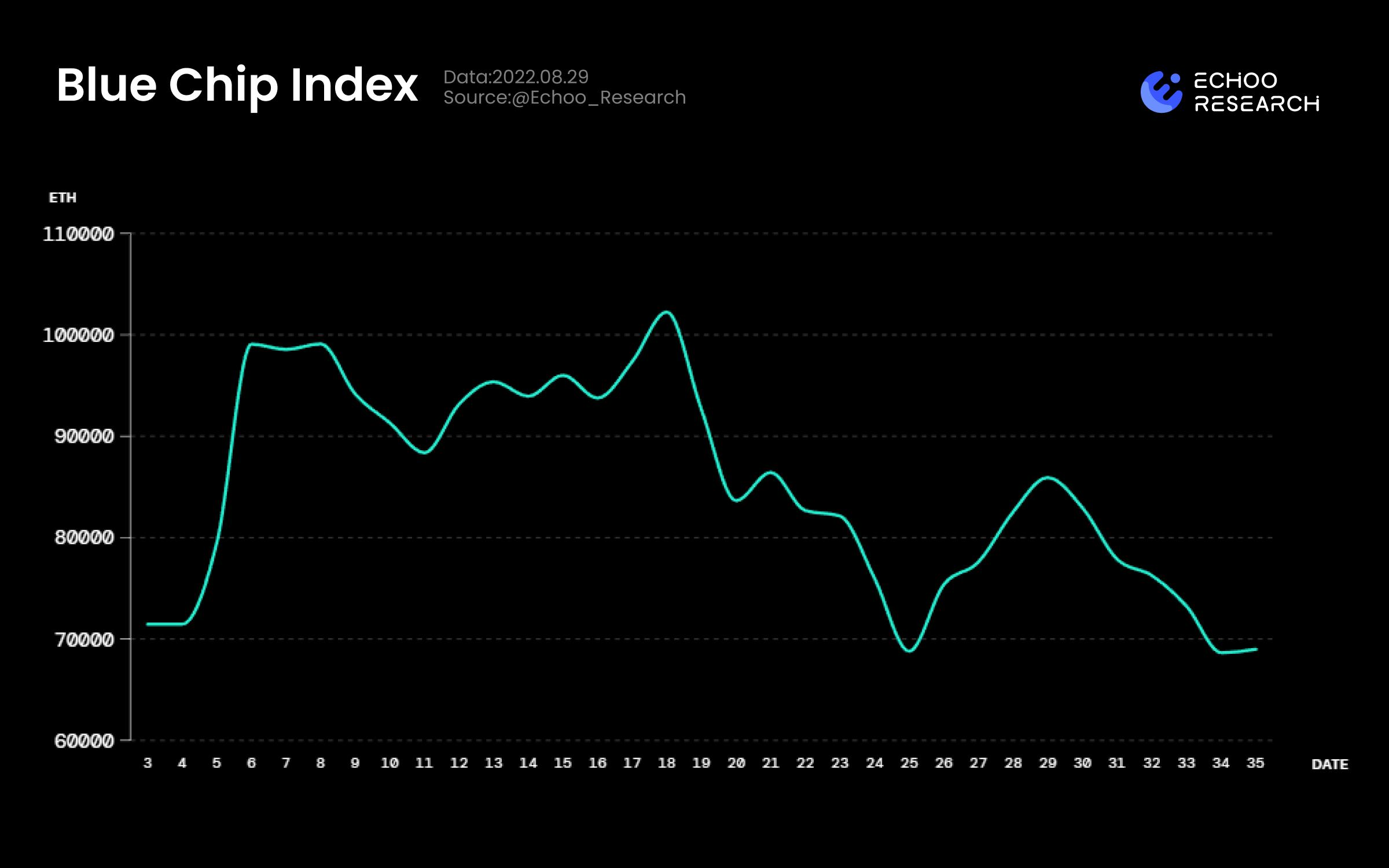

蓝筹NFT指数连续5周下跌后,在今年的最低值附近得到暂时的“支撑”,与此同时,我们也看到大部分蓝筹的价格都有较明显的反弹。

本周市场趋势

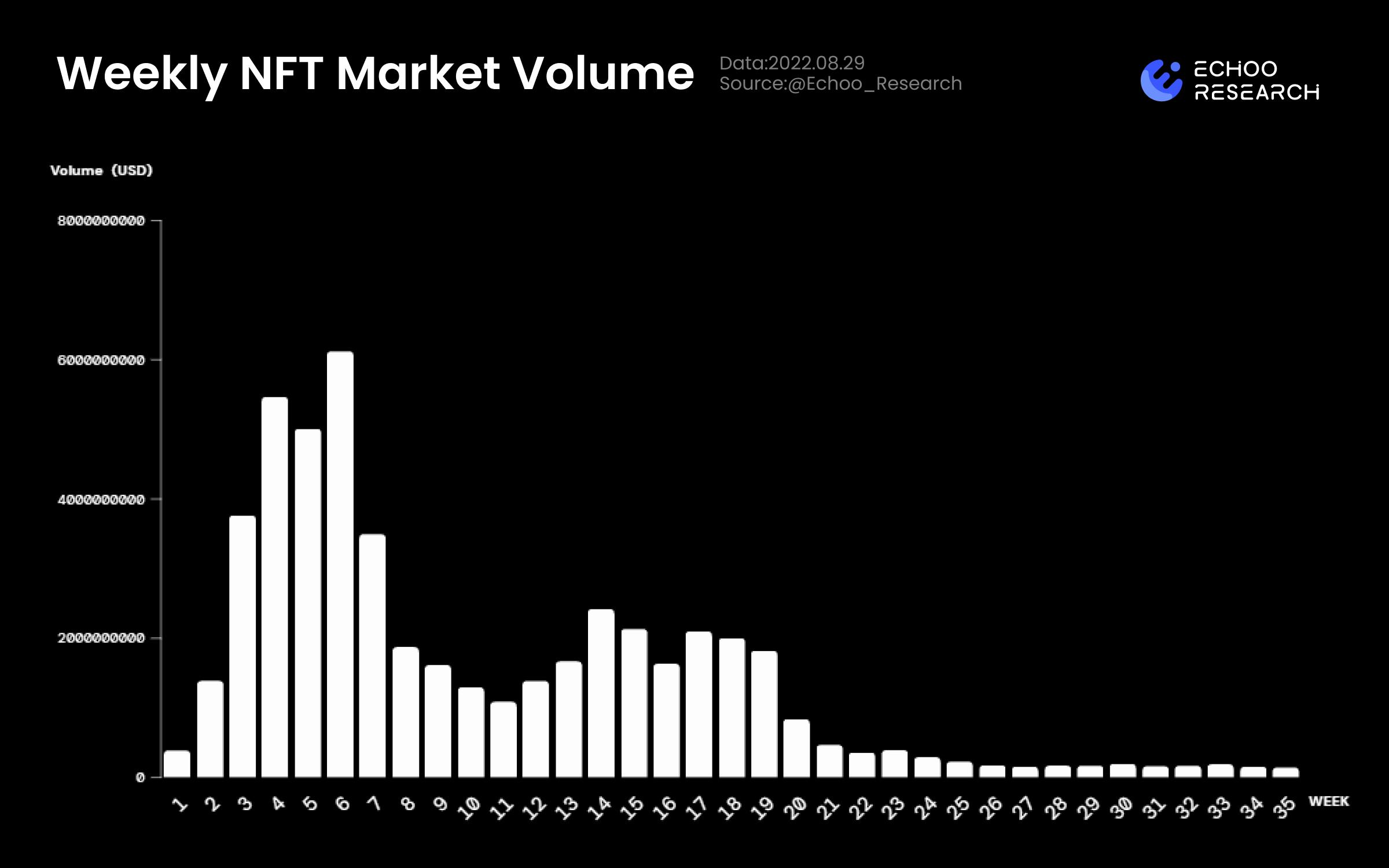

Weekly NFT Market Volume

最近两周加密市场迎来了整体下跌,BTC的价格从$25000跌至$19500,跌幅达20%,ETH也从2000跌至1400,跌幅接近30%。

NFT市场相比于传统加密市场并没有好转,本周NFT交易量较上周再次下降9%,已经到达今年的最低区间。我们不能确定现在是否为NFT市场的底部,可以肯定的是“现在是今年NFT市场最不活跃的时期”。

