一直以来,仍处于起步阶段的 DeFi 往往会遭受「脆弱性」的诟病,循环贷等高杠杆行为也加剧了这一问题。

DeFi 的发展往往与大的加密市场周期有关。不可否认,在上行周期中,加杠杆的行为会推动价格等进一步上涨,但在下行周期中,杠杆会成为投资者的灾难,毫不留情的清算将为市场带来毁灭性的打击。

到如今,在市场消除杠杆之后,链上 TVL 又回到了 DeFiSummer 之前的原点。显然,下一个十字路口已然来临,DeFi 协议未来将会如何发展?

首先,我们不妨先从 DeFi 代币的价值捕获开始。

一、哪种 DeFi 代币经济模型更具优势?

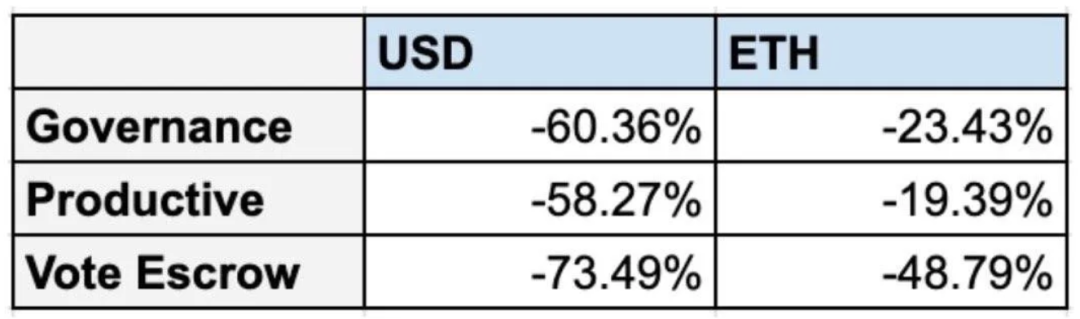

一个很有趣的数据是 Crypto Twitter 中有人统计了不同经济模型的 DeFi 代币在今年初到现在的表现。其中,表现最好的是 Productive 代币,也就是具备生产性质的代币。

用一个更易于理解的说法就是,Productive 代币都与协议业务相关,有明确的赋能。而 Governance (治理)和 Vote Escrow(投票托管) 代币的应用方向都是协议治理层面——尽管以 Cruve 为首的 ve 代币模式深受很多链上用户的喜爱,ve代币模式在一定程度上也降低了代币整体的流通量。

不过随着时间的推移,ve 代币模式会出现大量的代币排放,Curve目前每天向该协议的流动性提供者分发超过 100 万 CRV。

从代币的可持续性发展层面来讲,生产性代币在未来发展中更具优势。

生产性代币背后的协议往往是拥有真实收入的 DeFi 协议,而这种拥有产生真实收入能力的 DeFi 协议正在引导新的趋势出现。

二、什么是真实收入?

最近,“Real Yield” 是 Crypto Twitter 上的热门词汇,顾名思义,指哪些能产生真实收益的 DeFi 协议,而不是从代币发行中获得收益。

对于这个概念,推特博主 TheDeFiedge 的定义是:

1)产品/市场契合:无论市场条件或代币激励如何,人们都在使用该协议。

2)该协议通过其产品产生链上收入。

3)收入>运营费用+代币排放:只要协议的收入较高,有一些代币排放是可以承受的。

4)他们是否用稳健的货币与代币持有者分享收益:最受欢迎的选择是 ETH 和稳定币。

我们可以以 Synthetix 为例:

