1. BTC releases the strongest trading volume

After the BTC price recovered and rebounded from the adjustment, the price easily reached above the middle rail of the brin line, rebounding from $18799 to around $22400, with a range increase of 19.2%. From the performance of trading volume, the effect of this 7 trading days is obviously better than the performance of the past 2 months, and it is also the largest average trading volume performance in the past year. Therefore, the week before the Federal Reserve raised interest rates on September 22, BTC is showing stronger rebound expectations. The recent BTC growth space depends more on the position that the trading volume can reach. The overall market will rebound in large quantities to reduce the selling pressure, and the impact of short-term selling pressure changes on the market is very important.

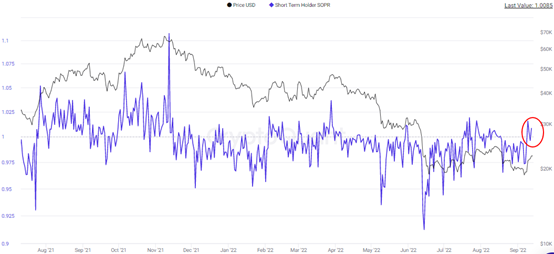

2. BTC medium and short-term investors' profit flight

The profit flight of BTC's medium - and short-term investors shows that investors are facing the opportunity of reducing their positions. The SOPR index has been running above 0 since September 9, which indicates that investors have made profits as a whole. During BTC trading, the nature of trading is profit flight. In the next trading day, with the increase of BTC rebound space, expected profit trading will still dominate the overall market. Therefore, when judging the market trend, the higher the SOPR index can reach, the greater the short-term selling pressure it will prompt. Referring to the SOPR index that can be reached in the past year, when the index is in the range of 1.05 to 1.1, it can effectively test the effectiveness of selling points.

3. The unrecognized loss of BTC decreased significantly

With the emergence of the rebound trend, the unconfirmed loss scale of BTC has dropped significantly, from the recent high of 0.507 on September 6 to around 0.353, and the loss scale has decreased by 15.4 percentage points. This shows that after the rebound trend of BTC in the past week, a considerable number of loss making orders have disappeared, which means that the selling pressure is also dropping rapidly.

In terms of absolute value, the proportion of unconfirmed losses on September 12 still reached 35.5%, which is still at a high level compared with the past two years. Therefore, BTC is still in the interpretation of digesting selling pressure, and we can pay further attention to the pressure level in the rebound.

4. Eth price rebounded slightly

With the volatile trend of eth, the recent overall increase has not exceeded expectations. It can be seen that the ETH price trend shows a certain deviation from BTC, which indicates that the strength of the overall market may not last too long. In terms of trading volume, the daily K-line trading volume of eth is still shrinking, so the increase is not ideal. However, considering the large growth space of eth in the previous period, the advantage in terms of cumulative growth is still significant.

5. Eth transfer volume rebounded slightly

During the recent eth rebound, the number of transferred eth rebounded slightly, but it did not exceed the previous peak. From the rebound strength, it reached 3.773 million on September 6, lower than 4.857 million eth on July 21, and lower than 8.156 million and 7.569 million eth on May 12 and June 13. Therefore, the ETH price is still in a stable operation stage. The trading enthusiasm of investors has not changed, and the expectation of increase has not been strengthened.