By: Liam Akiba Wright

Compiled by: Luffy, Foresight News

TL;DR:

- It is reported that Standard Chartered Bank has released a research report on Uniswap, setting a $100 price target for the UNI token by 2030.

- Standard Chartered's core logic is that tokenized assets will drive demand for open DeFi liquidity, and Uniswap is expected to capture a large volume of trades and earn transaction fees.

- However, most institutional-grade tokenized products are permissioned, and BlackRock's BUIDL product demonstrates that the DeFi sector still faces entry barriers.

Standard Chartered Bank has set a year-end 2030 price target for the UNI token at $100. This prediction suggests that the price of this leading decentralized exchange governance token will far exceed its current market valuation.

Standard Chartered's argument is that future tokenized assets will require decentralized trading platforms to convert fragmented on-chain financial instruments into tradable liquidity.

Standard Chartered estimates that by 2028, the global total value of tokenized assets could reach $4 trillion; and by 2030, the proportion of tokenized assets flowing into the DeFi market may increase from the current approximately 3.5% to 30%. Based on this projection, the DeFi market could hold over $2 trillion in assets by 2030.

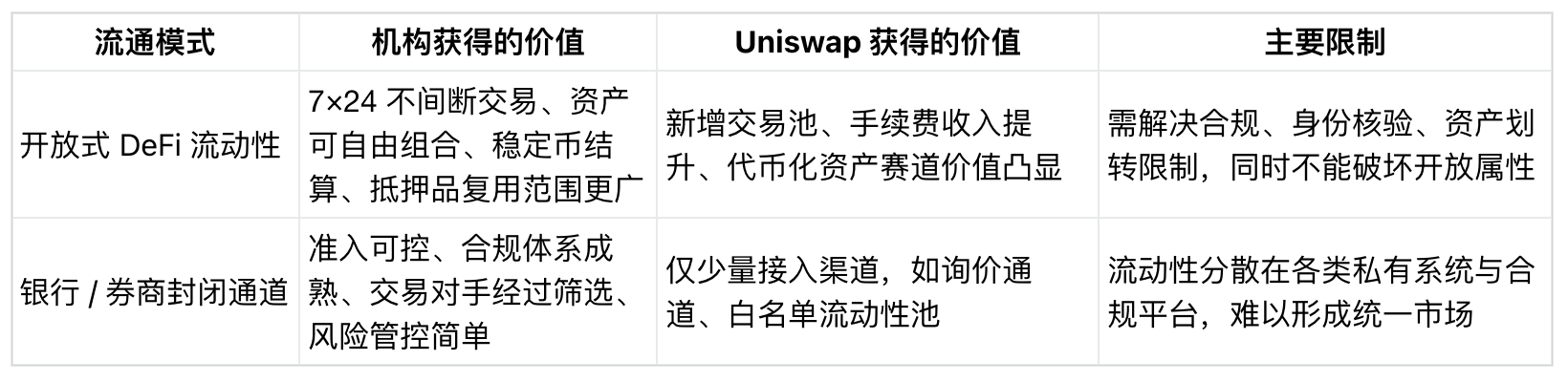

Currently, banks, asset managers, transfer agents, and compliant platforms are all entering the asset tokenization space. However, if these assets require 24/7 trading, flexible collateralization, and cross-product portfolio capabilities that a single institution's proprietary system cannot provide, then open, decentralized protocols will capture the liquidity dividend.

Within the current market environment, a core industry question emerges: Will on-chain assets such as tokenized treasuries, fund tokens, stock tokens, and stablecoins become liquidity instruments in open, decentralized markets, or will they remain confined to closed, strictly permissioned systems with fully controlled settlement and transfers?

Growth Prospects Depend on Open Liquidity

The valuation target set by Standard Chartered is built upon multiple layers of assumptions: First, the tokenized asset market achieves significant expansion. Second, a substantial portion of tokenized assets cease to be merely compliant, on-chain ownership records and instead become actively traded within DeFi markets. Finally, Uniswap can capture a sufficient share of relevant trading volume, driving up the value of the UNI token. The core of this entire logic shifts the focus from the asset issuance phase to the liquidity trading phase.

Standard Chartered had previously identified asset tokenization as a major long-term opportunity. In a 2024 report co-published with consulting firm Synpulse, the bank predicted that the global tokenization of real-world assets would reach $30.1 trillion by 2034, with trade finance being a core application area. The report also mentioned that tokenization would give rise to new DeFi applications and business models.

Citi's tokenization report from June 2026 presented a similar market size forecast but also highlighted countervailing factors: Its base case predicted tokenized assets would reach $5.5 trillion by 2030, with an optimistic scenario of $8.2 trillion. The report also noted that hybrid models might dominate, with institutions controlling issuance, distribution, and settlement channels.

The divergence between these two paths directly determines Uniswap's growth potential. If the scale of tokenized assets continues to grow but their value remains locked within bank platforms, transfer agent systems, brokerage networks, and compliant trading markets, the room for open DeFi development will be severely limited.

Conversely, if various tokenized financial instruments, stablecoins, and collateral assets require cross-category free trading, the status of protocols like Uniswap would rise significantly.

Data from DeFiLlama confirms Uniswap's foundation for meeting this demand. At the time of writing, the protocol's multi-chain Total Value Locked (TVL) is approximately $2.89 billion, with fee revenue exceeding $50 million in the past 30 days.