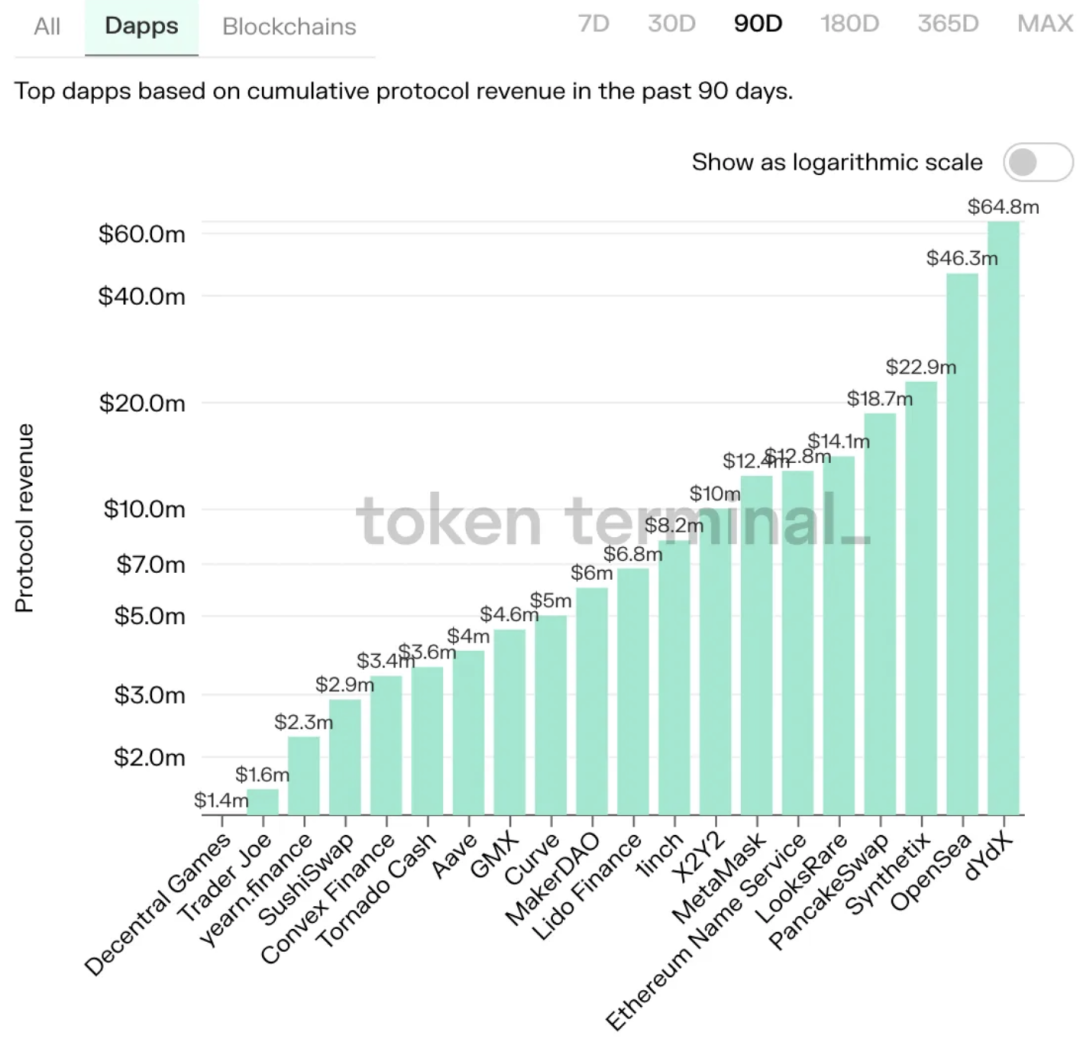

据 Terminal 数据显示,在过去三个月的时间中,Synthetix在所有 DAPP 收入排名中排第三位,创造了超过 4600 万美元的收入——对于一个「之前被人诟病日活只有几个人的DeFi协议」而言,在熊市中逆势发展,这简直就是一个奇迹。