从较大的时间跨度上来看,整个NFT市场的交易量依然徘徊在较低区间,并没有强势反弹的迹象。

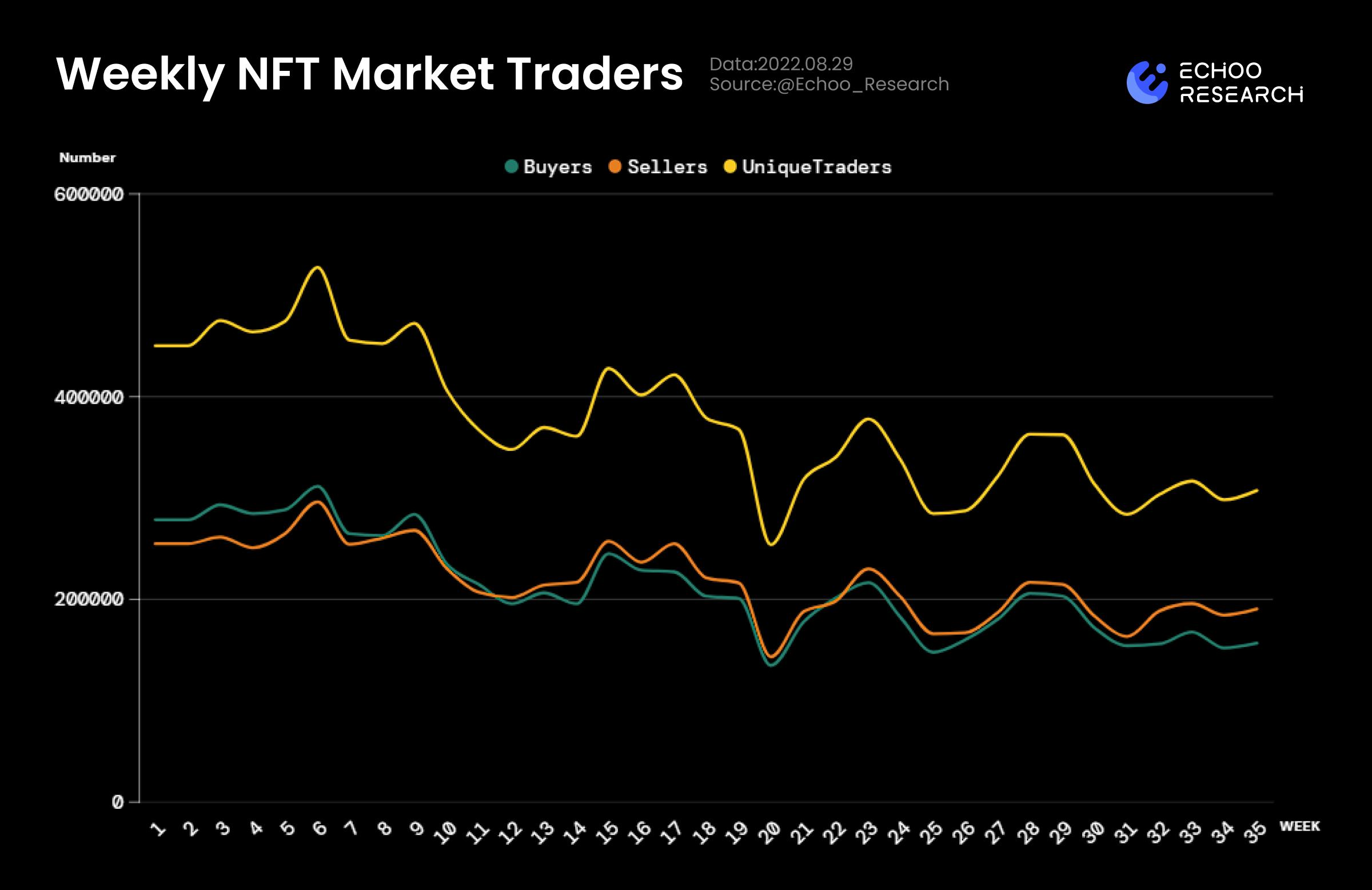

Weekly NFT Market Traders (Source: echoo.substack.com)

本周参与交易的人数较上周变化不大,市场的下跌并没有造成“抄底”人数的上升,反而买卖的净值差有扩大的趋势,交易的总人数区间也开始逐渐收敛,这证明市场上参与交易的人正在变少,大多数交易者处于“观望”态度。

其次卖出者比买入者多1.2倍,这证明目前市场上大多数更倾向于“卖出”。

Blue Chip Index (Source: echoo.substack.com)

蓝筹NFT指数连续5周下跌后,在今年的最低值附近得到暂时的“支撑”,与此同时,我们也看到大部分蓝筹的价格都有较明显的反弹。

在上周我们给出的建议和买入信号都得到了成功验证,另外最近较火的NFT如DigiDaigaku、Pudgy Penguins等,Echoo也均在周报中提前给出了信号。

