隐私对于 Crypto 来说是一件很奇怪的事,很多人不以为然,但也有人在不断专研新的隐私技术,那我们究竟是否应该拥抱隐私呢?

前些天,美国财政部宣布制裁了以太坊混币协议 Tornado Cash,并要求 Circle 冻结受制裁的 USDC 账户,此外,Tornado 的开发者也突然遭到了 GitHub 的暂时封杀。

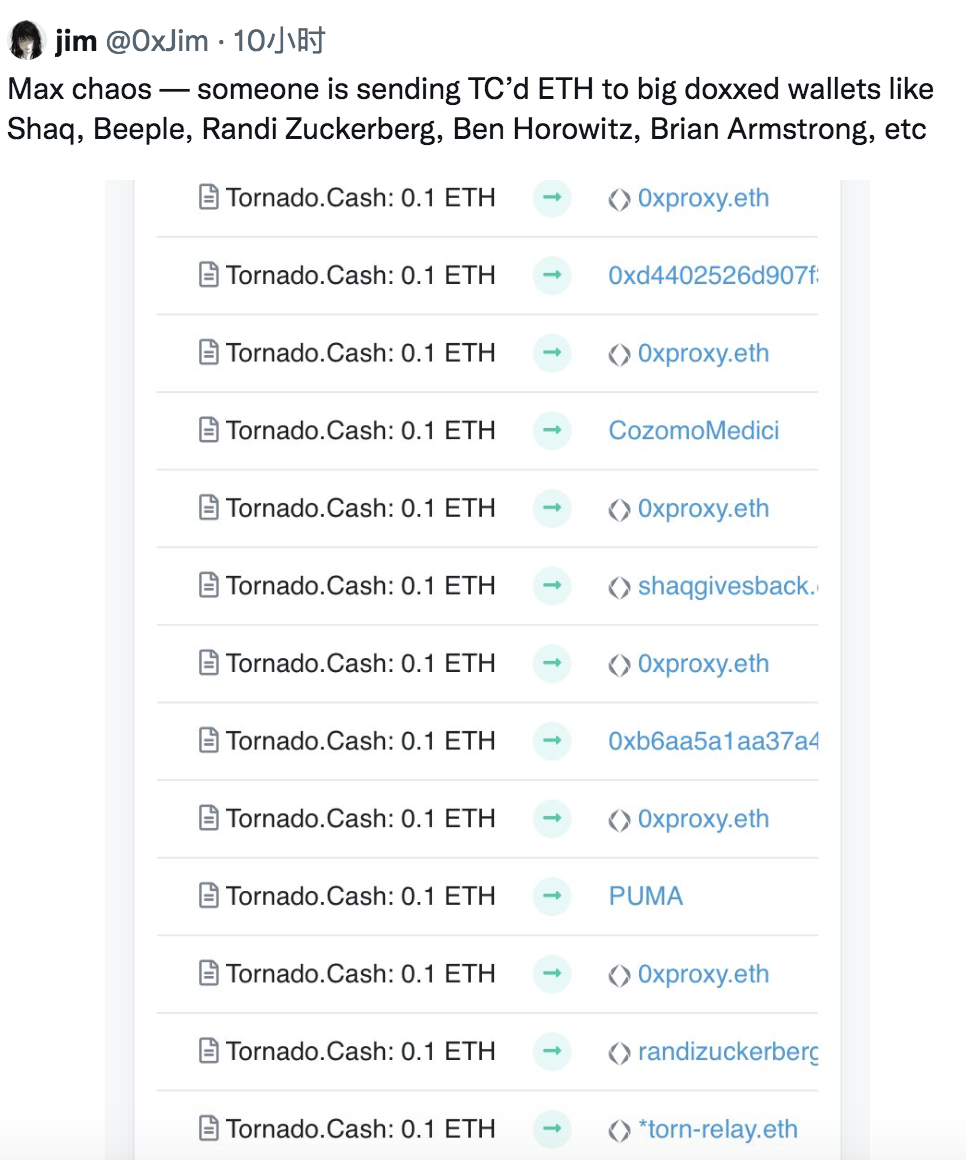

而在今日凌晨,有人开始将 Tornado Cash 混币过的 ETH 发送到 Brian Armstrong、Beeple、Shaq 等业内知名人士的 ENS 钱包地址,目的是让这些钱包也受到污染,这也被很多网友戏称为加密界的“投毒”事件。

而这一连串事件暴露出来了很多问题,以下是笔者暂时看到的 4 点:

1、老生常谈的中心化稳定币审查问题

USDC 作为一个受美国监管机构监管的中心化稳定币,自然是无法抗审查的,根据 Circle 首席执行官 Jeremy Allaire 透露,如果他们不冻结受制裁的地址,将面临故意逃避美国制裁合规义务的指控,这可能会导致最高 30 年的监禁。

这里需要明确的一点是,抗审查是适用于所有人的,因为被恶意“投毒”就会面临审查问题,那此时就关乎到你的财产了,哪怕你是无辜的,你的资产也可能会遭到冻结。

那我们是不是应该拥护一个去中心化的稳定币,最好是使用无需信任的比特币作为抵押品?(注意:WBTC 是需要信任的,它无法抵抗审查,因此 Makerdao 的方法是不可行的,我们首先需要的一个无需信任的 BTC 跨链方案)

2、中心化代码库的审查问题

此次 Tornado Cash 事件,GitHub 的封杀动作是令人意想不到的,而绝大部分所谓去中心化的 Crypto 项目代码库都依托于 GitHub ,因此有人便倡议建立去中心化的 GitHub,而例如 Radicle 这样的开发工具正在尝试做这样的事。

3、ENS 的隐私泄露问题

ENS 将复杂的以太坊地址替换为便于人类记忆的字符,这有助于 Crypto 的普及,然而它也带来了严重的隐私泄露问题。

以往,我们只是通过 ENS 地址来查探别人的财务数据,这仅仅是侵犯了隐私,但并没有造成实际的威胁,而在这次“投毒”事件当中,相关的 ENS 地址都可能会遇到一些麻烦。

这也提醒了我们,ENS 地址并不适合与个人的财务关联到一起。

4、可选隐私协议的致命缺点

最后,是 Tornado Cash 协议本身的问题,由于它是一个自由选择使用的协议,因此普通 Crypto 用户不太会去使用这个协议,而像黑客等对隐私需求较大的“用户”才会经常使用 Tornado Cash 混币协议,这引发了美国监管机构的担忧,并最终引来了制裁。

但如果隐私是一种默认选项,网络中的任何交易都带有隐私属性,那么这个网络的抗审查性会更强,当然,监管机构依然会追查相关的涉黑交易,这要求网络提供的隐私属性并不是绝对的,否则整个网络依然会遭到制裁。

而例如 Aleo 以及 Aztec 这样的通用隐私层协议,可能会改善这方面的一些问题,而它们能否平衡监管与协议可用性,会是它们能否取得成功的关键。

小结

全球监管机构对 Crypto 行业的监管只会越来越紧,这无疑会对现有的一些脆弱的基础设施造成巨大的冲击,但对一些新兴事物或叙事,这也意味着新的机会。而隐私作为区块链的重要属性之一,往往是被多数人忽视的,希望最近的事件能够改变这种状态,当然,需要指出的是,绝对的隐私是不允许被实现的,这一点不用怀疑。