让我们来看看 Synthetix 是怎样做到的。

Synthetix 是一个去中心化合成资产发行协议,允许在没有原始资产支持的情况下创建合成资产 Synths,我们可以通过合成资产来追踪现实世界/加密世界中任何拥有价值的资产(加密货币空头头寸、美元、股票、黄金、石油等等)。而所有的合成资产都需要由 Synthetix 原生代币 SNX 作为抵押,在进行合成资产大额交易时,鲸鱼们可以享受几乎为 0 的滑点。

Synthetix 逆势翻盘的原因在于 Synthetix 团队一直在基于市场发展和变化,对协议进行整改和升级。

此次爆发,主要基于 Synthetix 团队所做的两方面努力:

提案 SIP-120 的实施:将原本合成资产交易从 10 分钟结算时间调整成即时原子交易。

被 1inch 等聚合 DEX 集成——Synthetix和Curve的交易链路的低滑点成为了最优路线(Uniswap被跳过了)。

如果我们想要用 USDC 购买 ETH,那么链路就成了:

USDC->sUSD (Curve 提供低滑点)

sUSD->sETH (Synthetix 提供 0 滑点)

sETH->ETH (Curve 提供低滑点)

在成功内卷 Uniswap 后,Synthetix 还将协议收入分享给了 SNX 质押者。因此,SNX 质押者虽然会受到全局债务(Synthetix 的另一特点,SNX 质押者是任何使用 Synthetix 提供的合成资产交易者的对手方,意味着你的债务头寸可以增加或减少)的影响,但协议收入的分享也让很多 DeFi 用户愿意将 SNX 质押在协议当中。

目前已经有协议可以帮助这些用户对冲债务变化的风险,SNX 质押者完全可以对冲风险,并拿走 Synthetix 协议分红。

除了 Synthetix,还有哪些捕获真实收益的协议?

GMX ,一个建立在 Arbitrum 和Avalanche上的去中心化的合约交易所,最高可开 30 倍杠杆,GMX 也会将交易和杠杆交易的手续费的 30%兑换成 ETH/AVAX,分发给 GMX 代币质押者。

Gains Network ,建立在Polygon上,其推出的 gTrade是一个拥有高效流动性、功能强大的去中心化杠杆交易平台,加密货币最高可开 150 倍杠杆,外汇最高可开 100 倍杠杆,股票最高可开 100 倍杠杆。当其 DAI 保险库余额超过其 TVL 的 130% 时,将开启购买和销毁机制,

Trader Joe ,Avalanche上排名第一的 DEX,将 JOE 质押成 sJOE 可获得稳定币’USDC’奖励。

三、未来 DeFi 世界中怎样的协议才能可持续性发展?

会是真实收入协议吗?

我们在上文图中看到的收入第一、第二、第四的协议 dYdX、Opensea、PancakeSwap 都属于真实收入协议。但是问题在于,它们或是没有代币,或是代币没有协议相关业务的赋能。

本质来讲,如果代币没有赋能,协议便无法拥有强大的护城河——对用户更友好的协议会争夺该协议用户,进而取代之。

在这种情况中,生产性代币将会成为协议的护城河,持续吸引用户的关注力和购买动力,与用户进行价值共享。dYdX 团队也计划在 2022 年底推出的 V4 中改变代币赋能缺失的情况——提升代币的价值捕获能力已经变成了DeFi世界中的重要趋势之一。

拥有真实收入代表着协议在 DeFi 生态中的竞争力,也是支持团队继续发展的源动力。生产性代币将会成为协议的护城河,与用户分享协议捕获价值。

而这两点,将会在帮助 DeFi 协议在面对高波动的市场时发挥重要作用。

以上内容,我们都是在聊价值捕获的逻辑和 DeFi 协议们未来发展趋势,而随着时间的推移,更多有想法有竞争力的内容也开始逐步显现,DeFi 行业也会向前发展。至于 DeFi 是否会取代 CeFi,本文不做讨论。更有可能的未来是,DeFi 和 CeFi 会互相融合,各自完成自己擅长的那部分——以达到更好的资本效率。