值得注意的是,目前的反弹力度相比于25周较小,而且有走平的趋势,再加上整体市场的不景气,如果有想长线投资NFT的朋友需要耐心等待更强烈的反弹信号出现。

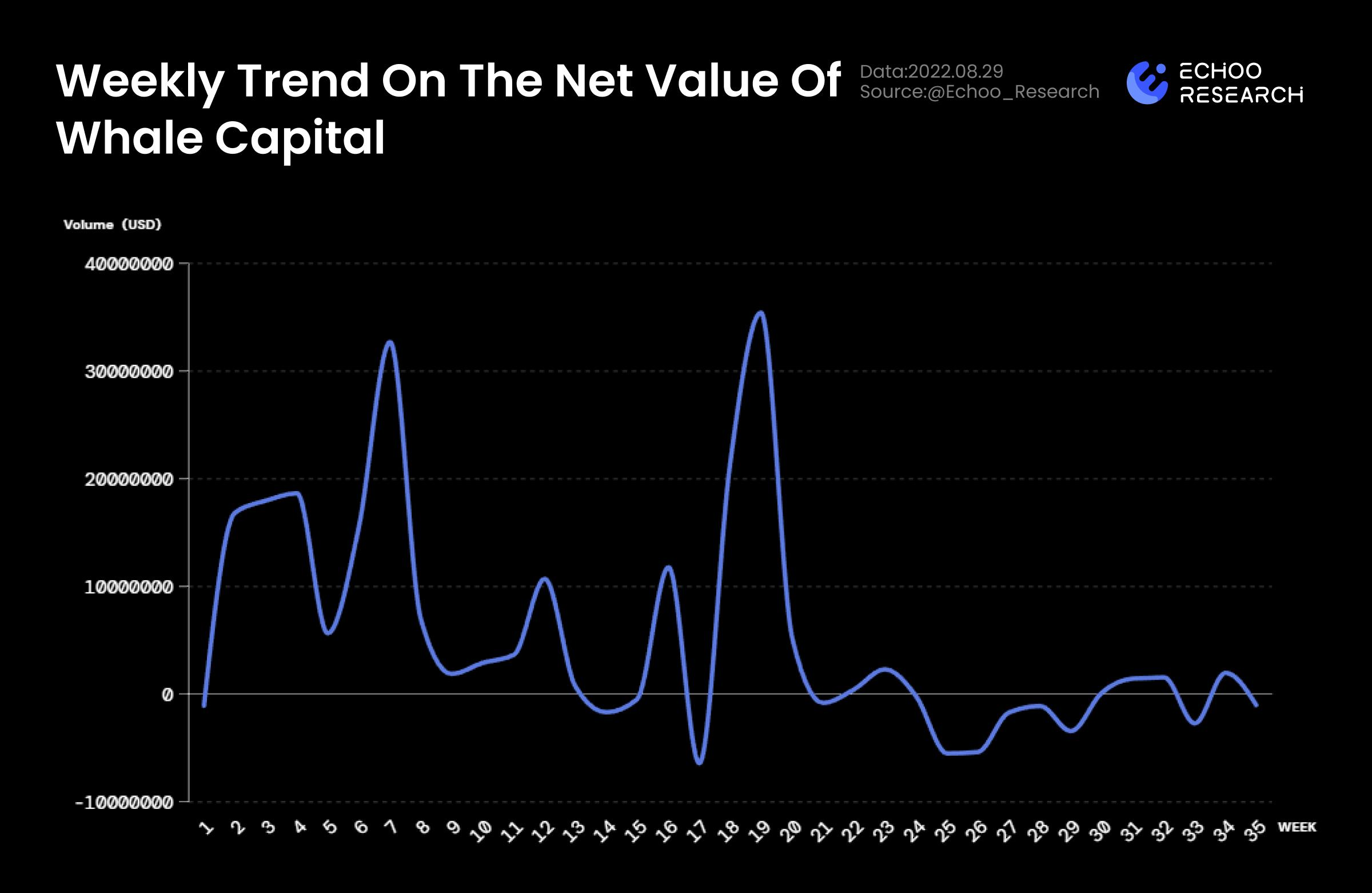

Weekly Trend On The Net Value Of Whale Capital (Source: echoo.substack.com)

在本周,巨鲸流入资金但再次转为负值,并且波动越来越小,大部分的巨鲸正在“离场”。

虽然巨鲸的行为相比于NFT市场具有提前性,但在目前市场整体交易量萎靡时,巨鲸的整体流动资金规模仍然较低,这代表了巨鲸更倾向于小资金规模参与NFT投资。

这也像我们多次强调的:当前NFT市场受到巨鲸的影响很微弱,更多的是散户在主导交易。

指数信号

1.巨鲸上周抄底的NFT

下表为巨鲸的买入前20名NFT,详细的购入数量及平均成本如下:

