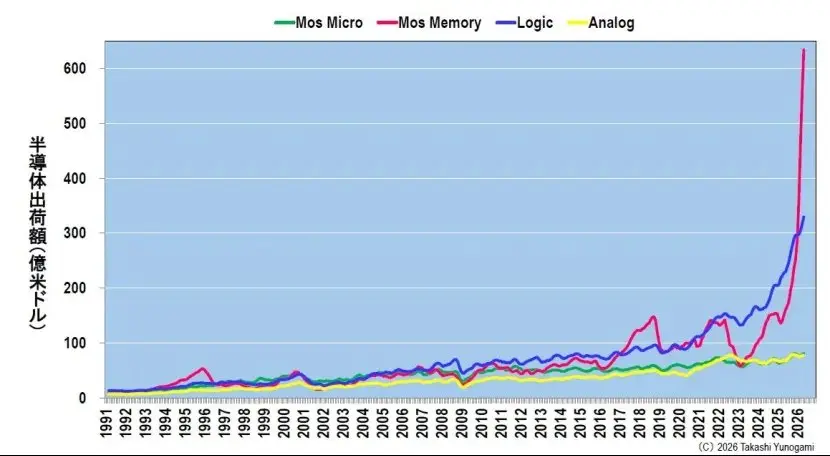

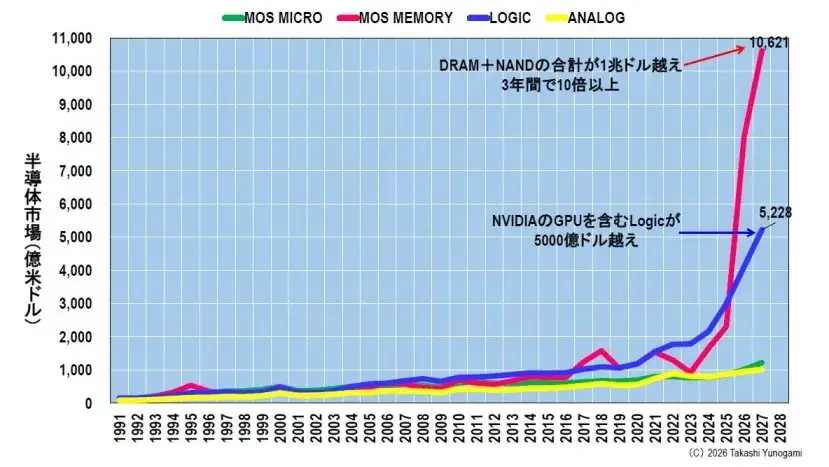

Figure 1 shows the three-month moving average shipment values for various types of semiconductors based on World Semiconductor Trade Statistics (WSTS) data from 1991 to May 2026. Over the past 30 years, the four major categories—Micro, Memory, Logic, and Analog—have shown a steady upward trend overall, despite economic fluctuations. This represents the "normal course of development" for the semiconductor industry.

However, since around 2024, logic circuits, and especially the recently surging memory, have shown an almost vertical upward trajectory, completely overturning conventional understanding. Memory growth, in particular, is astonishing, nearly breaking through the chart's peak. This growth is so rapid that the accumulated history of the past 30 years seems like just a warm-up.

Based on my many years of closely observing the semiconductor market, I can confidently say that the memory market has never experienced such steep growth. This is a historic anomaly, shaking the very foundations of the semiconductor industry.

