Author: Jae, PANews

Following its bullish call on UNI, Standard Chartered Bank has made another bold statement to the crypto industry: AAVE could surge 50-fold by the end of 2030, reaching $3,500.

Related reading:Standard Chartered Opens 40x "Bet," Calls for UNI to Rise to $100

Aggressive rhetoric, exaggerated multiples, coupled with a familiar script: AAVE’s price surged past $80, with 24-hour gains once approaching 20%. The on-chain lending market is in an uproar—some cheer the traditional giant’s bullish stance on AAVE, while others mock Standard Chartered as another sell-side entity carried away by hype.

Aave’s next battle will unfold at the intersection of fantasy and reality.

Standard Chartered Uses Excel to Draw a 50x "Candlestick" for AAVE

If one were to condense Standard Chartered’s AAVE research report into one sentence, it would be:Deposit scale determines lending capacity, lending capacity drives fee income, and fee income ultimately translates into token market capitalization. Over the past 12 months, approximately 90% of Aave’s fee revenue came from the net interest spread between deposits and loans.

The traditional valuation framework based on linear mapping logic has been directly applied by Standard Chartered to the lending protocol. According to its pricing model, AAVE will follow a stepwise upward trajectory.

Standard Chartered’s assumptions stem from predictions about two major trends in the DeFi sector:

-

DeFi TVL (Total Value Locked) will grow 37-fold. Standard Chartered predicts that by 2030, the total value of active assets in DeFi will grow 37 times from current levels, reaching approximately $2.7 trillion. This will be driven by a $2 trillion expansion in stablecoin scale and the massive wave of on-chain migration of RWAs (Real World Assets).

-

RWA penetration in DeFi will increase from 3.5% to 30%. This means trillions of dollars in traditional assets will flow into on-chain lending protocols.

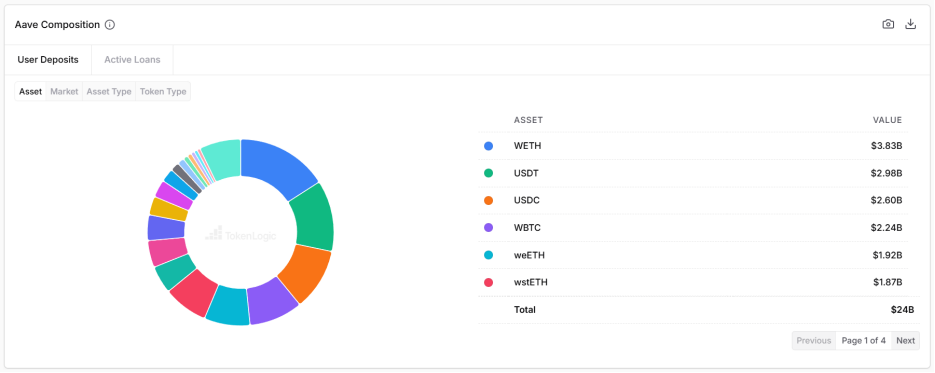

Looking back at its peak in October last year, Aave once managed deposits as high as $75 billion. If viewed as a traditional bank, this scale would place it among the top 35 banks in the United States.

Standard Chartered believes that Aave’s operational efficiency far surpasses that of traditional banks reliant on physical branches and redundant manpower. Once the tokenization wave arrives, Aave will leverage its Horizon permissioned lending market and the fee capture from its stablecoin GHO to convert the benefits of RWA on-chain into tangible protocol revenue.

Regarding the capital outflow triggered by the KelpDAO rsETH bridging security incident in April, Standard Chartered Bank characterizes it as a short-term fluctuation during the bottoming phase, not a collapse in the long-term protocol fundamentals.

Even setting aside the long-term narrative and focusing on a medium-to-short-term perspective, Aave’s fundamentals remain robust enough.

On June 18, Grayscale released an in-depth report on Aave, applying the traditional finance DCF (Discounted Cash Flow) model and P/E (Price-to-Earnings) ratio method to value a DeFi protocol for the first time.

Grayscale concluded:AAVE is a typical cash-flow-driven asset, currently trading at undervalued levels.

Grayscale emphasized that Aave’s full-year protocol revenue for 2025 was as high as $142 million, indicating healthy cash flow. More importantly, the token buyback and burn plan launched by Aave DAO in April last year, as well as the "Aave Will Win" proposal’s shift of product revenue to token holders, have institutionally established the transmission path from "protocol revenue generation → token value appreciation.”

Monopolizing 80% of Profits with Half the Sector's TVL, Idle Funds Remain Its Achilles' Heel

Beyond the macro vision painted by institutional capital, Aave has also built a deep moat at the micro level.