While existing data only represents the base operational scale, it is sufficient to illustrate that Uniswap's positioning is that of liquidity infrastructure.

For institutions, there is a clear operational difference between the two. Issuing a fund token is one process; building a trading venue where that token can be freely exchanged for stablecoins, collateral, and other tokenized assets is an entirely separate business.

The gap between these two processes determines whether automated market makers like Uniswap become essential infrastructure or merely peripheral access channels.

It is evident, therefore, that the choice of trading channel is as important as asset issuance. Liquidity determines whether tokenized products can form a tradable market, reusable collateral, and settleable assets; otherwise, they risk becoming static ownership certificates within compliant systems.

BlackRock's BUIDL: Connecting to DeFi, But Erecting Permissioned Gateways

BlackRock's BUIDL (BlackRock USD Institutional Digital Liquidity Fund) is a current real-world case highlighting this tension. In February of this year, Uniswap Labs and the compliant platform Securitize jointly announced that BlackRock's BUIDL fund would be accessible via the UniswapX trading channel.

This integration uses a Request for Quote (RFQ) mechanism and is only open to whitelisted users and pre-approved eligible participants.

Previous reporting by CryptoSlate on BUIDL pinpointed the core contradiction: While BUIDL holders can exchange for USDC via UniswapX, trading access is subject to strict permissioning.

The trading process leverages DeFi technology, but asset circulation is restricted to vetted institutional participants.

BlackRock's initial issuance rules for BUIDL fully embody this controlled model: The product is only for accredited investors, with a minimum investment of $5 million. Assets can only be transferred to pre-approved parties, and the fund is not listed on any exchange.

Data from RWA.xyz shows that as of June 16, BUIDL's total assets under management were approximately $2.37 billion, held by only 108 entities.

Combined with the permissioning rules, this illustrates the current state of the tokenization industry: large-scale tokenized products can emerge on-chain, but participation is highly concentrated and subject to full-cycle access controls.

Standard Chartered's investor roadshow materials from May 2026 also cited BUIDL's connection to Uniswap as a case study, arguing that decentralized platforms could be used for asset distribution and trading.

Even though the complete UNI valuation research report has not been made public, this roadshow material already categorized Uniswap as part of the institutional digital asset supporting infrastructure—the foundational support for the $100 price target.

The BlackRock BUIDL model sits between the two extremes: it utilizes Uniswap technology at its base but maintains full institutional permissioning controls throughout. This design builds a bridge to DeFi infrastructure without fully placing the tokenized assets into a permissionless, open liquidity pool.

It is highly likely that institutional asset liquidity solutions will initially adopt this hybrid model: leveraging DeFi infrastructure for trading and settlement while imposing strict controls on user identity, asset transfers, and counterparties.

UNI Still Lacks a Value Capture Mechanism

Even if Uniswap handles more real-world tokenized asset trading, it doesn't guarantee direct benefits for UNI holders. The protocol still lacks a stable value capture mechanism.

A previous UNI tokenomics upgrade proposal passed by the community on the Tally platform clarified protocol fee distribution and UNI burn mechanisms, while also proposing that Uniswap become the default trading hub for tokenized assets.

This plan provides a path for the valuation logic, but it depends on multiple prerequisites: community governance decisions, fee adjustments, institutional business partnerships, and growth in actual trading volume—all are indispensable.

The $100 price target given by Standard Chartered not only far exceeds current market prices but also surpasses UNI's all-time high from 2021. Achieving this target cannot rely solely on growth in asset issuance; it must be supported by real, sustained trading volume, stable fee income, and a clear mechanism linking protocol development to token value.

The core tension in the institutional tokenization space is that banks and asset managers need decentralized capabilities like on-chain settlement, 24/7 transfers, programmable collateral, and stablecoin payments, yet they simultaneously insist on KYC identity verification, asset transfer restrictions, designated counterparties, and maintaining control over secondary market strategy.

The Financial Stability Board's research report on tokenization also reflects this cautious stance. The report points out that the current overall scale of tokenization remains small, and the industry faces multiple challenges, including permissioned access, insufficient cross-platform interoperability, limited settlement assets, and fragmented trading venues.

These frictions are precisely the core obstacles preventing tokenized assets from becoming general liquidity instruments in DeFi.

If these industry barriers persist, Uniswap will remain merely a peripheral integration channel for institutional tokenization systems. If these pain points are gradually alleviated, the protocol could become the central trading venue where tokenized funds, stablecoins, and native crypto assets converge.

Ultimately, the core of Standard Chartered's valuation prediction depends on where tokenized liquidity ultimately flows. The $100 target represents significant upside potential. However, the more critical signal is that a traditional Wall Street investment bank has acknowledged that DeFi protocols have a chance to share in the institutional tokenization wave.

The BlackRock BUIDL case has proven that asset managers can use DeFi technology while maintaining strict circulation controls. Citi's outlook on the tokenization industry also suggests that Wall Street is likely to build hybrid systems, keeping issuance, distribution, and settlement firmly in institutional hands. Meanwhile, the various industry pain points raised by the Financial Stability Board highlight that interoperability and settlement systems remain core challenges.

Future market signals will come from more cases of tokenized asset integration. If new assets all adopt isolated, whitelisted RFQ channels, open DeFi will only capture a small market share. If cross-asset unified liquidity pools gradually materialize and custom control rules diminish, Uniswap's position in the tokenization space will no longer be confined to native cryptocurrency swaps.