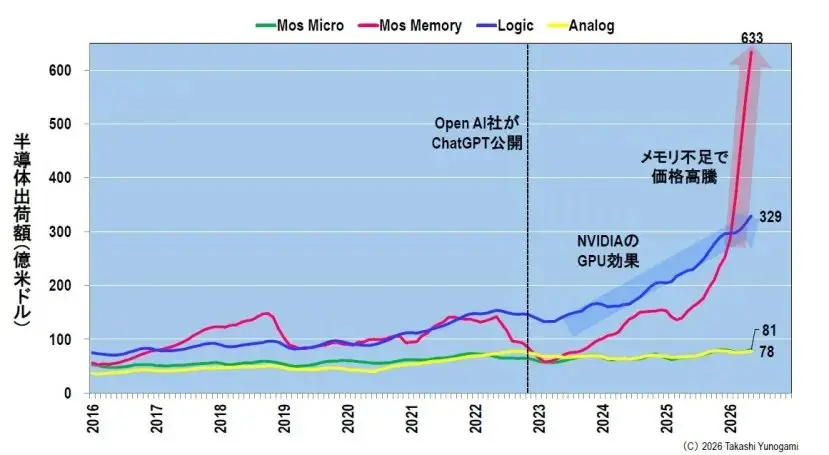

The increase is tenfold in roughly a decade, with a staggering year-on-year growth rate of 285%. Figure 2 illustrates this explosive growth, focusing on the period from 2016 onward. Monthly shipments of MOS memory were around $5.6 billion in 2016. After a brief boom during the 2017-2018 "memory bubble," shipments plunged to just $5.8 billion during the recession around early 2023. This marked the trough of the semiconductor downturn.

However, the subsequent recovery, or rather surge. As of May 2026, monthly memory shipments have skyrocketed to $63.3 billion. Compared to 2016 levels, that's over 11 times growth in just a decade. Compared to the early 2023 trough, it's about 10.7 times growth in just a few years.

Similarly, Figure 2 shows the logic business scale, which includes NVIDIA GPUs, also grew from $13.3 billion to $31.6 billion, clearly showing the "NVIDIA GPU effect" and "AI effect." However, even the growth of the logic business appears relatively modest compared to the explosive growth of the memory business.

Looking at growth rates makes the anomaly even clearer. Figure 3 shows the year-on-year growth rates for the same data. Memory's recent year-on-year growth rate is as high as 285%, a historic high.

For reference, even at the peak of the previous "memory bubble" (around 2017), the annual growth rate was about 60%. By comparison, you can see how astonishing the current growth rate is. Looking at the other three categories in Figure 3, even logic circuits are only around 40%, while microcontrollers and analog circuits are at just 14-19%. In other words, only memory growth has truly reached "another level."

DRAM and NAND Are Growing Explosively

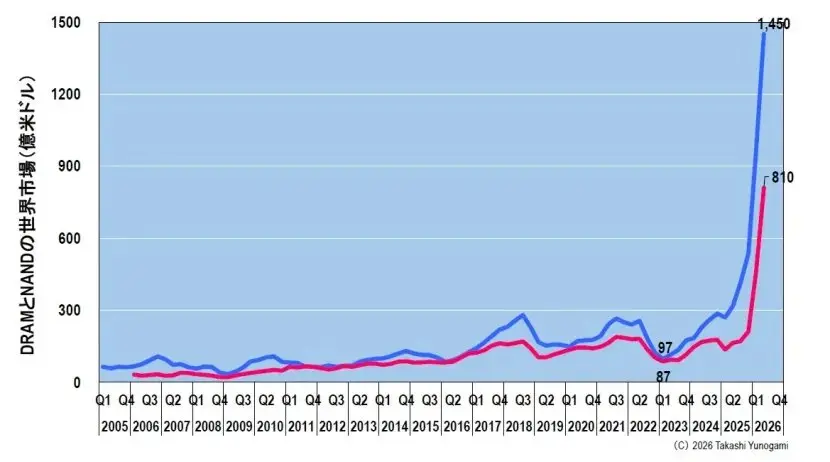

Within the memory market, the primary drivers of its explosive growth are the two major memory products: DRAM and NAND flash (hereafter NAND). Figure 4 shows the global DRAM and NAND market quarterly overview based on TrendForce data.

In early 2023, during the semiconductor industry downturn, DRAM prices hit rock bottom at just $9.7 billion, and NAND prices fell to $8.7 billion. It was a dark period where all memory manufacturers incurred losses and were forced to cut production.

However, by Q2 2026, the DRAM market size is projected to jump to $145 billion, and the NAND market size to $81 billion. Compared to the early 2023 lows, the DRAM market grew about 15 times, and the NAND market about 9 times. Combined, the quarterly total reaches $226 billion, with an annual total exceeding $900 billion—a scale that seems almost unbelievable at first glance.