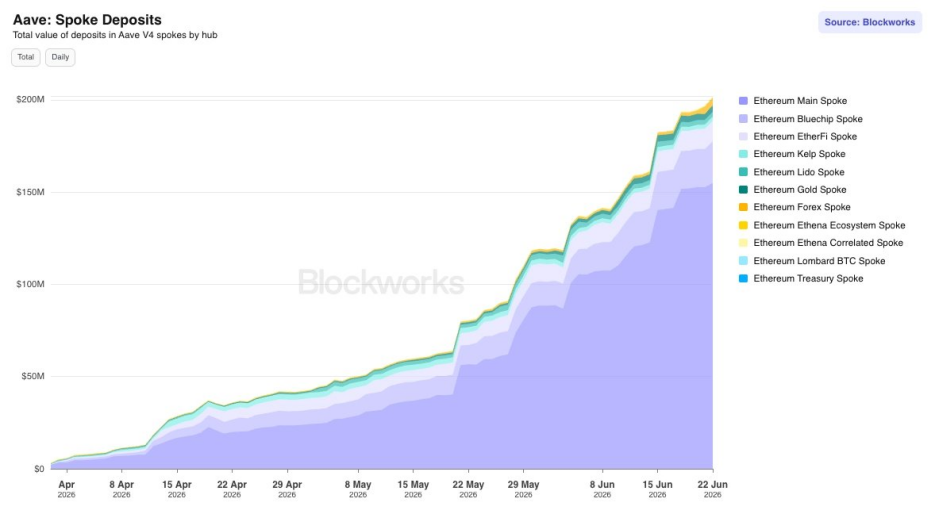

First, there is the breakthrough of the new-generation technical architecture, Aave V4. As the largest underlying architecture rewrite since the protocol’s inception in 2020, V4 employs a "liquidity hub-and-spoke" design to break the silo effect of single-chain liquidity. To date, V4’s total deposits have surpassed $200 million, with loan volumes nearing $60 million.

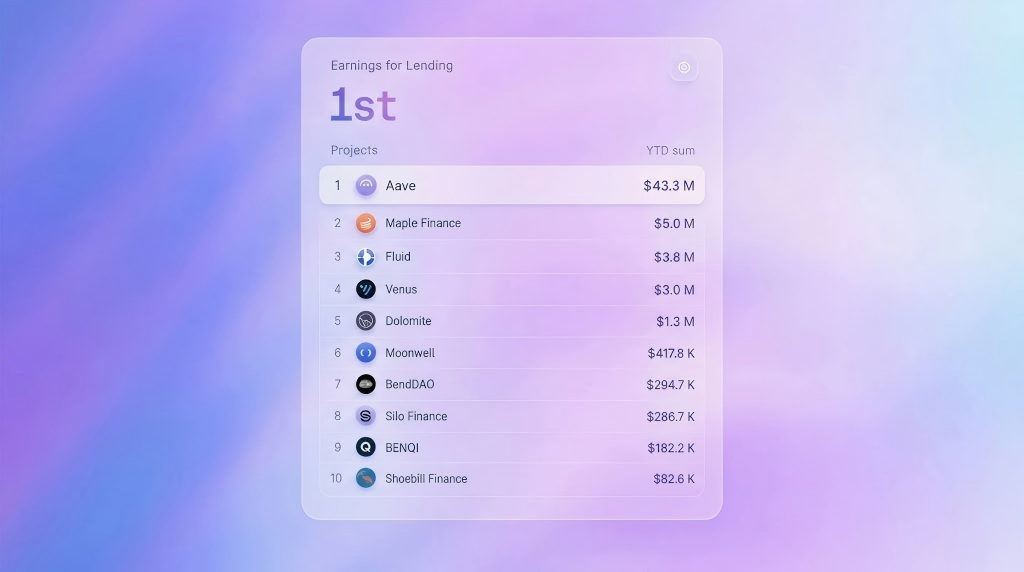

More remarkable is its profitability. On-chain data analytics firm MSB Intel pointed out that year-to-date, Aave has accumulated approximately $43.3 million in "protocol retained earnings" within the lending sector, accounting for 80.7% of the entire sector’s profits. Protocols like Maple Finance, Fluid, Venus, ranked behind it, each generating less than $5 million in profit, not on the same scale as Aave.

In the traditional business world, a company’s substance is often determined by net profit, not total assets. Retained earnings are an indicator that, after deducting relevant operational costs and token inflation incentives, truly reflects a protocol’s on-chain net revenue generation capability.

In other words, Aave uses roughly half of the sector’s TVL to capture over 80% of its net profit. This near-monopolistic profit structure is the hardest cornerstone in Standard Chartered’s 50-fold prediction.

On the flip side, the structural flaw once highlighted by crypto research firm Delphi Digital remains an unresolved challenge. The root of the problem lies within Aave’s peer-to-pool lending model.

According to Delphi Digital’s estimates, in the three primary markets of WETH, USDT, and USDC, Aave incurs an annual invisible loss (Deadweight Loss) of approximately $52 million due to idle funds, a scale almost equivalent to half of its annualized net revenue for Q1 2026.

The systemic disconnect between deposit and borrowing rates is an inherent defect of the peer-to-pool model. To ensure depositors can redeem their funds at any time without loss, Aave must maintain a massive idle liquidity buffer within its pools. This results in depositors receiving rates typically 25% to 35% lower than what borrowers pay. The difference is the opportunity cost of idle funds. Even if the DAO governance layer sets the reserve factor to 0, the invisible loss from idle funds would still be as high as $36 million.

The KelpDAO incident in April further revealed the fragility of this model. After hackers drained nearly $200 million worth of WETH, the WETH pool utilization rate was locked at 100% for five days. Ordinary depositors could neither withdraw nor participate in liquidations, leaving a scar on Aave that has yet to fully heal.

This structural flaw makes Aave susceptible to "upstream risk" contagion. Coupled with the inherent shortcoming of low capital efficiency, it also gives latecomers an opportunity to break through. Emerging lending protocols like Morpho, focusing on modular isolation, peer-to-peer matching, and minimalist underlying design, are encroaching on Aave’s market share from an efficiency standpoint, becoming its most formidable challenger beneath the throne.

Looking back from the midpoint of 2026, Aave stands at the corner of fantasy and reality.

The "$3,500" pie chart drawn by Standard Chartered Bank reflects traditional finance’s ambition for asset tokenization. Beyond mere TVL growth, Aave’s future focus will be on finding a viable path to support a trillion-dollar asset scale.

The throne of DeFi lending remains, but the foundation beneath it still requires a process of reconstruction or reinforcement.