NFTs Bought By Whales In The 35th Week

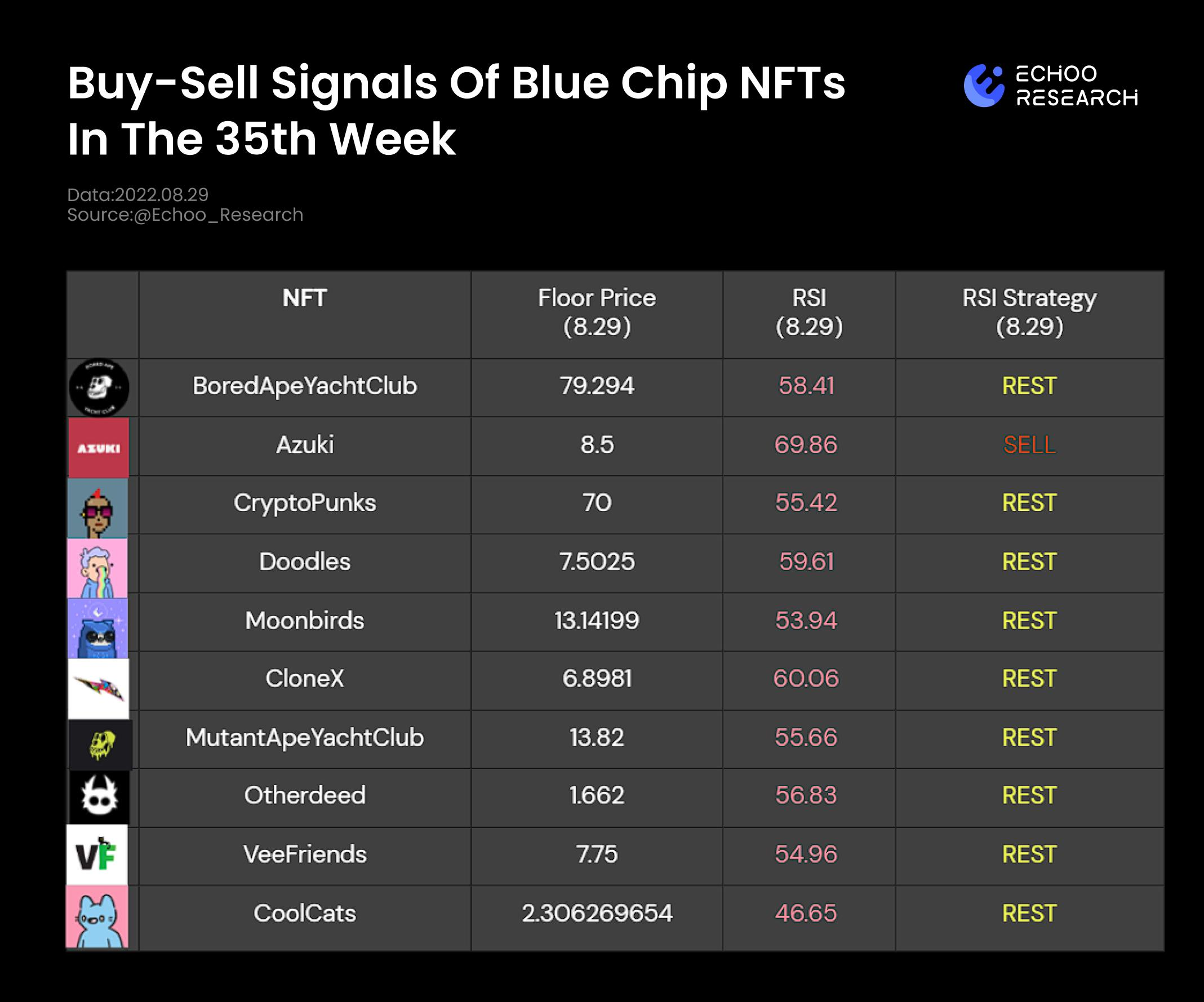

2.蓝筹的NFT买卖信号

本期Echoo Research为大家提供的指标是蓝筹的NFT买卖信号,对于买卖行为具有一定的参考性。

Buy-Sell Signals Of Blue Chip NFTs In The 35th Week