Memory, once considered a "cheap standard" or "commodity," is now poised to take the leadership role in the semiconductor industry away from microcomputers (like logic and MPUs).

The Reason is Abnormal Soaring of Memory and Wafer Prices

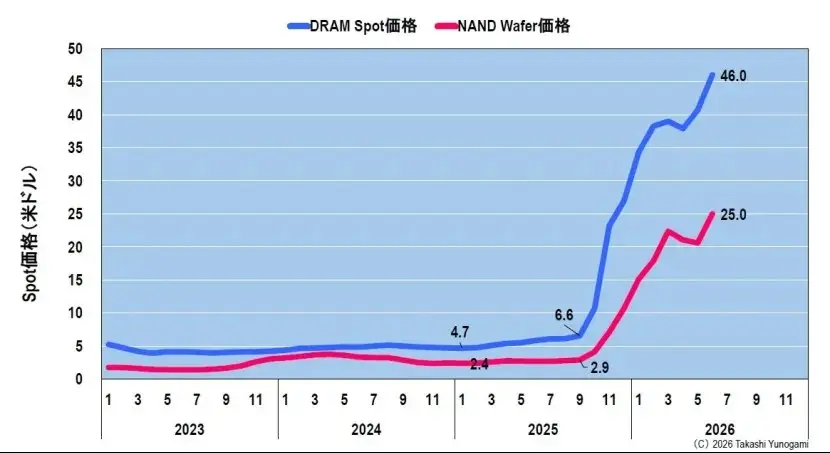

Why has the memory market expanded to such a scale? The key point is that this explosive growth is not solely due to increased shipment volume; the biggest factor is the abnormal surge in memory prices themselves.

Figure 5 shows the trend of DRAM (DDR5 16Gb 2Gx8) spot prices and NAND (1Tb TLC wafer) wafer prices. In early 2025, DRAM spot prices were only $4.70. Recently, prices have skyrocketed to $46.00, an increase of about 10 times. NAND wafer prices also jumped from $2.40 to $25.00, also an increase of about 10 times.

In other words, the primary reason for the tenfold market scale growth is not a tenfold increase in shipment volume, but because the "unit price" has surged nearly tenfold. Even if memory sales volume remained unchanged, revenue would grow tenfold. This is the mechanism behind the explosive growth in memory market size.

For memory manufacturers, this is an ideal environment. After all, prices automatically rise without significant capital investment, dramatically improving profit margins. As will be discussed later, the soaring stock prices of memory manufacturers are also due to the rapid profit growth brought about by this abnormal price increase.

The Reasons for the Price Surge

So why are memory prices soaring? It's because demand far exceeds supply. Tracing the source of this demand reveals it's thanks to the astonishingly massive investments made by hyperscale data center operators.

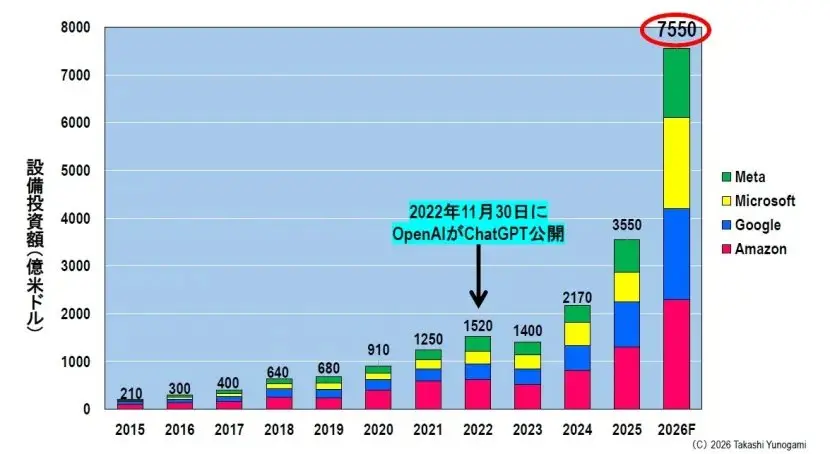

Figure 6 shows the capital expenditure (CapEx) trends of the four major hyperscale data center operators (Amazon, Google, Microsoft, and Meta). In 2015, the total CapEx for these four companies was just $21 billion. Even that was considered a "huge amount" at the time.

