也许 ETH 超越 BTC 比想象中的来得更早。

”“

比特币的目标是成为全球储备货币,以太坊的目标是成为全球数字经济的基础设施。这两个愿景都是巨大的,所以比较网络获得各自市场份额的可能性会更好。

”“

相对于其安全预算,比特币从未产生过有意义的交易收入,而是用区块奖励来大量补贴安全。目前的模式是不可持续的,削弱了其成为全球储备货币的可能性。

”“

以太坊已经成为最大的 dApp 生态系统的基础层,并拥有加密货币中最好的经济系统。

”“

该网络目前拥有:246 亿美元的 DeFi TVL;847 亿美元的稳定币。

”“

在 2022 年,它促成了超过:1.2T 美元的 DEX 现货交易量;526 亿美元的 NFT 交易量。

”“

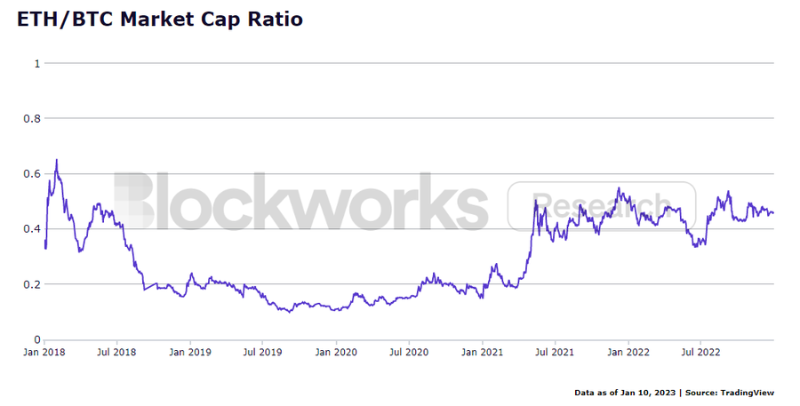

我预计以太坊将在下一个周期结束前超过比特币。以太坊的市值落后大约 $1500 亿,但合并后的出色表现将成为 ETH 基本面的一个有实力的推动力。

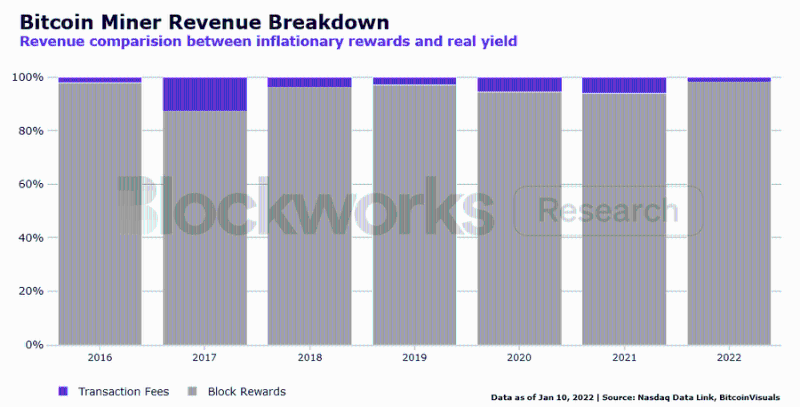

如果只看矿工收入的美元价值,比特币似乎做得更好。

”“

自 2016 年以来,矿工年收入一直呈上升趋势。

”“

但分析一下收入构成,就会发现背后的问题......比特币通过区块奖励大量补贴安全性。95%的比特币矿工奖励来自通货膨胀的区块奖励,而只有 5%是来自交易费的真实收入。

PoW 在设计上会消耗大量能源。这对安全来说是很好的,但它创造了强制卖家,因为矿工需要抵消他们的生产成本(电力)。即使通货膨胀率较低,95% 的矿工销售都是新铸造的 BTC,因为几乎没有产生费用。

”“

比特币不支持智能合约,所以 BTC 是网络上唯一可以存在的价值形式。用户必须在每笔交易中支付费用来转移 BTC。因此,费用产生依赖于 BTC 的流通速度,但用户却自称是囤币者……

”“

相比之下,ETH 是作为货币在数字经济中进行交易的。用户支付 ETH 来转移 ETH、稳定币和其他代币,或与 DeFi 应用程序互动。以太坊扩展了可能的行动,不仅仅是发送、接收和持有 BTC。

”“

在牛市期间,以太坊的真实收益百分比与总收入一起增加,凸显了网络的反身性。然而,当链上活动减少时,反身性就会受到伤害,这从 2022 年真实收益百分比的回撤可以看出。

”“

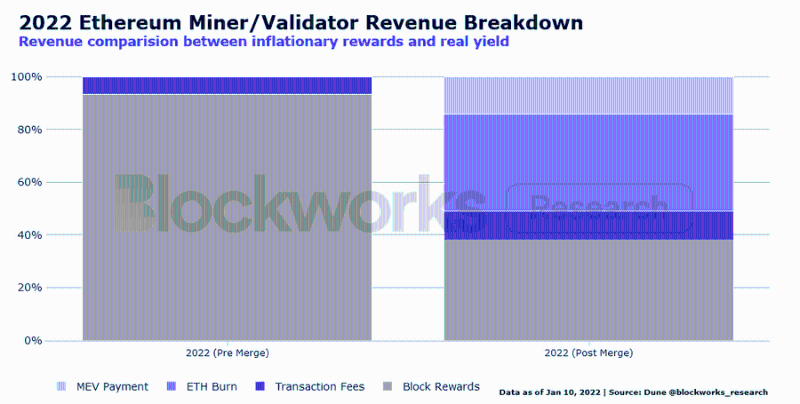

将 2022 年分为合并前和合并后的时代,显示了以太坊如何通过验证者收入的多样化来解决通货膨胀问题。合并后,以太坊验证者从交易费、ETH 燃烧和 MEV 支付中获得 62%的实际收入。

ETH 燃烧和 MEV 也与链上活动的水平相关。更多的交易量导致了更高的基础费用燃烧和更多的 MEV 机会。然而,在熊市,以太坊的净发行量近乎为零,并为质押者创造了正价值。

”“

迁移到 PoS 也导致在短短 117 天内减少 17 亿美元的 ETH 排放量。这对流动性流动来说是很重要的,因为 ETH 需要更少的购买压力来维持相同的价格。对通胀的影响?ETH 的 30 天年化通胀率高达 0.00%。

”“

同样,比特币并没有死。它在 2021-2022 年被个人、上市公司和国家/地区广泛采用。它的社区可能会在不久的将来努力优先考虑可持续性,但它目前的发展轨迹将导致它相对于以太坊而言滞后。