上周绝大部分蓝筹价格触发了买入信号,在反弹后大多数蓝筹NFT价格波动变小,出现了“不操作”的信号。

指标说明

RSI Strategy:根据RSI的买卖相对强弱的特性而设计的买卖信号。

简单使用方法:在波动区间下方为买入信号,在波动区间上方为卖出信号,偏离度越大信号越强烈。

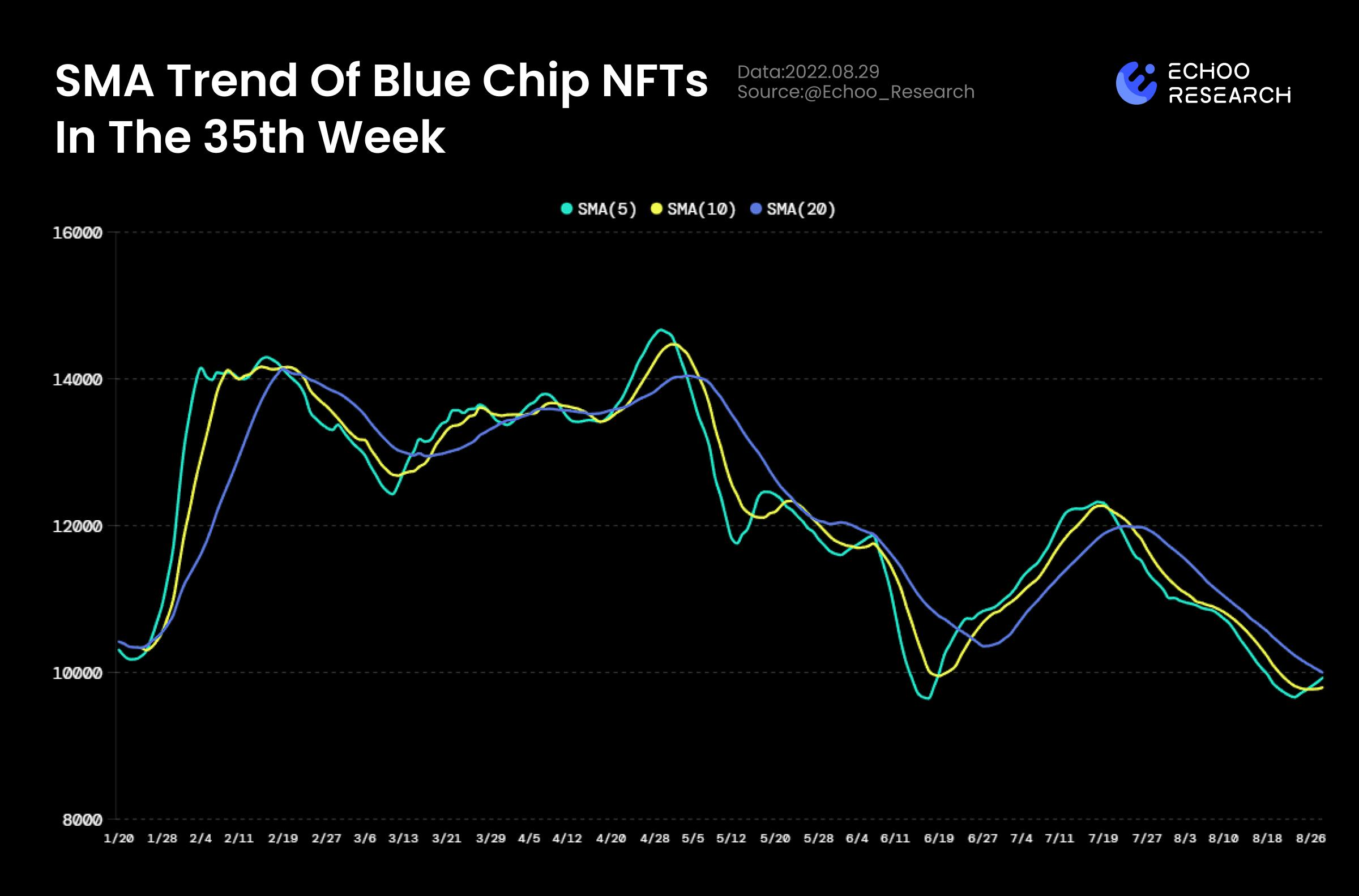

3.蓝筹集合的SMA趋势

近期蓝筹NFT的走势有反弹的迹象,打破了连续下行趋势,但反弹力度不够大,未能突破SMA(20)。

SMA Trend Of Blue Chip NFTs In The 35th Week

指标说明

该指标综合了蓝筹NFT的市值,运用均线进行计算,用来反映NFT大盘的趋势。

SMA:反映短周期于长周期的趋势。

简单使用方法:短周期线从下方穿过长周期线时为买入信号,短周期线从上方穿过长周期线时为卖出信号。