However, since OpenAI released ChatGPT in November 2022, sparking a generative AI boom, the capital investment curve has climbed steeply. The total investment by these four companies is projected to reach $355 billion in 2025 and a staggering $755 billion in 2026. This represents an unprecedented investment boom, with investments growing about 36 times in just over a decade since 2015.

$755 billion is well over 120 trillion yen. Just four companies plan to invest an amount equivalent to Japan's national budget (general account) in a single year on data center and AI infrastructure. This illustrates how extraordinary the situation is.

AI Data Centers Are Like "Black Holes"

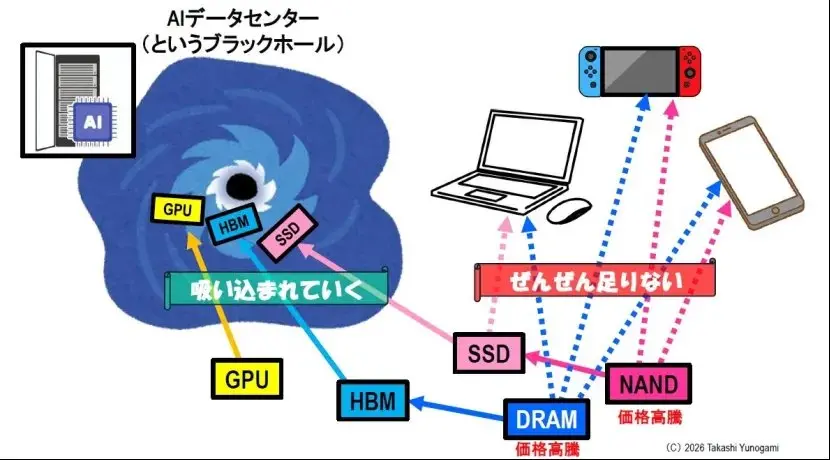

The ultimate destination of this massive investment is AI data centers. Figure 7 illustrates the current situation schematically.

As hyperscale data centers race to invest in AI data centers, the semiconductors essential for AI training and inference—namely, GPUs from companies like NVIDIA, the High Bandwidth Memory (HBM) used in those GPUs, and large-capacity storage SSDs equipped with NAND flash—are being sucked one after another into the "black hole" of AI data centers.

Memory manufacturers prioritize producing HBM, which offers high profit margins, and high-performance DRAM and NAND flash for data centers. This is a natural business decision. Consequently, production line capacity is diverted to the AI sector, drastically reducing the capacity available for other applications.

The industry most severely impacted is DRAM and NAND flash for digital consumer electronics like PCs, smartphones, and game consoles. Memory for these products is in severe shortage, to the point of being "completely insufficient."

With limited supply capacity, if demand is concentrated solely on AI data centers, memory for consumer electronics will inevitably run out. This leads to fierce competition for the limited supply, pushing prices higher. This directly correlates with the abnormal surge in memory prices mentioned earlier.

Indeed, PC and smartphone manufacturers have begun sending distress signals, stating they cannot obtain the memory they need, and procurement costs are skyrocketing, forcing them to pass these costs onto product prices. Ironically, in the shadow of the AI boom, the digital devices we use daily are becoming more expensive and even scarce.

Semiconductor Market Forecasts Are "Completely Wrong"

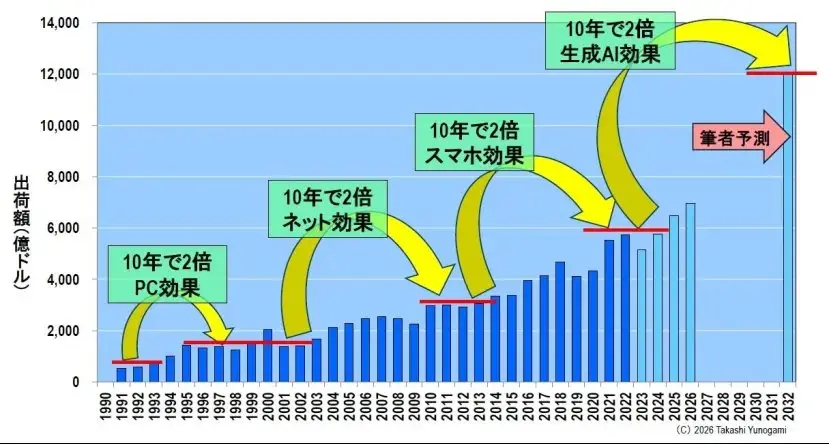

In 2023, I made a forecast for the global semiconductor market trend up to 2032, as shown in Figure 8. By analyzing the history of the semiconductor industry and incorporating the "PC effect," "Internet effect," "smartphone effect," and the upcoming "AI semiconductor effect," I predicted the market would grow at a rate of roughly "doubling every decade."

This forecast anticipated a market size of about $1.2 trillion by 2032. At the time, I considered this a fairly optimistic forecast.

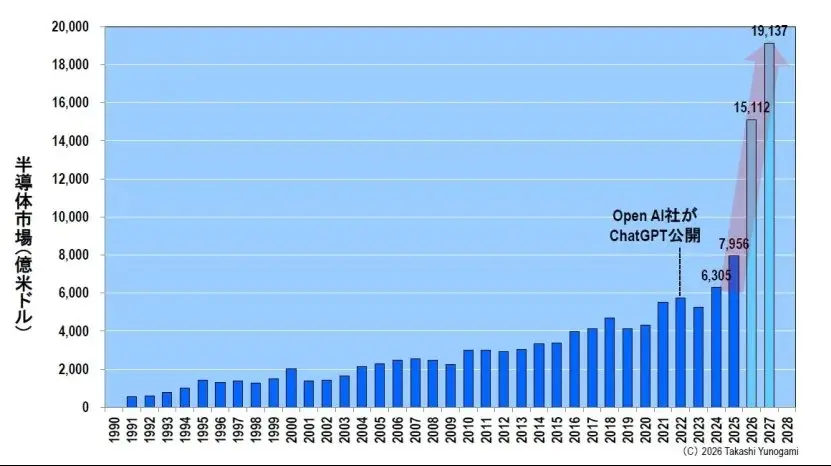

However, this forecast turned out to be completely wrong. In fact, it was wrong because it was too conservative. See Figure 9. According to the WSTS (World Semiconductor Trade Statistics) Spring 2026 forecast, the global semiconductor market size reached $630.5 billion in 2024, will reach $795.6 billion in 2025, and will break through $1.5 trillion to $1.5112 trillion in 2026. Furthermore, it is projected to grow rapidly to $1.9137 trillion by 2027, approaching $2 trillion.

In just a few years, the market size easily surpassed the $1.2 trillion level I previously forecasted for 2032. The 2032 forecast was realized in 2026. This doesn't mean the earlier forecast was "too optimistic"; rather, the disruptive power of the AI boom has completely overturned all previous conventions in the semiconductor industry.

Figure 10 clearly shows that this rapid growth is driven by Memory (including DRAM and NAND) and Logic (including GPUs). Memory is poised to break through $1 trillion by 2027, reflecting the explosive growth of DRAM+NAND discussed earlier. The Logic market is also expected to exceed $500 billion.

On the other hand, the Analog and Micro semiconductor areas have remained almost flat. In other words, the overall semiconductor market growth is not balanced; instead, only these two AI-related areas are growing at an unprecedented pace, pulling up the entire market. This is an extremely distorted growth structure.

How Long Will This Boom Last?

Now, let's answer the question on everyone's mind: "How long will the AI boom and the resulting growth last?"

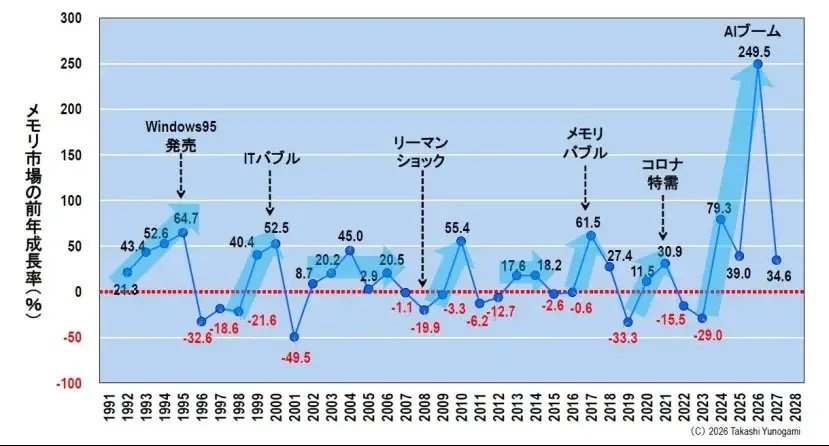

The key to understanding this lies in the long history of the memory market. Figure 11 shows the annual growth rate of the memory market over nearly 35 years since 1991. This chart reflects the countless ups and downs the semiconductor industry has experienced.

From the boom driven by the release of Windows 95 in 1995, to the IT bubble of 2000 and its subsequent burst, the memory bubble of 2017-2018, the Lehman Brothers collapse in 2008, and the boom during and after COVID-19 from 2020 onward, the semiconductor industry has been on a rollercoaster of boom and bust.

What deserves attention here is not the height of individual peaks, but the "duration" for which positive growth is sustained. Analyzing Figure 11 carefully reveals a crucial fact: in any historical period, the longest period the memory market has maintained an average annual positive growth is only five years. There has never been a case of six or seven consecutive years of positive growth in the past 35 years.

Why does the market plateau after five years? Because the memory market is inherently influenced by the "silicon cycle," which includes surging demand, price increases, companies increasing production investment, oversupply, and price collapse.

If the economy continues to boom, companies inevitably race to invest in equipment, ultimately leading to oversupply and a price crash. This is the inevitable operating mechanism dictated by the nature of memory as a product.

The current AI boom is expected to drive significant memory market growth, starting from the 2023 trough and peaking in 2024. According to historical patterns, this boom should end by 2028 at the latest, and possibly even peak by 2027.

While some will inevitably say, "This time is different" or "AI is special," we must not forget that the same was said during every past bubble economy.

The Higher the Peak, the Deeper the Valley

The history of the semiconductor industry also teaches us another undeniable rule: "The higher the peak, the deeper the valley that follows."

If you look at Figure 11 again, this rule becomes obvious. The IT bubble peaked in 2000 with an annual growth rate exceeding 50%, but was followed by a plunge to -49.5% in 2001. Similarly, the 2017-2018 memory bubble experienced a peak of over 60%, followed by a sharp drop of 33% in 2019. In this industry, the higher the peak of prosperity, the more severe and prolonged the subsequent recession tends to be.

Let's examine the current AI boom. A 285% annual growth rate is an unprecedented peak, far exceeding any previous bubble. Its rise is so high that the peaks of the IT bubble and the memory bubble pale in comparison.

Applying this principle, the conclusion is obvious. Following this unprecedented boom, the ensuing "valley" is likely to be far deeper and more severe than any previous downturn experienced by the semiconductor industry. We should prepare for an extremely severe recession expected to begin around 2027-2028, one that cannot be overcome half-heartedly.

Memory Manufacturer Stock Prices Soar and "Billionaires"

Currently, memory manufacturers' stock prices are soaring across the board. This is entirely expected, as rising prices have led to a dramatic increase in their profits.

A symbolic example is Kioxia. The company's rising stock price has made 600 investors, so-called "billionaires," realize over 1 billion yen in unrealized gains from their holdings. The entire industry is immersed in an unprecedented celebratory mood.

However, now is the time to stay calm. Stock prices are like a mirror reflecting expectations for the future. When those expectations are too high, if reality falls even slightly short, stock prices can crash instantly.

The higher the peak, the deeper the valley. This principle applies to stock prices as well, not just market size. In every past bubble burst, we've seen this scene: billionaires made rich at the peak of the bubble are forced to drastically sell down assets as the recession arrives.

Now, during the boom, is precisely the time to make solid preparations for the coming recession. This prosperity will not last forever. History shows that the memory market's positive growth lasts at most five years, after which a downturn follows (at least on the surface). The higher the peak, the deeper the valley. Therefore, I strongly urge the companies currently enjoying the boom: "While the boom continues, you should make solid preparations for the recession."